USOIL futures hit a 2-month low at $38.54, since recouping to levels in the mid $39.0s but remaining over 1% from the low from Friday’s closing levels. Prices are down by over 10% from the highs seen last week. The stalling out in the recovery pace of the global economy, along with large crude stockpiles and uncertainty about Chinese demand (which has been importing crude in record quantities in recent months, but may now be ready to slow this process down) has weighed on oil. Additionally, Saudi Aramco’s announcement on Sunday that it would cut prices on crude shipments to Asia also added significant pressure to Oil.

The end of the North American summer driving season has also been getting a mention in market narratives. This backdrop should keep USOIL lower, and therefore maintain USDCAD’s steady-to-upward bias for now. Currently, USDCAD has floated to a 4-day peak at 1.31387, aided upwards by a generally firmer US currency and a drop in oil prices.

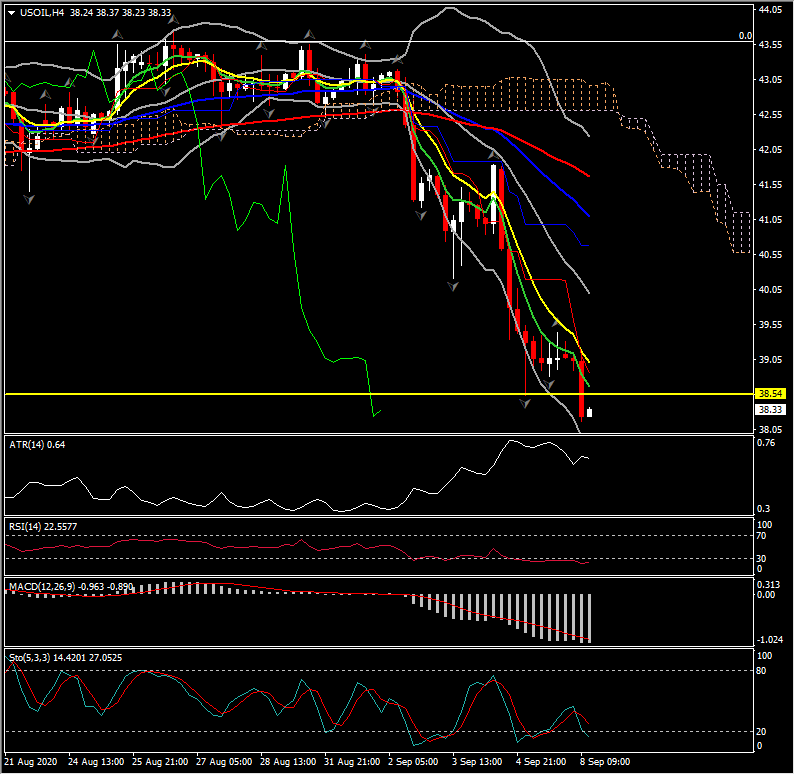

USOIL currently trades below 38.50 (latest double fractals reflecting strong support area). The breakout today below the latter, along with the fact that the asset is below 200-DMA for the 2nd day in a row, suggest an increasing negative bias in the near term and medium term since momentum indicators are also negatively configured in both time zones without reaching OS levels yet.

