Market News Today – USD remains weak (USDIndex down to 90.00). Equities closed down 0.25%; USA500 4163. Asian markets stronger. Commodities tear continues, GOLD tests $1870, USOil tests $66.50. 10-yr Yields pick up to 1.64% despite USD weakness. BTC holds at $45,000. Overnight – Kaplan – “no expectation of rate rises until next year”, RBA minutes “wages would likely need to expand “sustainably above 3%” to generate inflation” (currently at 1.4%) – AUD bid. JPY weaker following – Q1GDP missed (-1.3% vs -1.1%). UK Labour Market Report – better than expected but Earnings slip.

This week – Economic data slim, (FOMC Minutes) Earnings from Walmart, Vodafone, Home Depot, Target, Lowes and Cisco.

EUR – up to 1.2185, JPY struggles to hold over 109.00, Cable rallies to 1.4165 AUD pushes ahead to 0.7800 and CAD under 1.2100 to 1.2025 lows.

USOIL over $66.00 and testing $66.50 from lows at$63.00 on Thursday, Gold – rallied to 3.5 mth high $1870. Commodities remain robust. BTC tested under $42,000 again late yesterday, back to $45,000 now. VIX down 4.55% under 19.00 at 6-day lows

European Open – The June 10-year Bund future is a tad lower, but in cash markets the U.S. 10-year rate has corrected -0.7 bp to 1.64%. Stock markets across Asia bounced back and DAX and FTSE 100 futures are currently posting gains of0.6% and 0.8% respectively, outperforming versus U.S. futures, which have also moved higher, though. Inflation and virus developments remain in focus and markets will watch the Fed’s minutes this week for further guidance on the assessment of price pressures. U.K. labour market data showed a sharp decline in the claimant count for April, while the March headline rates reported an unexpected dip in the ILO unemployment rate and a sharp rise in employment. The latter is of course a reflection of the gradual re-opening of the economy. Looking ahead, there are reports of labour shortages, particularly in the hospitality sector, party due to the impact of Brexit and if that translates into higher wage growth, the rise in prices that so far is mainly driven by base effects and a temporary surge in demand, could become more entrenched. For the Eurozone that risk seems much smaller, but it will be a challenge to bring down youth unemployment in particular and avoid cliff edge scenarios once official labour market programs are being phased out.

Today – EuroZone Flash GDP (2nd), US Building Permits and Housing Starts, ECB’s Lagarde, BoE’s Bailey, Broadbent, Ramsden, Fed’s Bostic, Kaplan. Earnings from Generali (a beat) Vodafone, Imperial Brands, Walmart, Home Depot

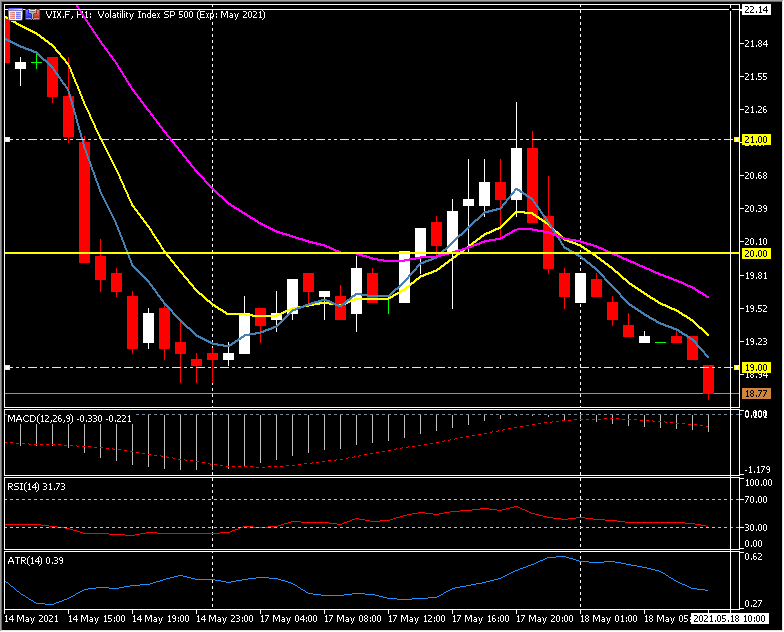

Biggest Mover @ (07:30 GMT) VIX.F (-4.55%) rejected 21.00 yesterday and broke 20.00 and 20HR MA into close, under 19.00 now. Faster MAs remain aligned lower, RSI 31 & moving lower, MACD histogram & signal line aligned lower having rejected 0 line into close yesterday. Stochs falling and in OS zone from earlier. H1 ATR 0.39, Daily ATR 2.33.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.