In the foreign exchange market, the US Dollar Index remained range-bound, but was subsequently boosted by Yellen and Bostic’s speeches and closed at 95.97. In addition, the 10-year US Treasury yield rebounded 4 basis points to 1.44%.

In terms of non-US currencies, the Euro hovered around 1.13 against the US Dollar; the British Pound closed up 0.16% to 1.3297 against the US Dollar; the US Dollar ended a 4-day losing streak against the Yen to close at 113.16; the New Zealand Dollar and the Australian Dollar have been hovering at low levels throughout the year and closed at 0.6813 and 0.7091 respectively; the US Dollar and Canadian Dollar remained stable at a high level of 1.28; the US Dollar and Swiss franc continued to test the previous low level of 0.92.

In the precious metals market, spot gold fell below the 1770 level to $1769 per ounce; spot silver held steady above the 8-week low at $22.33 per ounce.

In the oil market, OPEC+ decided to keep the output increase of 400,000 barrels per day unchanged in January next year. US crude oil fell to a minimum of 62.20 US dollars, and then rebounded more than 7% to 67.01 US dollars/barrel.

Key recent events:

The labor market has grown moderately, and the Dollar has regained support and rebounded.

Yesterday, the number of layoffs at challenger companies in the United States in November fell further by 7,947 to 14,875, a record low since May 1993. In addition, as of the week of November 27, the number of initial claims for unemployment benefits recorded an increase of 222,000, which was lower than the market’s expectation of 240,000. After the data was released, its previous value was also revised down to an increase of 194,000 (previously an increase of 199,000). Judging from the four-week average, the number of people applying for unemployment benefits was 238,750, which was lower than the previous value of 251,000 (pre-revision: 252,250).

Overall, these data reflect the continued moderate growth of the US labor market, and may benefit the non-agricultural data that will be released later today. The market predicts that after the November seasonal adjustment, the non-agricultural employment population will record an increase of 555,000, slightly higher than the previous value of an increase of 531,000, the unemployment rate will record a five-month consecutive decline to 4.5%, and the employment participation rate will rebound by 0.1% to 61.7%, the average weekly working hours remained at 5.0%, and the average hourly wage rate and monthly rate increased by 5.0% and 0.4%, respectively.

In addition, the market will continue to track news about the Omicron virus strain. According to foreign media reports, cases of infection with the mutant strain have been found in the states of Minnesota and Colorado. However, despite the fact that Omicron has been pointed out as having a very high transmission capacity and leading to the risk of a further surge in infections, President Biden gave the market a shot in the latest speech and said that the government will not re-impose the lockdown measures. Judging from the known clues, the current Omicron variant is not likely to cause fatal symptoms to most patients (especially those who have been fully vaccinated), but because this new variant is still relatively new, uncertainty remains for now.

In addition, Treasury Secretary Yellen and Atlanta Fed President Bostic were hawkish. The former stated that it would be “prepared to abandon inflation temporarily” and that the strong US economy will prompt interest rate hikes; the latter stated that if inflation stays near 4% next year, the Fed may raise interest rates more than once. The US Dollar Index rebounded on the eve of the non-agricultural report and ended at 96.07.

Today – EZ, UK, US Markit Services PMIs, EZ Retail Sales, US and Canadian Labour Market Reports, US ISM Services, US Factory Orders, ECB’s Lagarde, Lane, BoE’s Saunders, Fed’s Bullard

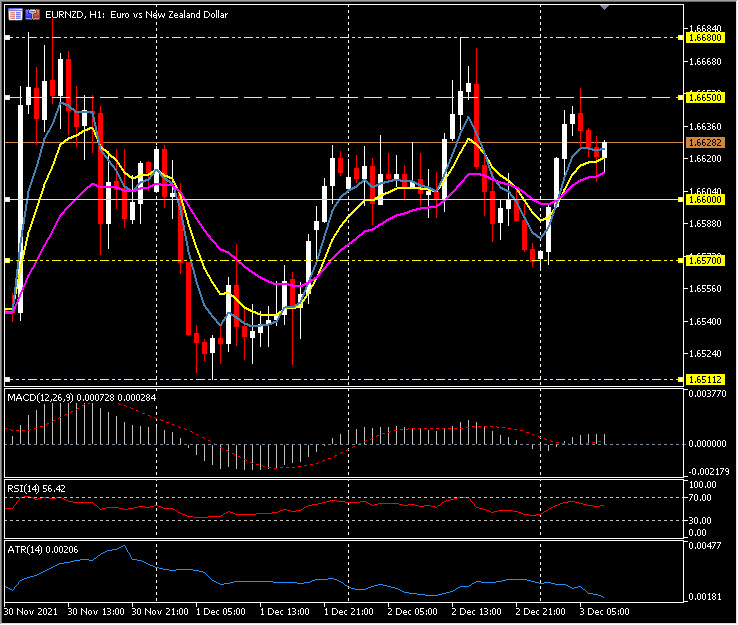

Biggest FX Mover @ (06:30 GMT) EURNZD (+0.32%) From a high @ 1.6680 & slide to 1.6570 yesterday, back to resistance today at 1.6650. Currently MAs aligned higher, MACD signal line & histogram struggle with 0 line, RSI 56 & cooling. H1 ATR 0.0020, Daily 0.0131.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.