The downside risk to consumer inflation in Turkey could give banks the leeway needed to start an easing cycle in the 4th quarter. However, the risk of rising global inflation is expected to increase as cheap central bank funds start chasing fewer goods. This would prompt the central bank to start raising interest rates or initiate an early reduction of the QE program, thus putting TRY in a difficult position.

The Central Bank of the Republic of Turkey kept the one-week repo rate at 19% during its July meeting, as expected, ahead of possible inflation volatility over the summer as reopenings and high inflation expectations continue to pose risks to pricing behavior and the inflation outlook. Taking into account the inflation rate and high inflation expectations, the current tight monetary policy stance will be firmly maintained until a significant decline in the April Inflation Report forecast path is achieved. CBRT is likely to continue to firmly use all available instruments in pursuit of its primary goal of price stability. The policy rate will continue to be set at a level above inflation to maintain a strong disinflationary effect until strong indicators point to a permanent decline in inflation and the medium-term target of 5% is achieved.

Turkey’s economy grew 7% year-on-year in Q1 2021, beating market forecasts of a 6.7% rise. This was the strongest growth in 3 years, driven by industrial production and other key sectors which have recovered well from the hit of the coronavirus as most restrictions were lifted in March. Faster gains were seen for manufacturing (12.2% vs. 10.5%) and services (5.9% vs. 4.6%) and construction (2.8% vs. -12.5%) rebounded. In addition, the information and communication sector recorded the largest growth in the quarter, jumping 18.1% (vs 15.1%). However, the strict lockdown imposed at the end of April is likely to disrupt economic activity in the second quarter. On a quarterly basis, the economy grew 1.7%.

Technical Level

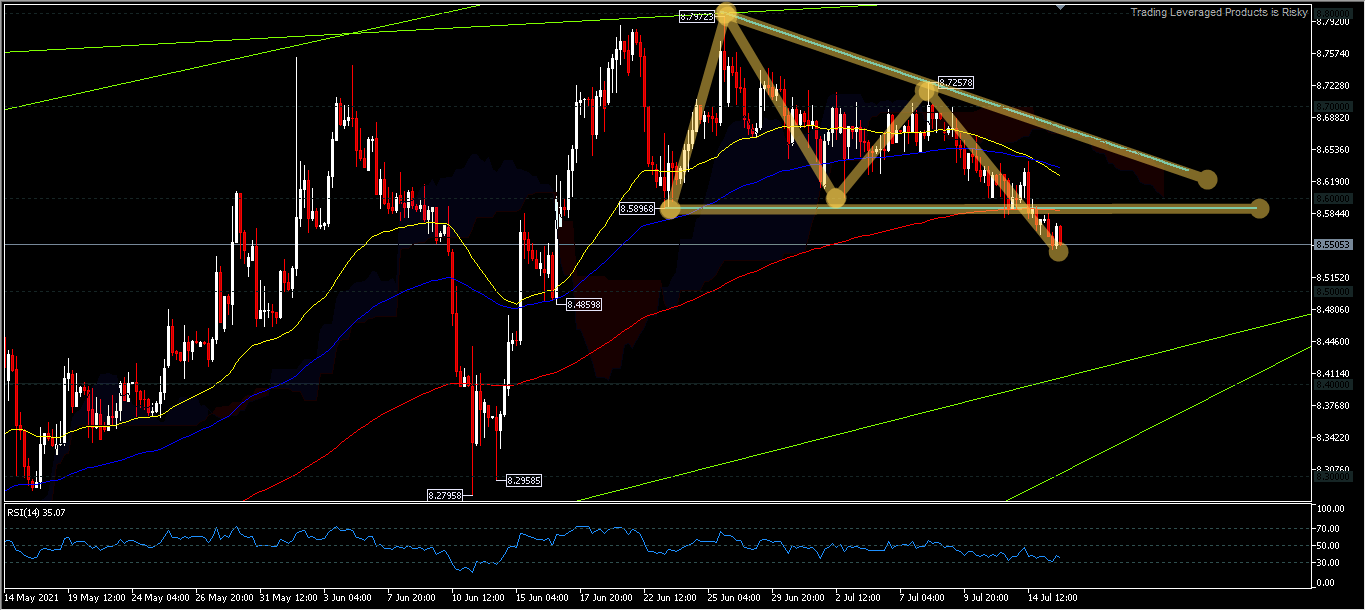

During the 2nd Quarter of 2021, TRY was the worst performer against USD with a decline of 17.6% and scored an ATH peak of 8.7972. CBRT, as expected, left the 1-week repo rate unchanged at 19%. As a result, USDTRY continues its corrective move. The asset formed a descending triangle from the second peak of 8.7257 after successfully crossing the 8.5896 support. The next corrective move will target the 50-day MA around 0.8500, but the price is still just above the Kumo although supported by the RSI entering 44.88 levels.

USDTRY, H4

The intraday bias is seen towards the downside, as the price surpassed the support, which was confirmed by Kumo moving below the 200-period SMA. The corrective movement could continue targeting the 8.4859 and 8.2825 support. However if there is a failure to decline further, the support level 8.5896 which was previously broken will become resistance with further strengthening to 8.6405. Overall the trend still tends to be bullish.

Click here to access our Economic Calendar

Ady Phangestu

Analyst – HF Educational offfice – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.