Market News Today – Yields spike (10-yr +9.27% – over 1.52), Equities tank (Nasdaq -3.52%, Nikkei -4%), USD off 3-year lows. Commodity, EM currencies & Sterling cool from highs. Oil holds up (US attack on Iranian groups in Syria), Gold falls further under $1770, BTC at $45K. US data yesterday biased to the upside (big fall Claims, Durables beat & GDP in-line.) Overnight – weak Housing, also weak but better than expected CPI & Retail data from JPY. Senate rejects $15 min wage in Stimulus bill and looks to trim the $1.9t proposals.

The dollar and yen rallied as a risk-off theme coursed through global markets, with equity markets, commodities, including base metals and oil, all tumbling. The sharp spike in US and most other sovereign yields this week and the associated concerns about inflation have driven the correction in risk assets and currencies. We maintain that sovereign yields are lifting out of exceptionally low levels, that rising yields and interest rates are par for the course in major bull markets in equities by historic standards, and that the prospect of higher corporate earnings can still carry equities higher. But for now, the prevailing bias is a risk-off one, although Treasury yields have dropped back quite sharply from highs today. In the mix today has been news of a US airstrike in Syria against infrastructure used by Iranian-backed militia, which was reportedly in response to recent Iranian attacks on US interests in Iraq.

The USDIndex rallied nearly 0.5% in posting a four-day high at 90.49, while EURUSD concurrently dropped to a two-day low at 1.2129. Cable retreated back under 1.4000 on route to pegging an eight-day low at 1.3903. The Australian and New Zealand dollars underperformed, not surprisingly, having been outperformers during the risk-on times. AUDUSD fell over 0.5% in printing a one-week low at 0.7805. USDCAD lifted to a four-day peak at 1.2649, extending the sharp rebound out of yesterday’s three-year low at 1.2466. The Yen, meanwhile, has been the biggest gainer, outperforming even the dollar so far today as its traditional role as a haven currency become re-established. USDJPY dropped from a six-month high at 106.43 to a low at 105.86. Yen crosses dropped sharply out of trend highs in synchrony, with AUDJPY, for instance, diving some 2.5% from the three-year high the cross had seen yesterday.

Over in the cryptocurrency world, sharp declines have made a return. Bitcoin has hit a low so far just above $44,000, which is nearly 15% down on yesterday’s high and some 25% down on the record peak that was seen earlier in the week. Arguments by crypto advocates that bitcoin is a hedge against inflation have evidently been found wanting.

Today – US Personal Income, PCE & core PCE, Chicago PMI, Uni of Michigan, ECB’s Schnabel, BoE’s Ramsden, Haldane.

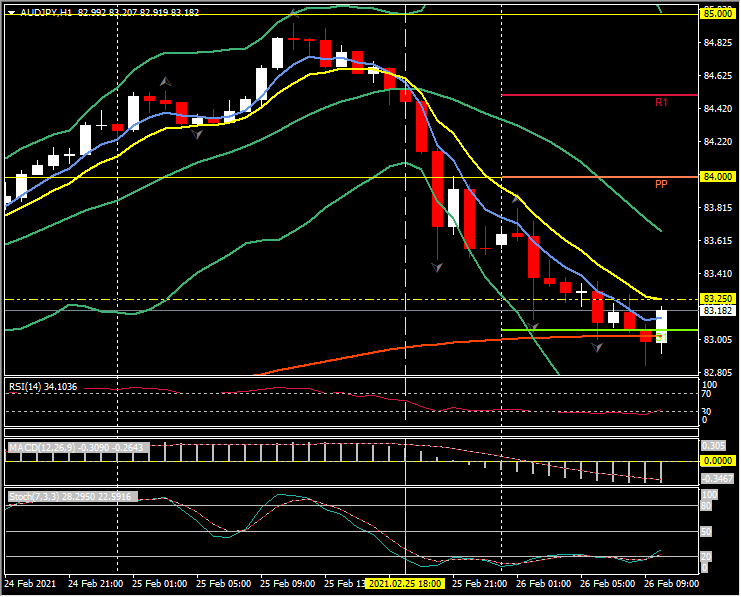

Biggest (FX) Mover @ (07:30 GMT) AUDJPY (-0.61%) Reversal of yesterday’s rally towards 85.00. Broke lower and under 20MA at R1 84.45 yesterday, now under PP and testing S1 and 200hr MA at 83.00. Faster MAs aligned and trending lower, RSI 34 and falling, MACD histogram & signal line aligned lower, falling after break of 0 line earlier. Stochs up from OS zone and rising again. H1 ATR 0.1325, Daily ATR 0.6000.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.