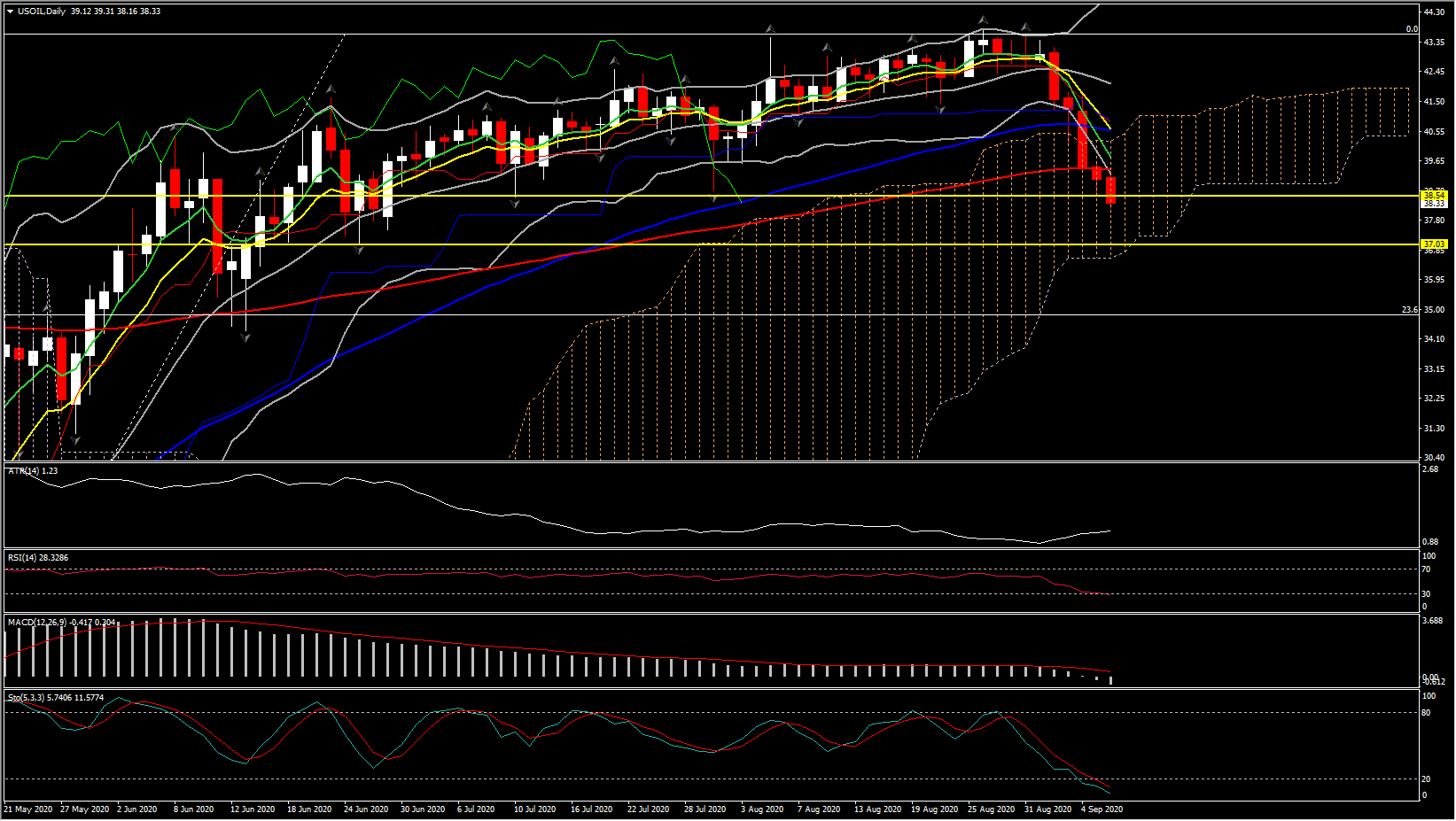

Near term decline is also reflected in the Ichimoku lines (1- and 4-H chart), as the bears drove the price below the Ichimoku cloud. In the daily chart however, the sellers have not managed to drive the asset below the cloud yet. Therefore the $37.00 support could interrupt the pair ahead of the $35.00 handle. In the event selling interest persists the key support level of $35.00 could halt the decline (26.3% Fib level).

Nevertheless, in regards to weekly events, the Bank of Canada is the focus this week, however it is not expected to impact the Canadian Dollar or USOIL. A steady 0.25% policy rate is widely anticipated from the BoC.

A reiteration of the forward guidance that debuted in July is expected, when the Governing Council said it “will hold the policy interest rate and effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved.” At that time, the Bank observed that the economy “will require extraordinary monetary policy support” as the recovery progresses. A similar sentiment should be on offer this week.

Governor Macklem delivers a speech to Canadian Chamber of Commerce on Thursday. A thin slate of economic data is on offer this week, with August housing starts (Wednesday) and Q2 capacity utilization (Friday) the highlights. Housing starts are seen easing to 210.0k in August from 245.6k in July, bringing it back near the 212.1k in June. Starts plunged to 164.9k in April and firmed to 195.8k in May. Similar to the US, housing has been underpinned by low mortgage rates.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.