Wall Street losses persisted through the Friday session, with the major indices all ending lower. Stocks got a brief boost from the stronger US retail sales data, though the dive in consumer sentiment, including upped inflation concerns, took the wind out of the rally’s sails.

Today, in the Asia session and on European open:

- The 10-year Treasury yield was down and bonds were also supported, with Australia’s 10-year down -4.4 bp at 1.233%, as stocks were hit by growth concerns.

- The September 10-year Bund future is up 42 ticks at 175.29, outperforming versus Treasury futures. GER30 and FTSE 100 futures are down -0.6% and -0.8% respectively.

- Reuters – Japan kept the overall assessment of its economy unchanged for a second straight month in July, retaining the view that conditions remain severe due to the impact of the coronavirus pandemic.

- Tech stocks struggled. – China’s crackdown on Tech giants Alibaba, Baidu, JD.com and Pinduoduo extending low amid new anti-monopoly and data security rules in China.

- Reports of issues with Japan’s supply chain have been noted, with suppliers in countries such as Malaysia, Thailand and Vietnam falling behind on production due to Covid shutdowns.

- Zoom Video Communications Inc ZM.O, the videoconferencing service that became a household name globally during the pandemic, plans to parlay some of the resulting rise in its share price into a $14.7 billion acquisition to secure growth.

- Oil prices declined on oversupply worries – OPEC and its allies agreed to ease output restrictions and supply cuts, including Russia which agreed new production allocations and a gradual phasing out of supply cuts, that will increase supply by around 400K barrels.

- Focus will remain on the Covid spread around the region with the Delta variant continuing to cause worries.

FX markets: In FX markets the Yen was supported by safe haven demand, and USDJPY dropped back to 109.84, although the Dollar climbed against most other currencies. EURUSD is little changed at 1.1803, while Cable dropped to 1.3746. AUD hit its lowest level in 2021, at 0.7372. USOIL stayed at the $70.60-$71.60 barrier. Gold edged higher, lifted by a retreat in US Treasury yields and concerns that a surge in coronavirus cases could dampen global economic recovery, though an uptick in the Dollar limited the safe-haven metal’s appeal.

Today – The calendar is pretty empty to start the week, hence growth concerns are dominating and developments will add to expectations that the ECB will strengthen the dovish tone of the forward guidance at Thursday’s council meeting.

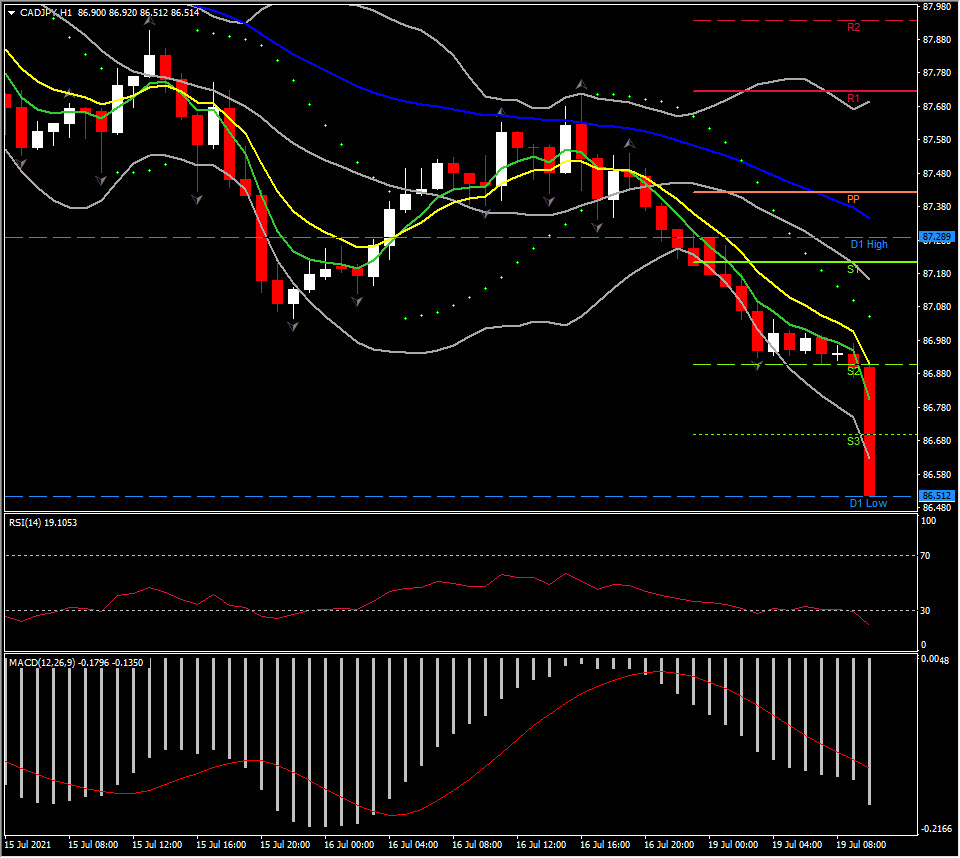

Biggest mover @ (8:30 GMT) CADJPY (-0.66%). The Yen was supported by safe haven demand, while CAD dips on USOIL weakness. An aggressive selloff of CADJPY broke all Support levels for the day with next Support at 86 and 200-day SMA at 85.78.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.