- A global rally in bonds helped knock Treasury rates lower as the markets repriced central bank outlooks, paring some of the more aggressive views on rate hikes. The moves across Treasuries, EGBs, and Asian bonds were precipitated by the RBA’s ending of YYC and push back against expectations for a 2022 tightening.

- Fears of an aggressive FOMC in 2022 were also pared, as were worries over a BoE rate hike as soon as Thursday. – US Yields lower (10yr rate fell to 1.54%).

- USD (USDIndex 94.00) eased as US futures steadiedafter posting new highs – The USA30 rose 0.39% to 36,053, closing over 36k for the first time ever. The USA500 advanced 0.37% to 4630, with the USA100 0.34% firmer at 15,649. GER30 and UK100 futures are down -0.013% and -0.12% respectively.

- Premier Li Keqiang warned that the Chinese economy faces new downward pressure, amid a pick up in Covid-19 case numbers, higher energy prices and supply problems. A strong China services PMI failed to lift confidence.

- USOil down at $81.18, amid some encouraging comments ahead of the OPEC+ meeting, which supported hopes that there will be some sort of agreement on higher outputs after all.

- Tesla’s Elon Musk bemoans German red tape, again – Tesla found a floor at 1145.

- Fired Apple employee files complaint with US labor agency – Apple at 150.00.

- FX markets – USD steady, USDJPY dropped back to 113.82 and AUD and NZD stabilised, after selling off yesterday.

FOMC preview: the Fed will resume its meeting today and announce its decision at 18:00 GMT, to be followed by Chair Powell’s press conference at 18:30 GMT. This meeting does not include the quarterly economic forecasts or dot plots. The announcement of QE tapering is fully anticipated, leaving attention on Powell’s remarks and how he addresses inflation and growth dynamics. We expect he will reiterate the view that inflationary pressures are “transitory,” while acknowledging that prices have been elevated and are likely to remain high but mostly due to the reopenings from the pandemic and supply chain factors. He also should note the slowing in growth as evidenced by the slippage in Q3 GDP to the 2% rate, but again much can be attributed to supply constraints of labor and materials. Powell will not signal any timeframe for rate hikes but will try to downplay risks of a June liftoff while continuing to differentiate tapering from tightening.

Today – Markets are likely to be cautious ahead of the Fed announcement today and the BoE decision tomorrow. Data releases today include the final UK services PMI, as well as Eurozone unemployment data, ECB Lagarde Speech, US ADP and US ISM PMIs.

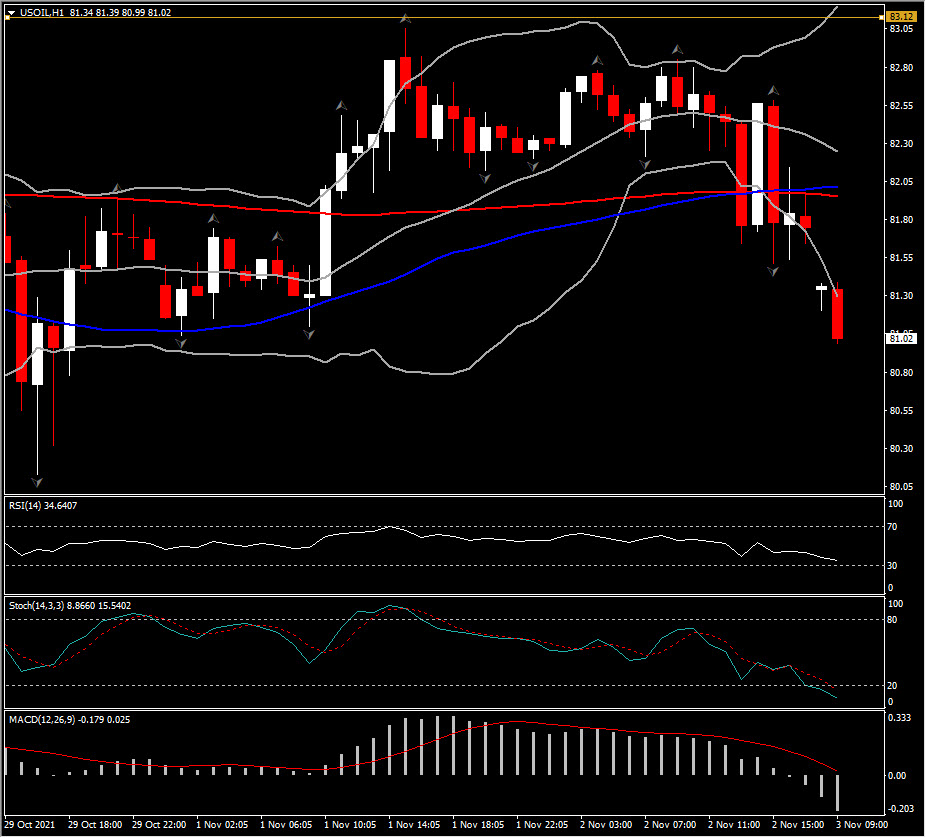

Interesting Mover @ (06:30 GMT) USOIL (-1%) dips below 81 and S1 extending lower BB downwards. Faster MAs aligned lower, MACD signal line & histogram turned negative, RSI 34 and neutral, while Stochastic dipped to 8 and is sloping down. H1 ATR 0.48, Daily ATR 1.95.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.