Market News Today – The markets characterized the May US jobs report as Goldilocks –neither too hot, nor too cold. Indeed it was just right for bond and stock bulls. Treasuries rallied with a burst of short covering as the smaller than expected headline job increase pushed a Fed tapering further out the calendar. The steep drop in yields was very favorable to Wall Street, and especially the USA100. Today stock markets traded narrowly mixed amid disappointing trade data out of China and with investors keeping a close eye on comments from Treasury Secretary Yellen, who urged President Biden to press ahead with spending plans ($4 trillion/year), even if they may fuel inflation, while saying that a “slightly higher” interest rate environment would be a “plus”. China trade data showed weaker than expected export growth, but a jump in imports to the highest since 2010.

G7 – agreed to a global minimum tax of at least 15% on multinational companies but faces a rocky path to implementation. (The Biden administration could win support for its US tax increases). The deal give countries more authority to tax the profits of digital companies like Apple Inc. and Facebook Inc. that dominate global markets but pay relatively little tax in many countries where they operate.

European Open – The Sep 10-year Bund future is little changed, as are US futures, while in cash markets the US 10-year rate has lifted 2.0 bp to 1.57%. EGBs are also likely to move up from the lows seen in the wake of the US payroll number on Friday. With fiscal support being stepped up and the recovery strengthening, the pressure on central banks to take the foot off the accelerator is getting stronger and flexible QE schedules may become more of a thing especially for the ECB, which will be meeting on Thursday. The ECB is expected to move away from its commitment to “significantly” higher monthly PEPP purchases. GER30 and UK100 futures are currently down -0.2% and up 0.04% respectively, while US futures are fractionally lower.

Covid will remain on the regional radar again this week, as cases in several countries continue to rise, causing economic restrictions and factory closures. Thailand and Vietnam have been hit by fresh outbreaks, while Malaysia last week put a total lockdown in place. The restrictions will ultimately impact incoming data in the region.

Today – Today’s slate includes Japan’s Q1 GDP, current account, PPI and the MoF business outlook survey. Supply is a focal point in the week ahead with the $120 bln in coupon auctions. Today‘s rally in Treasuries reflects little fear. Ironically, the richening may work to diminish demand. Markets will also digest the G7 agreement on tax payments of big firms today.

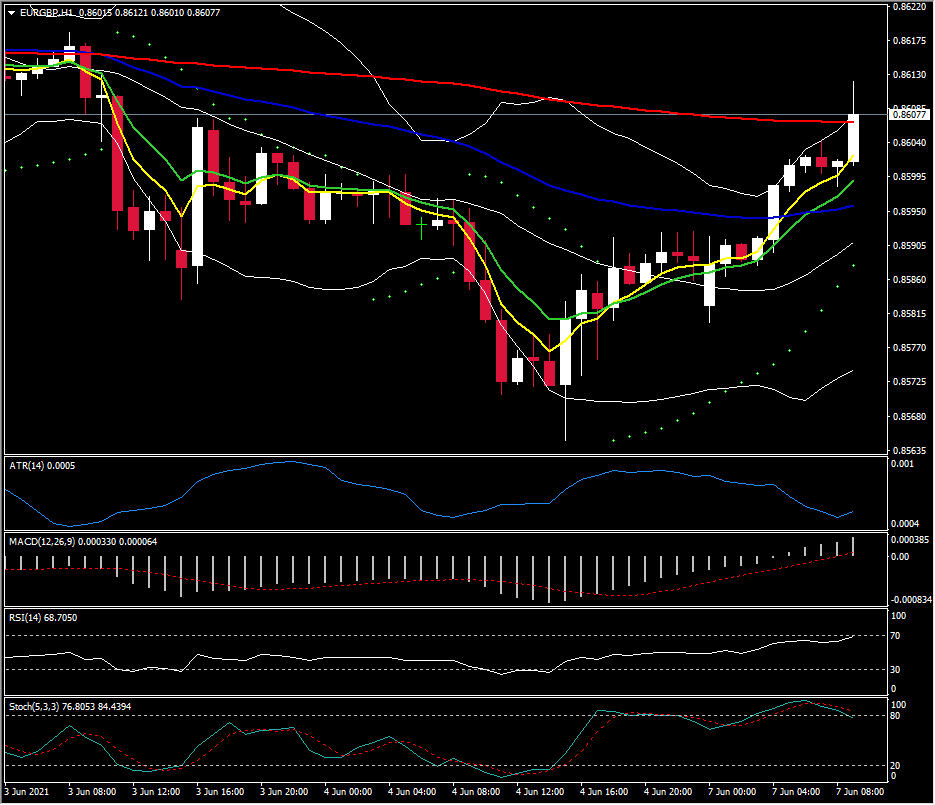

Biggest FX Mover @ (07:30 GMT) EURGBP (+0.49%) has moved up from its 2-month floor at 0.8560. Faster MAs remains aligned higher, RSI 68 and spiking higher, MACD signal line and histogram rising but signal remain at 0. Stochs turning lower from OB zone. H1 ATR 0.0005, Daily ATR 0.0041.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.