The Dollar is down for a second day, with the narrow trade-weighted USDIndex printing a six-day low at 93.08 to nearly fully unwind the gains seen in the wake of last Friday’s US July jobs report, when we printed an eight-day high at 93.87.

Some market narratives have been attributing the Dollar’s ebb as being a return of the currency’s inverse correlation with stock market direction, along with the perception that the Fed has strategically dropped its concern about inflation risk, which has driven real US yields into negative territory. These factors appear to be outweighing the improvement in the US economy and downward trend in new coronavirus cases. As for Washington’s tensions with Beijing, this hasn’t been much of a concern for Wall Street, with most onlookers anticipating this weekend’s meetings to review progress on the Phase 1 trade deal will go well, even though China has been lagging behind in its purchases of US farm and energy goods.

Among the main Dollar pairings, EURUSD climbed to a six-day high at 1.1838, putting the 27-month high seen last Thursday at 1.1917 back in the scopes. USDJPY extended a moderate correction from yesterday’s three-week high at 107.03, posting a low at 106.57. The Yen was more mixed against other currencies, with EURJPY remaining buoyant, just off the 16-month high that was pegged yesterday at 126.23, while AUDJPY traded softer after the cross peaked at a three-week high yesterday. The Nikkei 225 hit a six-month high, which followed a strong close on Wall Street yesterday, with the S&P 500 finishing just a whisker below a record closing peak. European stocks have opened lower with GER30 holding over 13,000 at 13,025 and the UK100 trades down around 6,200. AUDUSD edged out a two-day peak at 0.7188. Australian July employment data showed a forecast-smashing 114,700 rise in the headline, while the June figure was revised higher, though lockdowns across the country are now blighting the immediate outlook. USDCAD settled just above Wednesday’s six-month low at 1.3227.

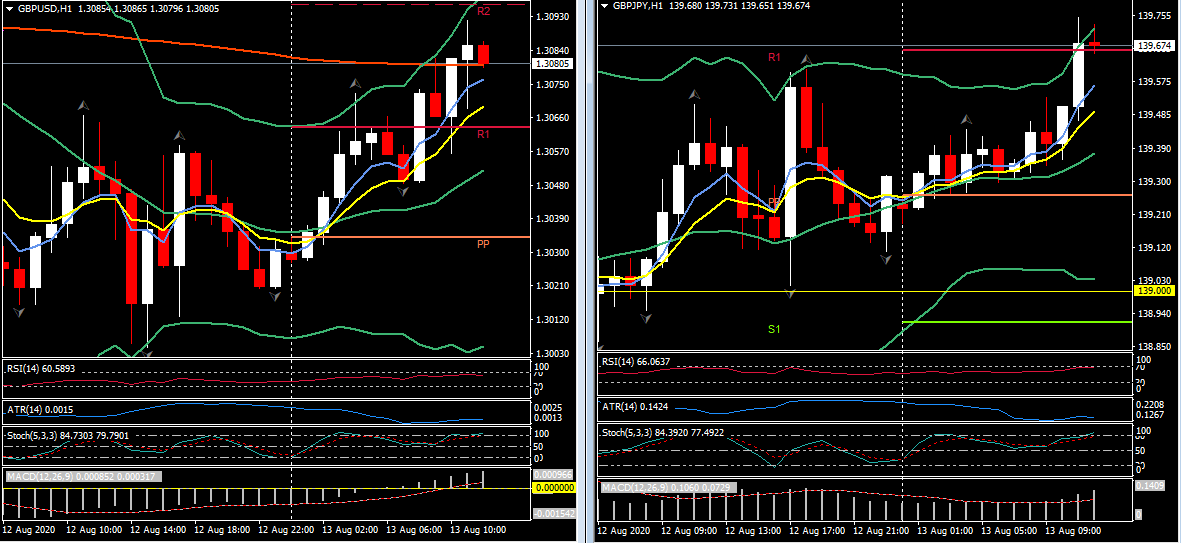

Sterling is trading mixed, edging out a two-day high at 1.3092 against the Dollar, while also gaining on the Yen and Aussie Dollar, but holding steady-to-softer versus the Euro and some other currencies. Yesterday’s preliminary UK Q2 GDP data showed a gargantuan 20.4% q/q contraction to confirm the technical definition of recession following Q1’s 2.2% shrink. The data wasn’t a surprise given the lockdown that was in place to varying degrees throughout the quarter. June GDP rose by 8.7% m/m, however, with June production data showing a robust rebound and beating expectations in the main headline readings, while high frequency data and a myriad of anecdotal evidence point to a strong rebound in the current quarter. The government’s furlough scheme has greatly limited the impact on the employment market. We have been talking down the Pound, to a degree, having seen limited scope for the currency to sustain its recent patch of outperformance. The BoE last week delivered a warily-upbeat outlook, though with localized lockdowns and most media doing their utmost to maintain maximum fear of a second wave of coronavirus infections, we take a circumspect view of the outlook over the coming months, anticipating a plateauing in economic rebound momentum. Manchester, Preston, Bradford and Aberdeen are back in lockdown and there is a number of new travel restrictions with other countries. The furlough scheme will end in late October, which is likely to trigger a wave of job losses, particularly in the airline, retail and hospitality sectors.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.