Market News Today – Gilt yields closed higher after stronger than expected US inflation numbers, while Eurozone bonds, in particular BTPs, got a boost from the ECB announcement, which affirmed the commitment to keep monthly PEPP purchases “significantly” higher than at the start of the year. The ECB is essentially in wait and see mode and seems to be focusing very much on the outlook for the travel and tourism sector against the background of new virus variants. Central banks successfully convinced markets that the spike in inflation is transitory and after the spike in US inflation yesterday, the Eurozone May inflation round will likely look tame by comparison.

In Asia, Australia and New Zealand bonds found buyers, but in South Korea bonds extended losses after comments from the central bank’s chief economist on normalizing policy. For now the factors driving the jump look transitory, but there are some lingering concerns that it could become entrenched and there was talk that central bankers willdiscuss tapering at the Jackson Hole meeting over the summer.

In Europe, the bunch of data releases out of the UK at the start of the session was largely bond friendly, despite monthly GDP being a tad weaker than expected at 2.3% and industrial and manufacturing production unexpectedly dropping -0.3% and -1.3% respectively. The visible trade deficit meanwhile remains sizeable at around GBP 11 bln.

In FX markets the Yen struggled and USDJPY lifted to 109.42, while the EUR strengthened and EURUSD is at 1.2192, while Cable is little changed at 1.4182. Stock markets mostly managed slight gains as markets continued to digest the uptick in US inflation. JPN225 is up 0.04%, GER30 and UK100 futures are still up 0.1% and 0.2% respectively and US futures are also higher, led by a 0.11% rise in the USA100. USOIL is at $70.14 per barrel.

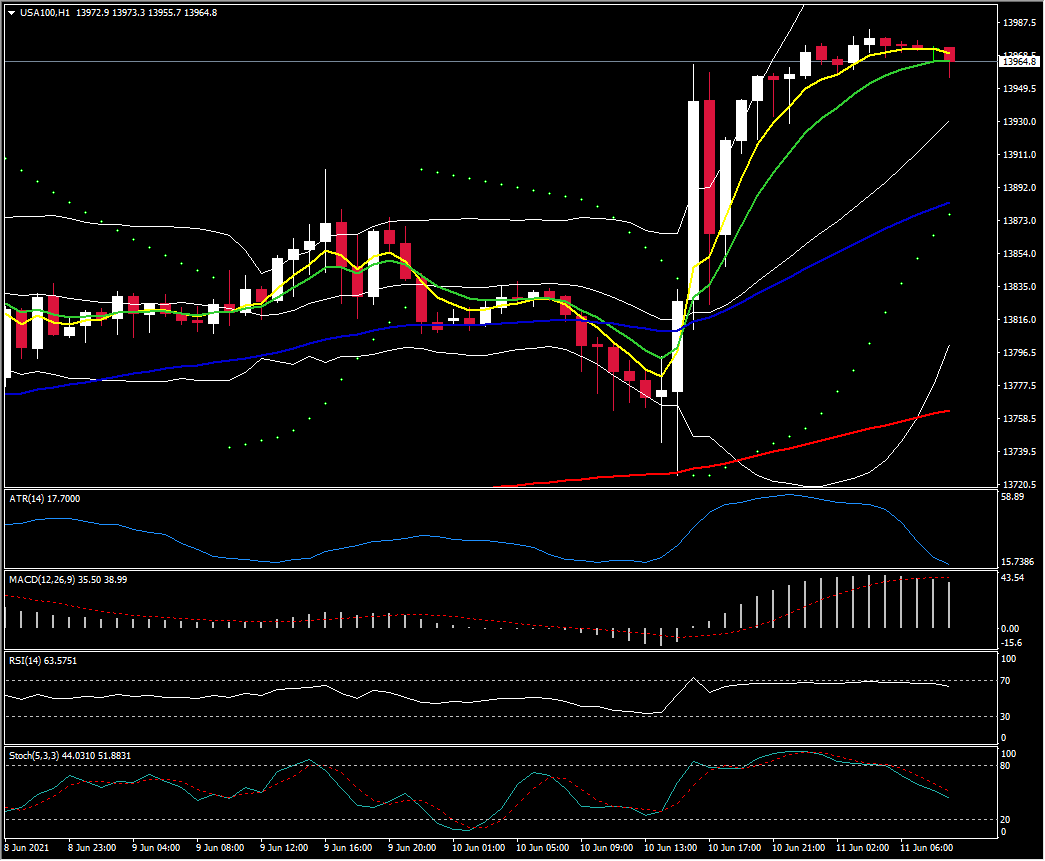

Biggest FX Mover – USA100 just a breath below 14k. Currently the rally has stalled, with fast MAs flattened along with RSI at 63 while Stochastic is sloping lower pointing to 20 barrier. ATR (H1) at 17.70 and ATR (D) at 142.70.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.