Canada’s CPI accelerated to a 0.7% y/y pace in October from the 0.5% rate of expansion (y/y, nsa) in September. CPI climbed 0.4% on a month comparable, not seasonally adjusted, basis in October after the -0.1% dip in September. The increase relative to September is consistent with the usual seasonal strength in CPI. A decline in gasoline prices exerted the anticipated drag — CPI excluding gasoline rose 1.0% y/y in October, identical to September. The three core CPI measures averaged 1.8% in October, up from 1.7% in September but still running under the BoC’s 2.0% target midpoint.

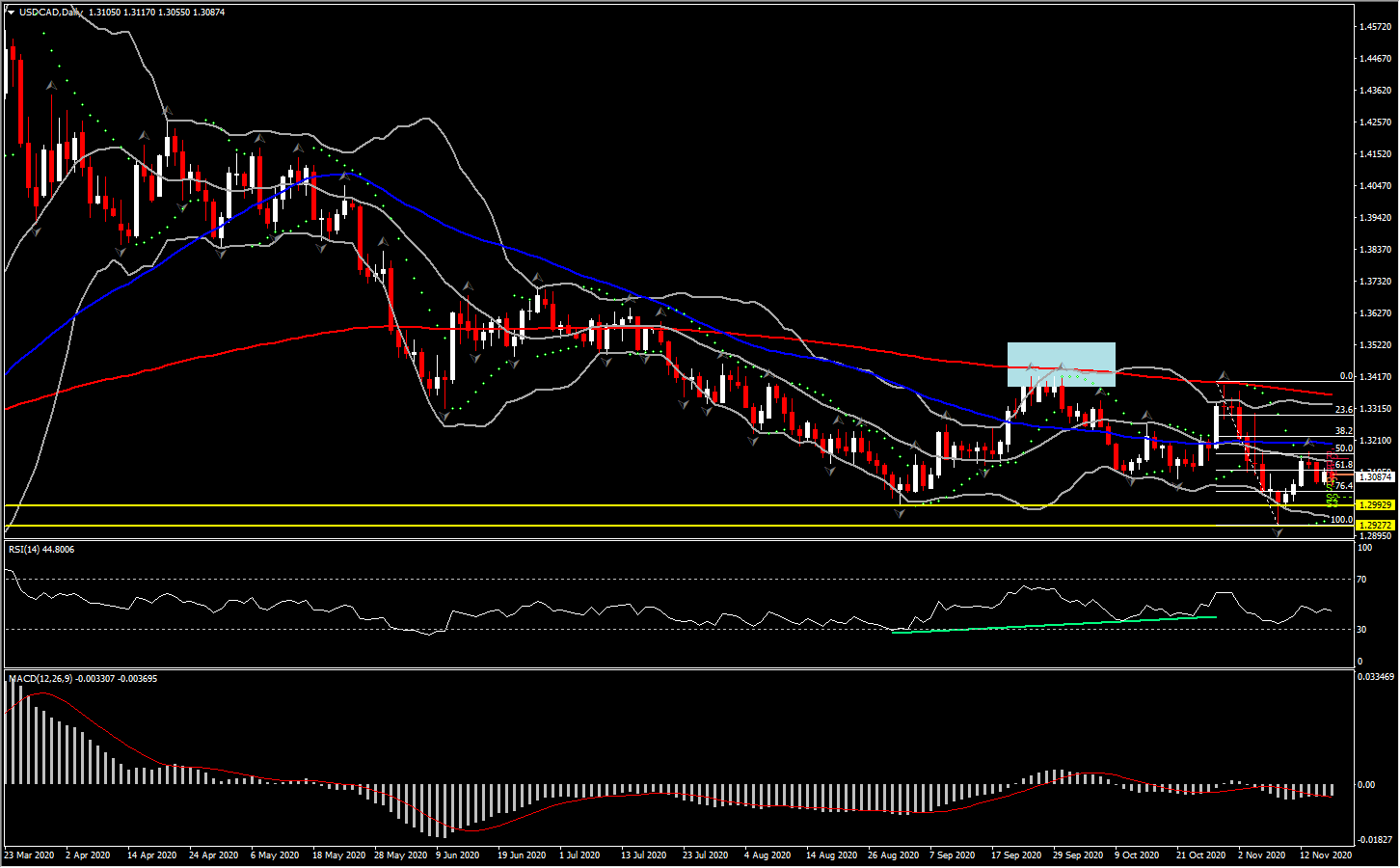

Overall, total and underlying inflation remains tame, supportive of the BoC’s commitment to keep rates on hold for an extended period. USDCAD reacted positively on the data announcement as USD gained some ground after US housing starts beat expectations. However USDCAD is under pressure for the 4th day in a row. USDCAD has been trending lower since March, and it seems that there is more to come as the current trend low is at 1.2928, which was seen last week, and which was the lowest level the pair has seen since October 2018.

Meanwhile, there has been evident caution after recent strong gains in world stock markets. Markets have remained buoyant on vaccine news, as the USA30 is 0.4% firmer, the USA500 is 0.2% in the green and the USA100 has edged up 0.1% in pre-market futures trading. In Europe, the Euro Stoxx and GER30 have both risen 0.3%. The UK100 is also up 0.3%. In vaccine news, Pfizer announced that its vaccine was 95% effective in final data and that it will seek government authorization in the next few days, leaving the treatment on target to go into distribution by the end of the year if approved, reports the WSJ (paywall).

