")

Market News Today

- RBA leaves rates unchanged – but surprises by extending AUD 4 bln/week Bond purchases until February (from November)- “Delta outbreak is expected to delay, but not derail, the recovery”. No rate hikes expected until 2024 (no change). AUD spiked on no change to 0.7468, down to 0.7410 on Bond news, back to 0.7425 now.

- USD (USDIndex 92.18) continues to hold over 92.00

- Yields ticked up; as Treasuries slipped, (10yr 1.34%)

- Equities pushed higher in Asia Nikkei +1.3% again to today on expectation of more stimulus & JPY data, (Earnings & Leading strong, big slip for Household spending). – USA500 FUTS at new highs 4548 earlier)

- USOil recovers from $68.00, back to $69.00 now, on positive news from Asia session.

- Gold slips to $1816 now, from 1828 yesterday & 1833 on Friday.

- Overnight – Major beat for Chinese trade, exports in particular pushing trade surplus over $8bn better than expected. ($58bn vs 50bn). German Industrial production & CHF Unemployment inline with expectations.

Military coup in Guinea (one of the world’s biggest suppliers of bauxite, a necessary component of aluminium) – saw aluminium at its highest in more than a decade due to supply concerns.

European Open – December 10yr Bund future down -7 ticks at 172.29, with Treasury futures underperforming slightly. DAX & FTSE 100 futures down -0.1% & -0.2% respectively, indicating a lower open for European markets. RBA decision to stick to taper plans, albeit extending the time frame, should not dent the likely ECB move to scale back monthly purchase volumes closer to those seen in Q1. That would still mean sizeable support & Lagarde is likely to sweeten the pill with an affirmation of the very dovish guidance on interest rates. EURUSD & Cable at 1.1864 & 1.3825 respectively. USDJPY at 109.92 from Monday’s low at 109.68.

Today – German ZEW Survey, EZ Revised GDP and Final Employment, ECB weekly purchases. Government treasuries from the UK, Germany and the US.

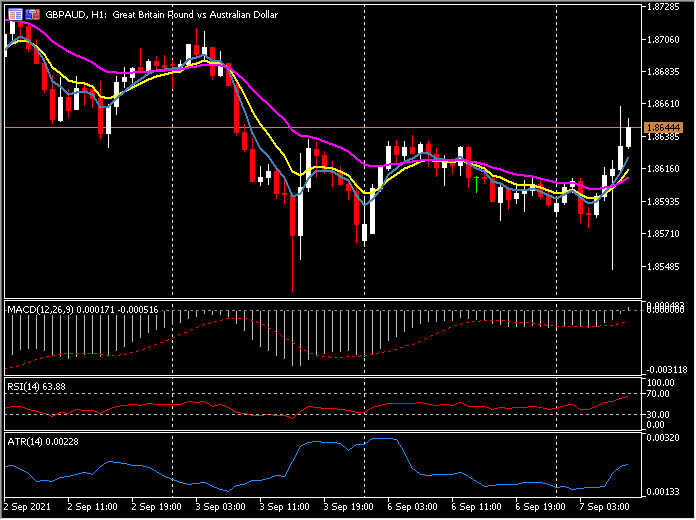

Biggest Mover @ (06:30 GMT) GBPAUD (+0.32%) All AUD pairs volatile on surprise from RBA, 1.8550 to 1.8650. Faster MA’s aligned higher, MACD signal line & histogram breaking above 0 line and rising. RSI 63.88 and rising. H1 ATR 0.0023, Daily ATR 0.0112.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.