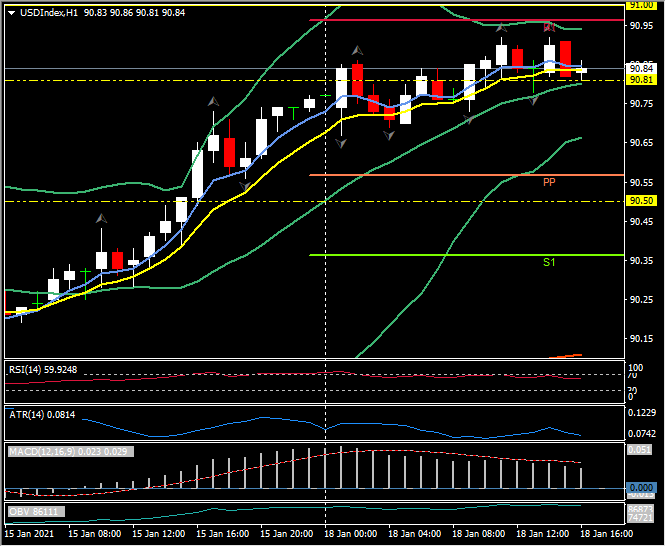

USDindex, H1

The USDIndex has posted a one-month high at 90.88, which sets up potential for a third consecutive up week, something that hasn’t been seen since January last year. Other currencies have mostly softened, especially the dollar bloc and other cyclical currencies as global stock markets have continued to sputter. Chinese equities have been the exception, with the CSI 300 showing over a 1% gain in the late afternoon session having rebounded out of early declines following strong growth data. China Q4 GDP rose 6.5% y/y, beating the median forecast for 6.1%, with full-year growth coming in at 2.3%, which is impressive given that all other major economies contracted. Equity markets in Asia outside of China failed to catch a coattail, with the main indices in Japan, South Korea and Australia, for instance, all racking up fairly hefty declines.

Stock markets around the world have lost the ‘great reflation trade’ spirit that had been so strong in November and December. Various factors seem to account for this. One is that the winter surge in Covid-19 across the densely populated northern hemisphere has been perhaps worse than many had been anticipating, leading to tight societal restrictions across major economic areas, albeit not as severe as seen during the ‘mother lockdowns’ seen in the first wave. New variants in the SARS-Cov2 coronavirus has been a further concern, given the risk they could render current vaccinations less effective or even ineffective (a better understanding about this should emerge over the coming weeks). This has come as asset valuations at lofty levels, ranging from the record highs in US Indices to the nine-year highs in iron ore prices, and with investors relatively low on spare cash. In the mix was an apparent sell-the-fact type of reaction after US President-elect Biden last Thursday confirmed a $1.9 tln fiscal spending package. The transition of political power in the US this Friday is also being viewed as something of a risk event, given the threat of violent protests. The cautious sentiment looks likely to persist for now.

European stock markets have traded cautiously mixed so far today. The GER300 is currently up 0.03% and the UK100 down -0.27%, while US futures are posting fractional losses. The US markets are closed for Martin Luther King Jr Day today, which is making for quieter trading conditions as investors are also questioning how much of Biden’s stimulus program will survive the approval process.

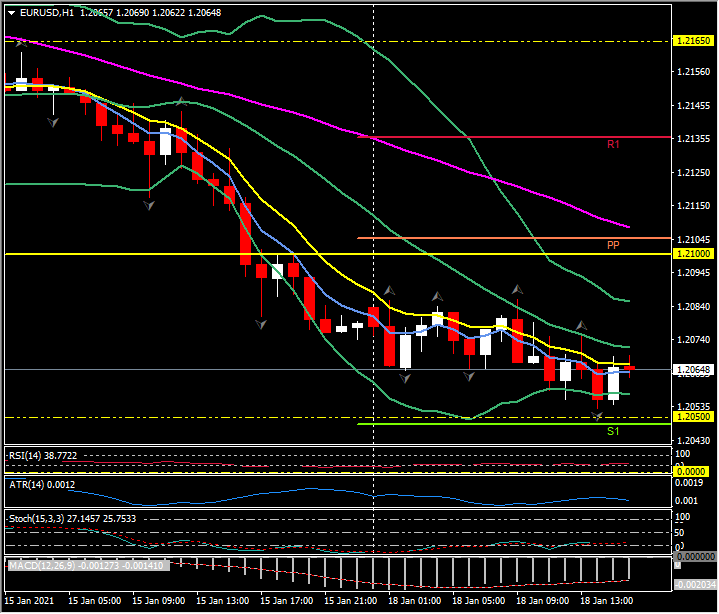

Elsewhere, EURUSD trades down again, earlier posting a new seven-week low at 1.2053, which extends a two-week run lower. The pair has corrected from the 33-month peak that was seen last week at 1.2350. Cable ticked lower under S1 to 1.3518, and USDJPY is oscillating through today’s daily pivot point at 103.75. USOil has recovered from a test of the 200-hour moving average earlier at 51.80 to trade at $52.25 and Gold, having plummeted to $1810 on open, has recovered to its daily pivot point at $1836. The 200-day simple moving average ($1842) was breached and broken on Friday for first time since November 30 last year.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.