Receding fears of aggressive policy turns from the Fed and BoE saw shorts scramble to cover with yields plunging as the markets repriced policy outlooks. Although the FOMC announced tapering and the BoE warned of rate hikes down the road, the more patient stance taken by both banks wrongfooted bond bears and forced a repricing of rate expectations.

- USD up (USDIndex 94.40).

- Yields have backed up with the 10-year Treasury yield at 1.53%, but bonds across the Asia-Pacific region still caught up with yesterday’s rally, and the JGB rate is down -1.1 bp at 0.06.

- Equities were mostly firmer Thursday as well, with the USA100, USA500, GER30, and CAC40 all at record highs. – The equity rally started to stall today. Hang Seng and CSI 300 are currently down -1.2 and -0.3% respectively, JPN225 has lost -0.7%.

- China’s rising Covid-19 case numbers and problems in the country’s property sector remained in focus as developer Kaisa Group Holdings Ltd. and its Hong Kong listed units were suspended from trading.

- The RBA’s quarterly policy statement with updated projections sounded upbeat on the recovery, but cautious on wage growth, which backs official assertions that rates won’t rise for a long time to come.

- USOil down at $78 lows after dropping sharply yesterday in the wake of the OPEC+ agreement to stick with the gradual 400K barrels a day increase in production, which boosted speculation that countries will tap their strategic reserves to keep a lid on prices.

- Gold up at 1798 as the falling yields provided support.

- FX markets – USD steady at 94.40 highs, AUD and NZD were under pressure, while the JPY strengthened, leaving USDJPY at 113.61. EURUSD at month low 1.1560 & GBPUSD stabilised at 1.3500.

- USDZAR – dipped early on Friday on elections results, after a volatile week during which it swung back and forth on domestic politics and US monetary policy. – ANC took 46% of the vote, its worst result since taking power at the end of white minority rule in 1994.

Today – The focus turns to the October employment report, where we expect non-farm payrolls to rise 380k versus the 194k in September. Hourly earnings should rise 0.4% after jumping 0.6% previously, while the average work week is seen dipping slightly to 34.7 from 34.8. The unemployment rate is penciled in at an unchanged 4.8%. September consumer credit is due late in the session.

For earnings, reports are due from Berkshire Hathaway, Toyota, Enbridge, Dominion Energy, Johnson Controls, Honda, Sempra, TELUS, Magna International, Ventas, and DraftKings. Next week the refunding auctions are on tap with $120 bln in 3-, 10-, and 30-year paper for sale.

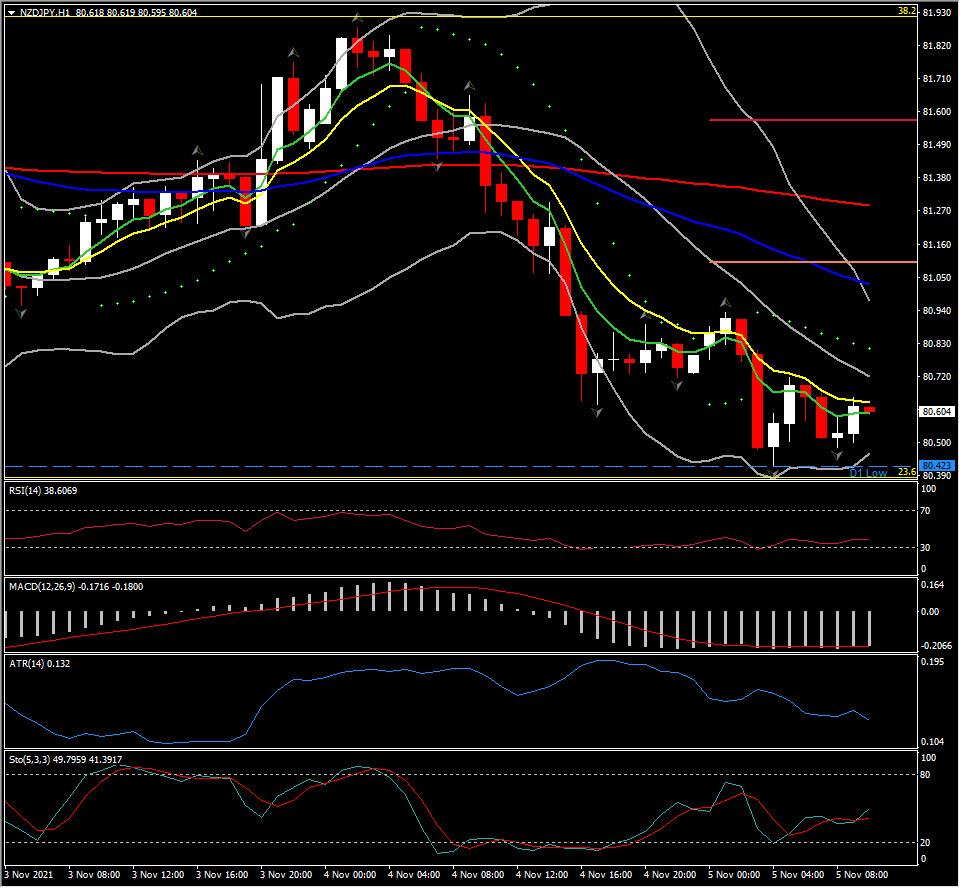

Biggest Mover @ (06:30 GMT) NZDJPY (-0.28%) dipped to 80.43. Faster MAs flattened, MACD signal line & histogram clash but are sharply negative, RSI 38 and neutral, all indicating consolidation for now. H1 ATR 0.133, Daily ATR 0.819.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.