Commodities also rallied, particularly metals, with aluminium prices, for instance, extending recent solid gains in posting the highest levels seen since late 2018. The gains in commodities are both a negative for the Dollar and a positive for the dollar bloc currencies.

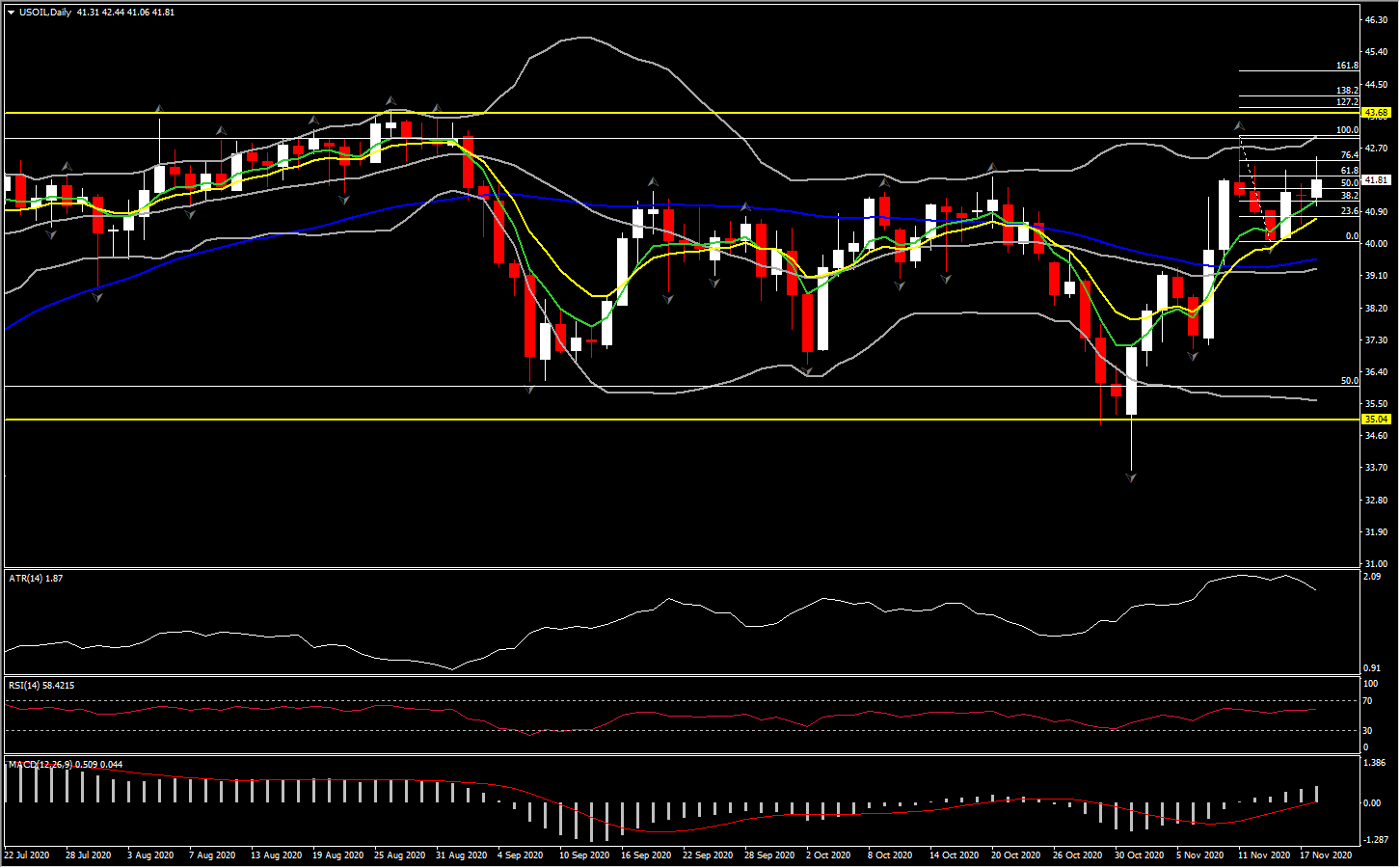

A key factor influencing metal prices has been recent data from China showing its economy is in stronger than recently anticipated shape. Disrupted copper supply out of Peru, which is the world’s number two copper producer, along with the launch of an international copper contract in China, are other factors with regard to metals. Oil prices have also been buoyant, with USOIL prices drawing nearer to last week’s 8-month high. The OPEC+ group’s musings about extending the prevailing restricted output quotas out to next March, and possibly June, with the aim of swinging the oil market back into deficit (supply deficit) by mid 2021, has been supportive of oil prices.

Currently USOIL is up 1.0% from Tuesday’s close, trading at $42.00 after peaking at $42.68 into the open. Prices were under some pressure after the close on Tuesday, when the API reported a larger than expected 4.2 mln bbl build in weekly crude stocks. The oil market will now look to the 10:30 ET release of weekly EIA inventory figures.

The potent mix of low interest rates for the foreseeable future, quantitative easing, fiscal stimulus and the prospect for more, spare capacity (which maintains low costs), and the vision of a return to normalcy in 2021, suggests there is more to come from the rally in cyclical assets. This in turn could be negative for the Dollar.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.