Market News Today – Fears over rising inflation weighed on both stocks and bonds, with equities bearing the brunt of the pressure. The broader indexes were the underperformers with the USA30 dropping -1.9% and the USA100 was down sharply too, off nearly -2%. Today, GER30 and UK100 futures are down -0.3% and -0.2% respectively. The rout in tech stocks in particular continued to see wider markets selling off overnight, and European bourses are likely to continue to struggle ahead of key US inflation data later today. Treasuries were heavy too, led by the long end amid the inflation threat. Yields have spiked in Australia and New Zealand, after some warnings that Australia could lose its AAA rating.

Inflation fears have made a comeback although the sell off in equities seems to be abating somewhat, likely also thanks to ongoing verbal support from central banks, which continue to see the current spike in inflation as transitory. There was a plethora of Fedspeak and all concurred it was not the time to discuss tapering, while suggesting the disappointing jobs report was likely due to other issues aside from unemployment benefits.

In FX markets, the USD strengthened and USDJPY lifted to 108.89. AUD and NZD are broadly lower. Cable eased at high levels currently at 1.4130, EURUSD sustains support at 1.2115 for a 3rd day. USOIL stabilised at the $65 area.

Today – Today’s US inflation reading aside, the local calendar confirmed German HICP inflation at 2.1% largely thanks to base effects from energy prices. UK GDP for Q1 came in a tad better than feared, with the quarterly rate showing a contraction of -1.5% q/q, largely due to lockdown measures.

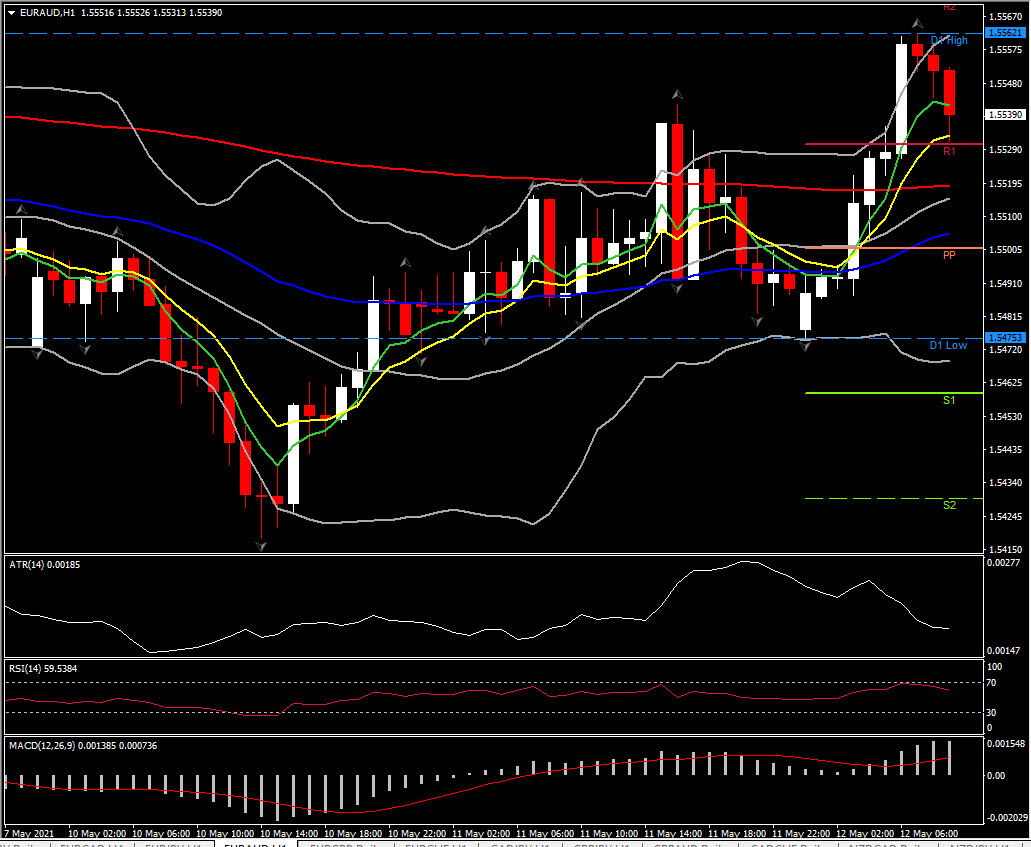

Biggest (FX) Mover @ (07:30 GMT) EURAUD (+0.37%) broke 20- and 50-day SMA, spiking to 1.5562 high so far. Faster MAs stabilised and are flattened currently, as RSI after the 70 high is pulling back despite the bullish bias in the MACD histogram. Hence the intraday indicators suggest the end of the rally for the time being. H1 ATR 0.00185, Daily ATR 0.00911.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.