- Q3 earnings season has gotten off to a strong start, with big banks largely shooting the lights out on revenues and earnings.

- Incoming data was constructive as well, with jobless claims coming in at pandemic lows, while the rate of PPI growth slowed. All 11 S&P sectors are higher.

- Bulls are in control, both in the bond market and on Wall Street. – Overlooked the hawkish Fed implications from the record strength in PPI and the lowest claims readings since before the pandemic.

- Yields declined and Treasuries are in the green on short covering and dip buying, recovering from the recent aggressive selloff. US Treasury yield has lifted 1.8 bp to 1.53%.

- China: will loosen restrictions on home loans and boost lending & bank added enough medium term funds to keep liquidity in the system steady.

- Equities up. JPN225 managed a 1.6% gain and US futures are also higher, led by a 0.4% rise in the USA100.

- Oil lifted above $81.99. – Prices quickly backed up after a larger than expected stock build in the US.

- Improved market sentiment, which has lifted global stocks, commodity prices and bond yields, is also weighing on the safe-haven Dollar.

- FX markets – USD dropped, Yen declined.

- EURUSD retests 1.1600 mark, Cable at 1.3689, USDJPY touched 114.16.

European Open – The December 10-year Bund future is slightly higher, US Treasury futures slightly in the red, as stock futures move higher in both Europe and North America after a good session for equities across Asia overnight. Market sentiment improved and GER30 and UK100 futures are currently up 0.4% and 0.3% respectively, while a 0.4% rise in the USA100 is leading US futures. EGB yields had dropped back markedly yesterday, but in the UK money markets are still bracing for an earlier than expected lift off on rates, which ironically is actually helping long rates to come down.

Today – Today’s data calendar is unlikely to change the overall picture, with only eurozone trade data for August and some final HICP readings on the agenda.

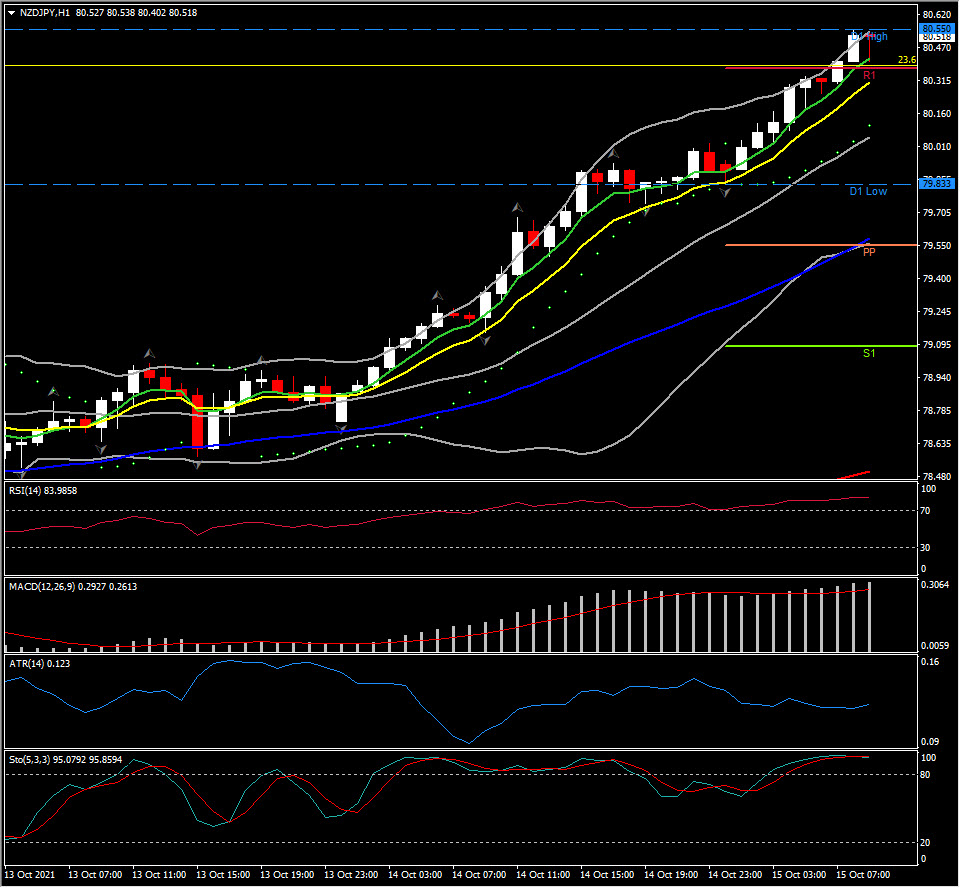

Biggest FX Mover @ (06:30 GMT) NZDJPY (+0.60%) Breached 80.55. Up for 7 days in a row. Currently faster MAs keep pointing up, MACD signal line is at 0 & histogram trending higher. RSI at 82 & Stochastic at 94 but both sloping down, all indicating further upwards move in the medium term but possible pullback in the short term. H1 ATR 0.123, Daily ATR 0.810.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.