Economic activity has rebounded on both sides of the channel as lockdowns were lifted, but the impressive rebound in confidence data in recent months has proven to be too optimistic on the speed of the recovery with real sector data for May actually looking weaker than hoped. That ties in with the moderation in market confidence, which was also reflected in German ZEW investor confidence, which pulled back from June highs in today’s July numbers. Central bankers meanwhile acknowledge that the second quarter may not have been as bad as initially feared and have essentially switched to a wait and see stance, after putting substantial crisis measures in place.

With that in mind the ECB is widely expected to keep policy settings unchanged at today’s meeting. Lagarde’s recent comments suggest that data releases have come in slightly better than officials had feared and the central bank seems ready to move out of crisis mode and into a wait and see stance. That doesn’t mean the ECB won’t keep the option of additional easing measures open, but for now officials should be able to afford to take a step back and monitor the impact of crisis measures already implemented.

Wait and see then is likely to be the main message at today’s council meeting, although Lagarde will, however, stress again the need for fiscal stimulus to support monetary policy and step up the pressure on politicians to come to an agreement on the proposed EUR 750 bln pandemic recovery fund, that will be discussed at the EU leaders summit later in the week. Central bankers have long stressed the need to complement monetary policies with appropriate fiscal policies and on the whole central bankers also seem to welcome the proposal for a jointly funded mechanism and a focus on grants rather than loans.

The debate will take place within the context of the EU’s next multiannual budget framework, and won’t be easy, as countries disagree on whether to focus on grants or loans and whether jointly backed market funding is the right way forward.

Markets have the fund pretty much priced in and the risk is of course that the reality of EU politics once again falls short of what investors are looking for.

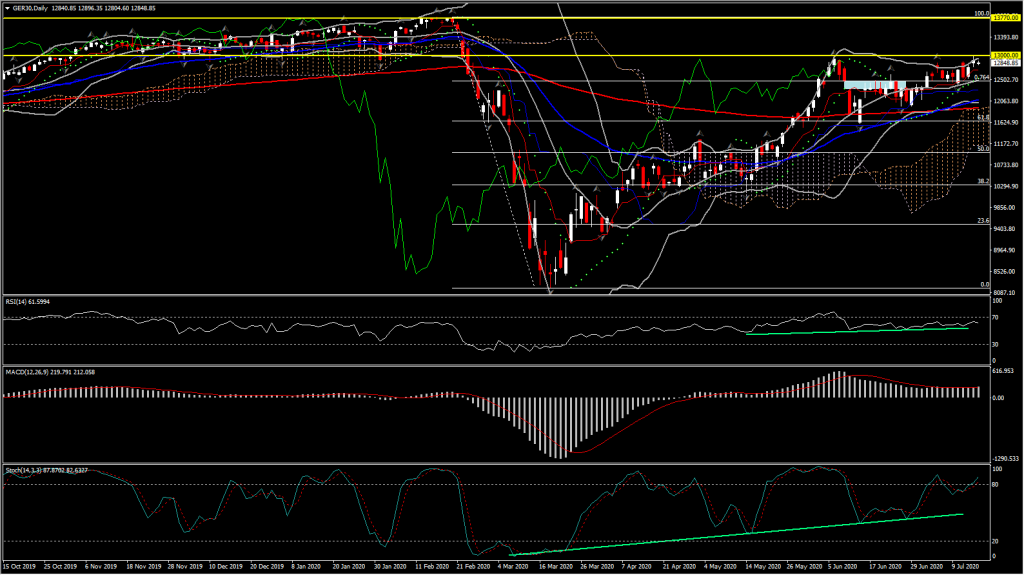

DAX – GER30

Meanwhile European stock markets are broadly lower with peripheral markets outperforming slightly going into the ECB meeting. General risk appetite has waned again amid concerns about the global outlook and rising tensions between the US and China. The GER30 is currently down -0.8%, and the UK100 down -0.9%, while IBEX and MIB are posting losses of -0.1%. US futures are also heading south following on from a broad move lower across Asian markets.

GER30, despite the short term decline, sustains 4-month highs, close to the 13,000 area. The index filled May’s and June’s gap, while it has been trading well above Ichimoku cloud since May, suggesting an overall positive bias. All daily exponential moving averages (20, 50 and 200) are aligned northwards. Momentum indicators are gradually moving more positive as the market has pulled higher this week. RSI is above 60 and confirming higher lows since early June, inline with the uptrend in the price action along with strong positive configuration on Stochastics, despite the flattening of MACD lines that suggest consolidation. The bulls could be looking to use any near term weakness as an entry point. Hence Support could be seen at 12,500 (20-DMA and 76.4% Fib. level since January 2020).

It is interesting to see though that despite the positive technical background it struggles to break the 13,000 Resistance area.

EURO

The EUR fell back against a generally stronger US Dollar, with EURUSD trading slightly above S1 at 1.1384. Risk appetite waned again, amid concern about the world recovery, and US-China tensions and with the security breach at Twitter Inc not helping. Eurozone markets which traded unevenly yesterday are likely to remain cautious going into the ECB announcement today.

EUR intraday remains under pressure with fast MAs aligned lower and lower Bollinger bands extending southwards. Next immediate support could be found at 1.1350, and 1.1330 (200-EMA in 1-hour chart). Volumes meanwhile declining suggesting that the bullish momentum seen since 10 of June is threatened.