")

The major indexes surged sharply higher on the back of more good news on vaccines and the expectation of massive stimulus sooner than later. Another batch of stronger than expected data helped too. But opening the door for the gains was the more subdued tenor of the Treasury market. In the Asia session, the risk aversion returned and stock market sentiment faded. Major indexes quickly pared early gains and headed south, while Treasuries were supported and the US rate dropped back -0.2%.

The risk-on flows lifted longer dated Treasury yields, but the cheapening was much more orderly than last week’s furious 20 bps intraday jumps in the 10- and 30-year maturities. A heavy corporate calendar is also contributing to the losses in Treasuries with the focus on a $7 bln 6-part deal from Goldman Sachs.

Headlines:

- The February ISM and the January construction spending strongly beat expectations and contributed to upward revisions in GDP projections.

- The RBA left policy settings unchanged and while that was expected, market reaction suggests that there was some hope of supportive action, especially after the central bank doubled its bond purchases on Monday.

- China’s banking regulator highlighted worries about bubbles in overseas financial markets, but also domestic property markets, with suggestions that leverage will be reduced, which only added to concerns about further tightening in China.

- Dovish comments from ECB’s Villeroy, who called for an active use of PEPP purchases and flagging the possibility of a deposit rate cut seem to have helped to boost confidence that the central bank will manage to avoid a cliff edge scenario on stimulus, without stoking inflation.

- The Pfizer PFE.N and AstraZeneca vaccines are more than 80% effective at preventing hospitalisations from COVID-19 in those over 80 after one dose of either shot, Public Health England said on Monday, citing a pre-print study.

Forex Market

EUR – 3rd day lower at 1.2075. Next Support at 1.2000.

GBP– crossed the 20-DMA and currently is traded at 1.3878.

JPY – Yen found buyers, leaving USDJPY at 106.80.

AUD – holds steady between 20-and 50-DMA

CAD –CAD has been soft, weighed on also by the continuing weak oil prices during the session.

GOLD –slumped to its lowest in 9 months, as a stronger Dollar and elevated US Treasury yields eroded investor appetite for the non-yielding metal.

USOil – below $60 as expectations that OPEC would agree to raise oil supply in a meeting this week added to pressure and worries over slowing demand in China dampened sentiment.

Today: Calendar focuses on Eurozone inflation data for February, as well as German jobless numbers and retail sales and Canadian GDP for Q4. Also on tap speeches from ECB’s Panetta and Fed’s Brainard.

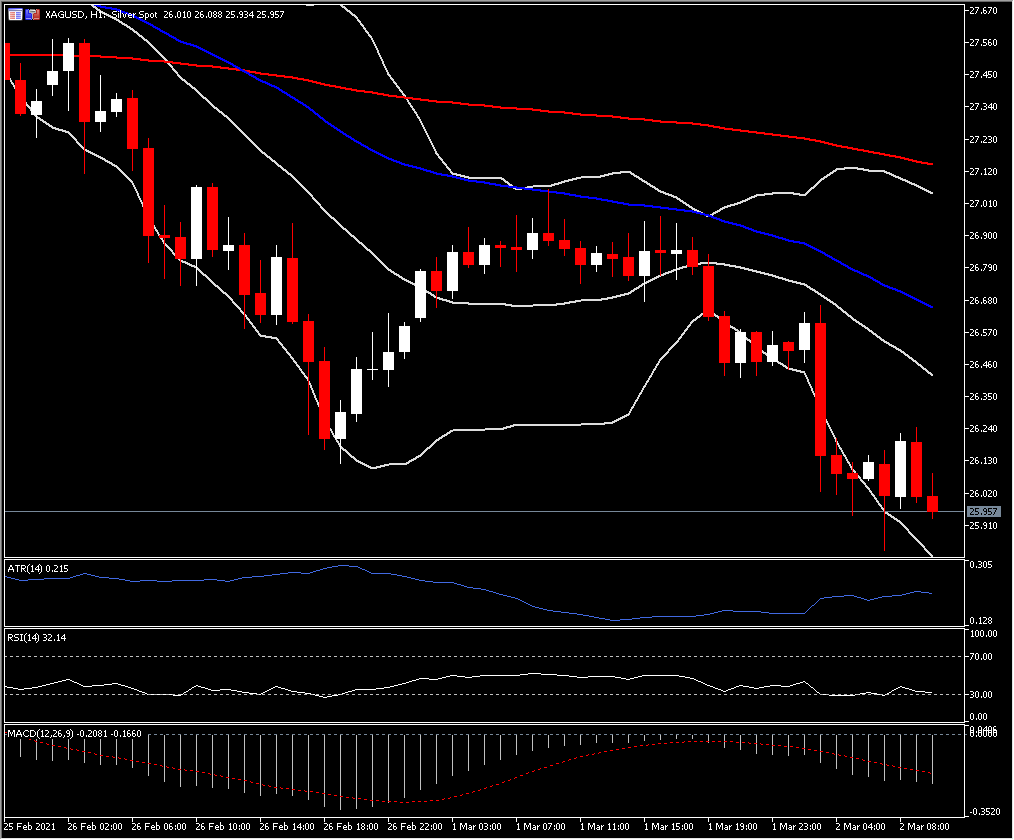

One of the bigger movers – XAGUSD (-2.19% decline)

Click here to access the our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.