USDCAD & USOil, H4

Canada’s GDP grew at a 5.6% pace in Q1, undershooting expectations following the 9.3% clip in Q4 (revised from 9.6%). However, GDP was 0.3% firmer compared to Q1 of 2020 as the economy has rebounded from the huge drop in Q2 of 2020.

Of course, prices have picked up, with the GDP implicit price index climbing 2.9% in Q1, led not surprisingly by higher prices for construction materials and energy goods. Housing investment continued to grow at a strong pace, supported by very favorable financing conditions and the recovery in the job market. The return of restrictions in April and May is expected to leave the economy with little growth during the quarter (we see a 0.5% gain in Q2, with risk for a flat or even negative reading). The BoC is likely to look through the slump in Q2 as vaccinations have ramped up, consistent with a resumption of the recovery in the second half of this year. The monthly GDP report revealed a jump to 1.1% growth in March, a bit faster than expected, from the 0.4% pace in February, consistent with strong growth going into the return of restrictions in April.

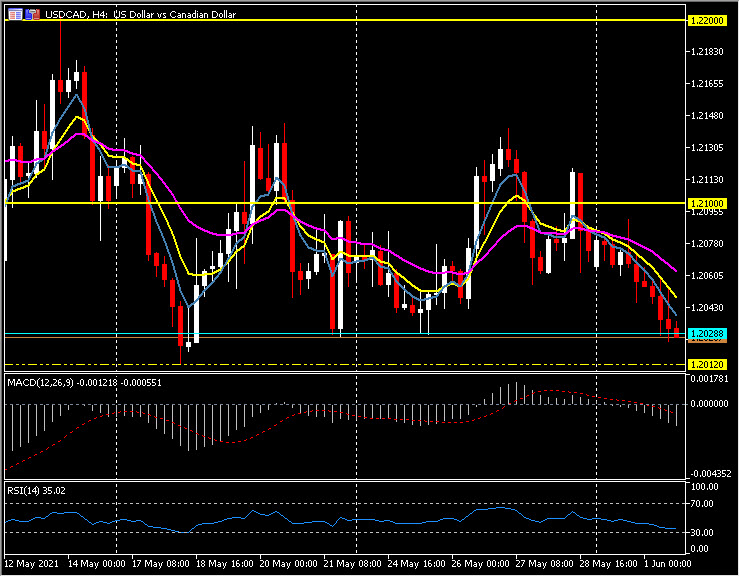

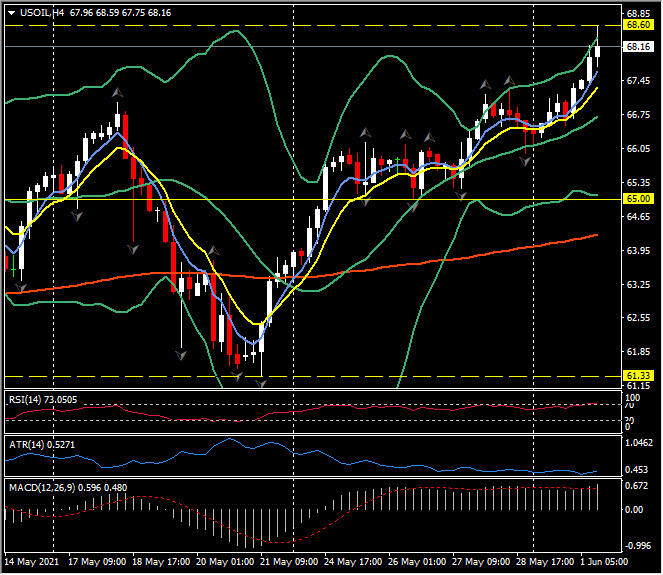

USDCAD was little changed following the miss in Q1 Canada GDP, though remains near two-week lows of 1.2025 printed at the North American open. Two-plus year highs in USOil has supported the CAD today, as prices topped over $68.60, while overall, the USD remains on the heavy side. USDCAD‘s six-year low of 1.2012 seen on May 18 is the next support level. A break below there brings the May, 2015 low of 1.1920 into focus.

USOil rallied to levels last seen in October of 2018, topping at $68.60, up from Monday’s low of $66.69. Improving demand, as economies reopen has supported prices of late, as OPEC+ says surplus inventories will be burned off over the next month or two. The cartel is expected to gradually relax production caps through July, which could limit price gains going forward. Iran is the wild card, and should sanctions on the country’s oil exports be lifted, upwards of 2.0 mln bpd could hit the market later in the year, likely to put renewed pressure on prices, as we saw in late-May when the Iranian news first emerged and prices spiked lower to $61.33.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.