USDJPY, H1

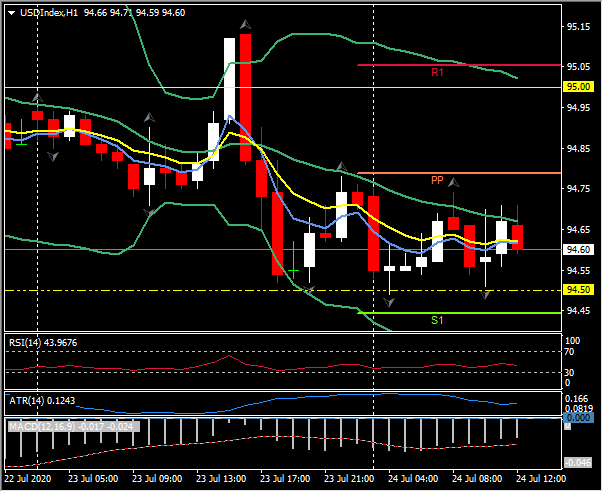

The Yen has outperformed today as risk aversion took a firm grip on global markets. The Dollar has so far failed to pick up safe haven demand, and has remained on a softening path. The narrow trade-weighted USDIndex carved out a fresh 22-month low at 94.49. The Dollar has lost appeal partly on the advent of the EU’s recovery fund, seen as a milestone by many analysts that has served to tip the balance out of the dollar’s favour, and partly amid expectations for dovish guidance from the Fed at next week’s FOMC, with some speculating that the US central bank is considering yield curve targeting. A Reuters survey highlighted increasing pessimism about the nearer-term US outlook given the extent of localized lockdown measures in response to the spike in coronavirus cases across many southern and western states. Intel also underwhelmed markets in its guidance for Q3 earnings.

Against this backdrop, EURUSD remained firm, although off from the 21-month peak that was seen yesterday at 1.1628. USDJPY dropped by 0.5% to a one-month low at 106.17. Yen crosses were concurrently weak, driven by safe haven demand for the Yen. EURJPY fell to a two-day low at 123.36, extending a correction from Wednesday’s seven-week peak at 124.30. AUDJPY has been the biggest mover of the day so far, dropping 0.6% to a three-day low at 75.32. AUDUSD fell by a lesser magnitude, but still managed to peg a three-day low, at 0.7074. USDCAD lifted to within a pip of its peak from yesterday, at 1.3428. Oil prices have remained heavy after yesterday sinking to three-day lows. Cable edged out a fresh six-week high at 1.2773. The pair has been trending higher for about three weeks, though recent daily price action has been jagged and upside momentum has been waning, with the Pound having been weakening against other currencies on signs, and confirmation at a press conference yesterday, that the UK and EU remain deadlocked on key issues in trade talks.

The first reading of July PMIs from the Eurozone and the UK both beat expectations earlier. The Markit Composite EZ number came in at 54.8, significantly above expectations of 51.1 and back in expansion territory over 50.0. The preliminary UK July PMI surveys smashed expectations, with the composite headline surging to a five-year high of 57.1, up from 47.7 in the final reading for June and well up on the median forecast for a 50.8 reading. This extends the strong rebound for a third consecutive month from April’s series-record low at 13.8. The services PMI rose to 56.6 from 47.1 and the manufacturing PMI lifted to 53.6 from 50.1. However, a note of caution accompanied the data, with Markit noting – “July’s PMI represents a step in the right direction, but there is a mountain still to climb before a sustainable recovery is in sight.”

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.