USDCAD & USOil, H1

The Dollar firmed up, rebounding after weakening on Friday. The USDIndex lifted out of a six-day low and pegged a high at 92.37, which reversed over half of Friday’s decline but has since declined to 92.20. EURUSD concurrently ebbed to a low at 1.1835 after opening near 1.1880 and now trades around 1.1850. The dollar’s ascent came with the 10-year Treasury yield ebbing by some 2 bp, to sub-1.340% yields. The demand for both the Dollar and Treasuries reflected a safe haven bid, with stock markets sputtering in Europe while US index futures corrected from the record highs that were seen on Wall Street on Friday. Stock markets in Asia, aided by China’s trimming of bank reserve requirements (announced on Friday), still managed to gain after posting their worst week since April. Japan’s Nikkei outperformed, for instance, rallying by over 2% out of the two-month low that was printed on Friday. But the overall vibe in global markets has been one of weariness

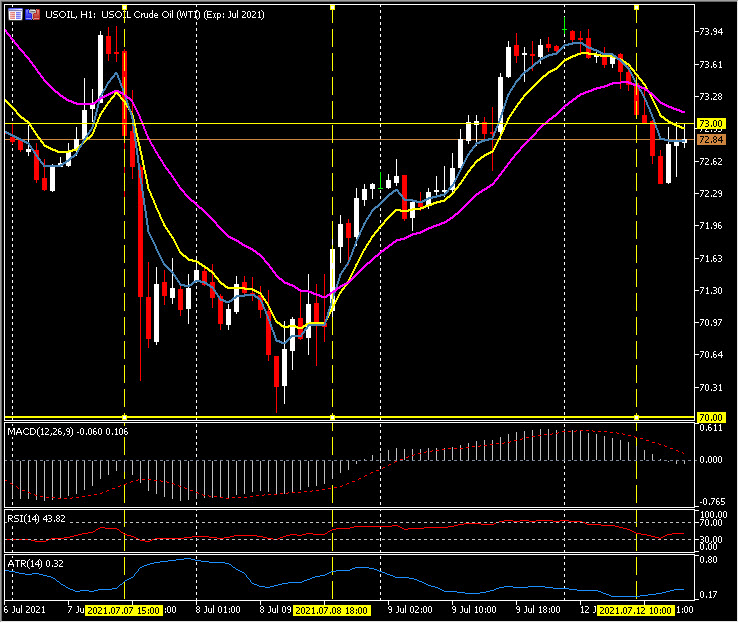

Industrial commodities declined, and oil prices were showing a decline of over 1.5% during the European session. USOil trades at $72.90 in early NY trade after testing $74.00 in during the Asian session and triggering lower on the Crossing EMA strategy, touching $72.35 during the European session. The major price driver now appears to be the rise of Covid cases globally, the Delta variant in particular, and its potential impact on global demand. Current relative price weakness has come despite declining oil stockpiles, and uncertainty over OPEC+ intentions on production levels. OPEC talks on output broke down last week, after Saudi Arabia and the UAE fought over output levels. With no new talks scheduled, the point may come where some producers walk away from current production caps and open the spigots. For now, last Thursday’s three-week low and test of $70.00 provides support.

Concurrently, the USDCAD has rallied from Friday’s close below 1.2440, to trigger higher on the crossing EMA strategy touching highs of 1.2514, before retracing below 1.2500. The risk backdrop is largely on the risk-off side of the equation as North American markets open. The Bank of Canada’s rate announcement on Wednesday is the focus this week. Markets are anticipating a further cut to QE as the bank unwinds the emergency policy setting amid a recovering economy. The solid rebound in June employment, revealed last Friday, added to the already solid case for further trimming of accommodation. Hence, the BoC is expected to taper another C$1.0 bln, which would leave QE totals at C$2.0 bln. Such an outcome is likely to support GoC yields and the CAD, as the Fed remains in the “talking stage” with regards to QE tapering.

The combo of lofty asset valuations, plateauing economic growth across major economies and the Delta-variant driven rise in new Covid cases have remained a collective bugbear for investors, offsetting expectations for ongoing uber-accommodative policies at most central banks.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.