- RBA confirms end of yield curve targeting and after abandoning any attempt to defend the 0.1% for the April 2024 yield last week, the bank confirmed today that the yield target has been ditched and opened the door for an earlier interest rate hike.

- Lowe stressed that the bank will see through spikes in the inflation rates, and that unlike elsewhere the RBA sees a further, but gradual increase in core inflation, as there is a lot of inertia in the labour market, which makes it hard to see inflation accelerating too quickly.

- Australian shares fell on Tuesday – Miners and banks worst performers

- AUD tanked as markets adjusted rate hike bets. AUDUSD at 0.7465 from 0.7533.

- US Yields were off their early highs (Currently 10yr fractionally higher at 1.56% compared to the day’s peak at 1.603%).

- USD (USDIndex 93.80) down as US futures in the red after a largely weaker session in Asia despite the strong earnings season. Overnight prices wobbled after the Manchin remarks and mixed data, but all rallied into the close. (A beat from the ISM, but a miss on construction spending, though they still modestly boosted growth prospects).

- The USA100 climbed 0.63% to 15,595, while the USA500 was 0.18% firmer at 4613, while the USA30 advanced 0.26% to 35,913. Treasury revised Q4 borrowings higher to $1,015 bln, with $650 December 31 cash balance, and $476 bln borrowings for Q1 2022. GER30 and UK100 futures are down -0.17% and -0.21%, respectively.

- Senator Manchin continued to oppose a quick vote on President Biden’s massive spending plans, saying he will not vote on a reconciliation package without knowing more about its impacts. He worries over programs that “irresponsibly” add to the debt, which totals over $29 tln, and which risks hurting families that are suffering from “historic inflation.” He said holding the infrastructure bill “hostage” will not get his support for reconciliation.

- USOil topped at $83.05, on slow OPEC oil output increase & China ramped up operating rates to meet a spike in diesel demand.

- Gold – up to 1796.30 again.

- FX markets – AUD sold off, Yen strengthened – EURUSD little changed at just over 1.1605, GBPUSD dropped back to 1.3630. Markets are concerned that an early lift off in rates could hamper a still fragile economy.

Today – Data releases today focus on final manufacturing PMIs for the Eurozone, which were delayed by the public holiday in parts of the region yesterday and employment data from New Zealand.

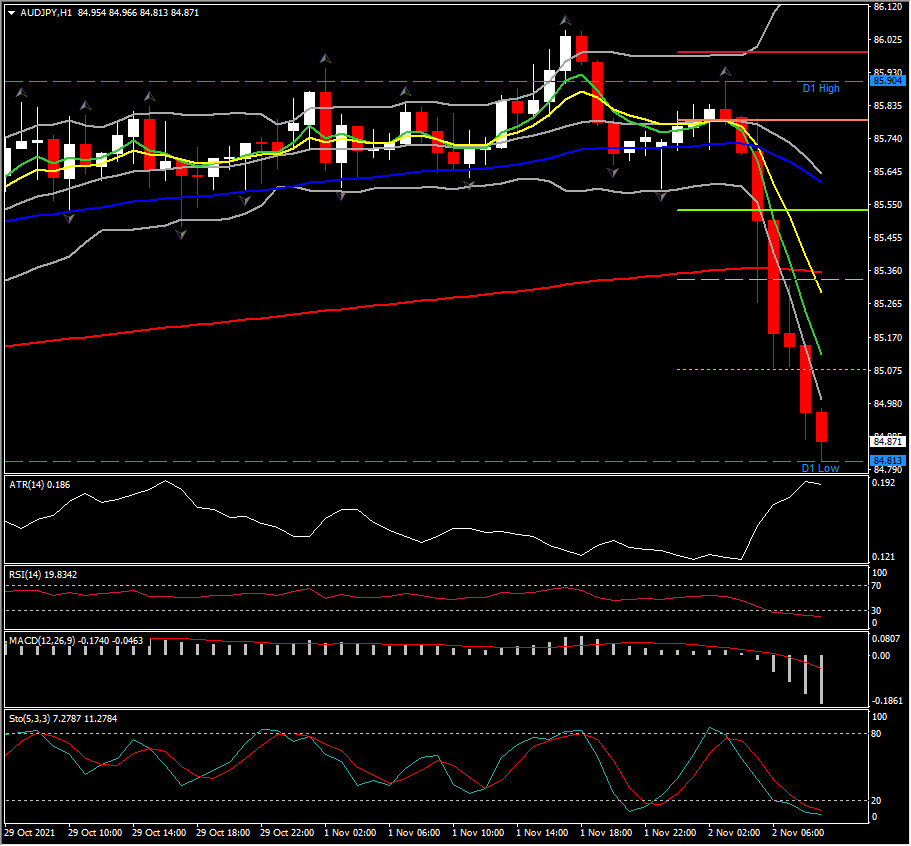

Biggest FX Mover @ (06:30 GMT) AUDJPY (-0.94%) dips to 1-week lows from 85.90 to 84.80. Faster MAs steadied, MACD signal line & histogram are sharply lower in negative territory, RSI 20 and neutral. H1 ATR 0.186, Daily ATR 0.806.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.