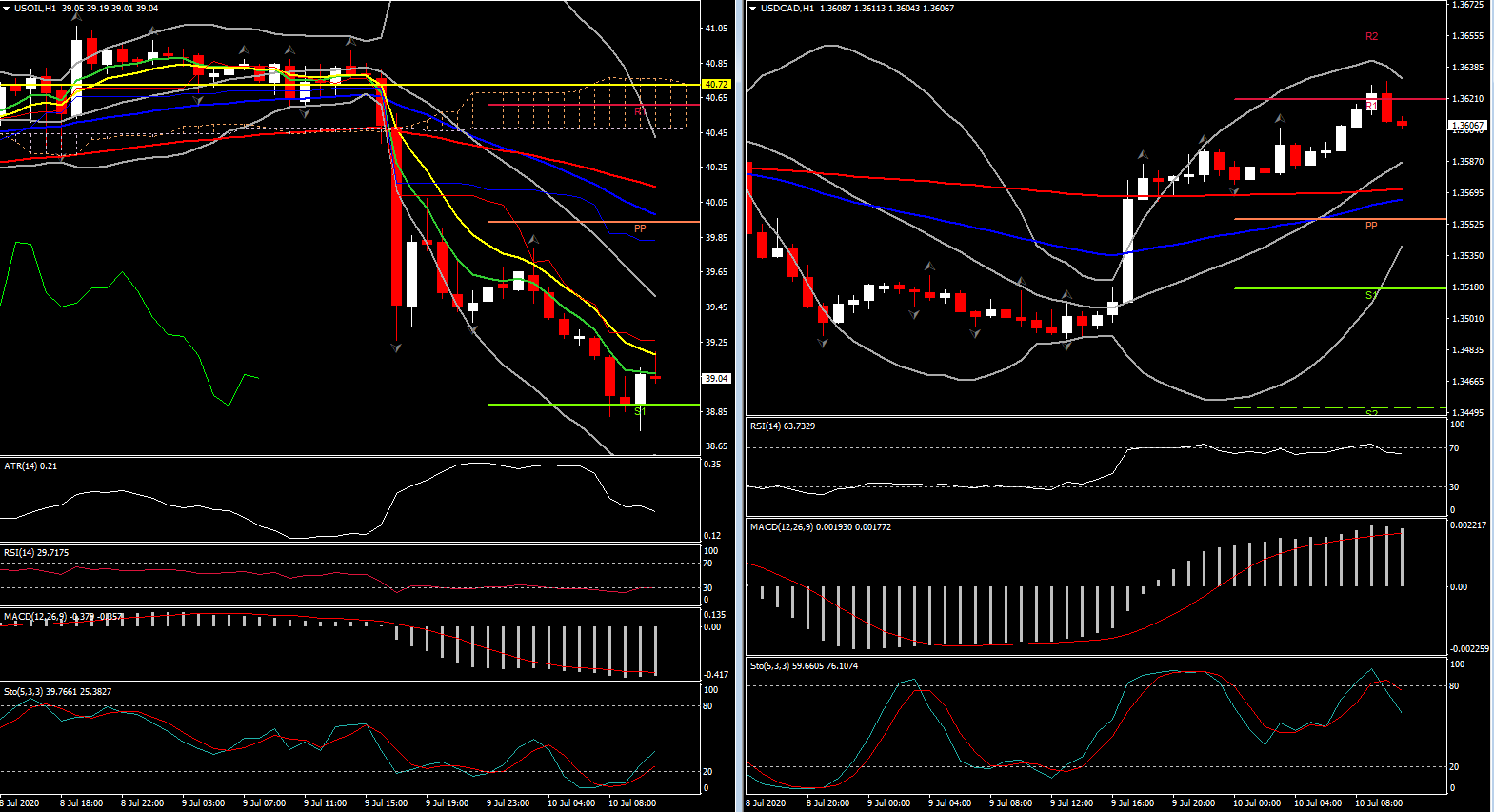

USDCAD has posted an 11-day high at 1.3628 (above R1) as USOil fell to an 11-day low at $38.74, extending the correction from the 17-day high seen earlier in the week at $41.63.

It was the SCOTUS ruling on Trump taxes, along with fears of new troubles for the aviation industry, that turned modest risk-on conditions into full-on risk-off that had the impact, seeing equities tank, yields fall, and WTI crude prices tumble nearly $1.50/bbl. Initially the decline started yesterday following the EIA inventory data which showed a 5.7 mln bbl rise in crude stocks. The street had been expecting a 3.0 mln bbl draw, though the API reported a 2.0 mln bbl build after the close on Tuesday. Meanwhile, gasoline supplies, seen flat, actually fell 4.8 mln bbls, while distillate stocks were down 3.1 mln bbls, versus expectations for a 0.5 mln bbl fall. The larger draws in products largely offset the higher crude build.

USOil overall remains in a broader consolidation phase after the post-lockdown rally peaked at a three-and-a-half-month high at $41.63 in late June. The outlook should remain neutral as global demand looks to be flattening out, and supply is looking to remain tight. The OPEC+ group are maintaining supply quotas, while US output has fallen from 13.0 mln bpd to 10.5 mln bpd. Reuters reported that 42 of 50 states have seen cases rise over the past two weeks versus the prior two-week period. Until the supply/demand picture clears up, WTI crude is liable to continue to trade in a narrow range near the $40 mark.

Nevertheless, the sharp rebound in oil demand from the April nadir has been priced in, with focus now on the coronavirus infection rate as economies reopen, which has caused some areas around the world to re-introduce lockdown measures. This backdrop of lockdown measures threatens to weigh on, or at least cap, oil prices, along with curtailing the Canadian Dollar’s upside potential. The USDCAD could revisit its 1-month high at 1.3716 if it sustains a move above 20- and 200-DMA and more precisely if it closes the week above 1.3600 (which is the 50% Fibonacci level since June’s downleg). Support comes in at 1.3484-1.3500, which encompasses the June-23rd 3-week low.

On the Canadian domestic front, the June employment report is up today. We are expecting a 700k headline gain after the 289.6k jump in May, with the unemployment rate seen ebbing to 11.0% from 13.7% in May.

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.