The Dollar majors have been plying narrow ranges so far today, with global markets generally in somewhat of a directional stasis presently, with participants mindful of the potentially economically disrupting new waves and clusters of coronavirus infection outbreaks in reopening economies. There is also conjecture that even if the coronavirus remains reasonably contained, the rapid pace of the rebound out of the April nadir will taper substantially over the coming months.

Sterling

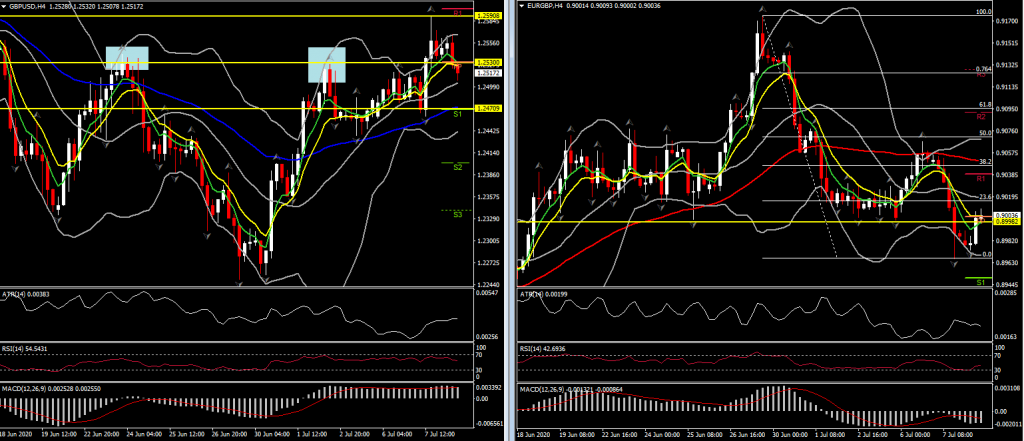

Sterling yesterday saw an upward rotation against the Dollar and Euro, along with most other currencies. Confirmation that UK-EU trade discussions will continue throughout July, and then recommence in the week of August 17th following the summer recess, along with some speculation that the two sides might make a political declaration of intent (to makE a trade deal) before the end of the month, were taken as a bullish cue by the forex market.

The UK government will also be presenting a budget update today, where a range of targeted measures to tackle rising unemployment are expected. These factors have for now offset negative leads, including reports that the BoE has been talking with commercial banks to prepare them for the possibility of negative interest rates.

Incoming data out of the UK, including yesterday’s release of the June construction PMI survey (which showed the sector returning to expansion), have been indicating a strong rebound from the April nadir, when the coronavirus lockdown measures were in full force. However, the path ahead looks to be a rocky one. New lockdown measures have been re-introduced in the city of Leicester, due to a spike in coronavirus cases there; an ominous sign of the challenges being faced as the UK economy reopens, especially with social distancing rules having been relaxed and with pubs and restaurants reopening.

Hence there is a net neutral view on the Pound. Cable will likely remain hostage to the ebb and flow of risk appetite in global markets.

Euro

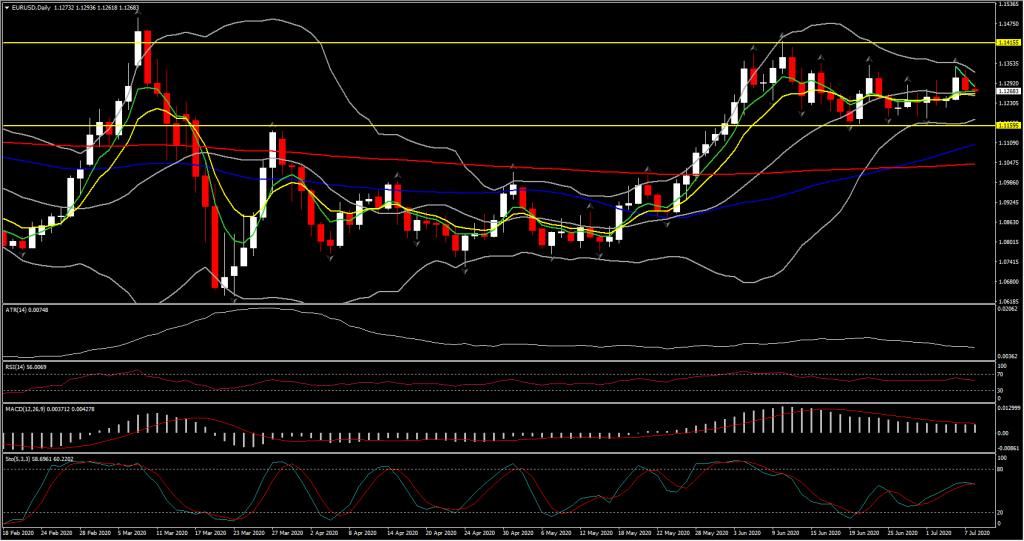

In Europe, however, since there wasn’t much progress on the EU-UK trade talks, the focus turned to the EU budget talks and of course the EUR 750 bln recovery fund as German Chancellor Merkel travels to Brussels to lay out her priorities for Germany’s EU presidency, which runs until the end of the year. EU heads of state are expected to meet at the end of next week, where an agreement on the details on the recovery fund is expected. So far the prospect of a jointly funded recovery program has been helping to prop up the EUR and failure would be a negative for the Euro.

So far today, EURUSD has drifted modestly lower, reflecting a pick up in demand for Dollars as European equity markets and USA500 futures turn lower, the latter more than giving back earlier advances. While there has been an abundance of above-forecast data out of the Eurozone and elsewhere of late, which has been a theme in global data releases since the April lockdown nadir, the pace of recovery is now likely to fall back. This especially looks to be the case given the problematic clusters of outbreaks of new coronavirus infections, which have been causing localised lockdowns across the world.

Markets look likely to remain trapped in a constant state of tweaking risk premia, which for EURUSD means downside pressure when the dollar gains on safe haven demand, and upside pressure when things are looking more rosy.

There is a slightly more circumspect view given the risks of setbacks on the road back to economic normalcy. Any upset on this front would be a negative for the Euro.Today’s local data calendar is pretty empty – German trade data are due tomorrow.

Click here to access the Economic Calendar