- USD (USDIndex 96.15) steady, as Treasuries rose sharply on the improvement in risk appetite on expectations for an acceleration in QE tapering to be announced at next week’s FOMC meeting, and as the market set up for this week’s $112 bln in coupon supply. Stock market sentiment strengthened further overnight and the GER30 and UK100 are posting gains of 0.6% and 0.2% respectively, while a 0.7% rise in the USA100 is leading US futures higher.

- The RBA left policy settings unchanged, but sounded relatively optimistic on the virus front, which for some signalled that an early exit from QE is on the cards.

- Growing confidence that Omicron won’t derail the global recovery, but that also means that central banks remain on course to rein in stimulus as new virus restrictions will likely add to inflation pressures.

- Today’s released UK BRC retail sales were stronger than expected, but may be distorted by warnings that consumers should bring forward Christmas shopping in the light of supply chain disruptions, which could worsen over the winter.

- US Yields 10-year rate lifted 1.7 bp to 1.45% overnight, JGB rates are up 1.7 bp at 0.051% as stock market sentiment continued to improve. Australia’s 10-year jumped 6.5 bp to 1.64%.

- USOil – higher above 200-DMA at $70.60 – concerns about the impact of the Omicron variant on global fuel demand eased, while Iran nuclear talks stalled, delaying the return of Iranian crude.

- FX markets – EURUSD remains below the 1.13 mark, while Cable is still below 1.33 as the FOMC decision comes into view. USDJPY lifted to 113.72, but currently 113.58.

European Open – The March 10-year Bund future is down -50 ticks, underperforming versus Treasuries and leaving Bund yields to jump sharply in catch up trade, after Treasury yields continued to move higher through the Asian session.

Today – The calendar has Eurozone detailed GDP numbers for Q3, but the focus will be on German ZEW investor confidence. In the US session, we have US trade and productivity and Canadian Ivey PMI.

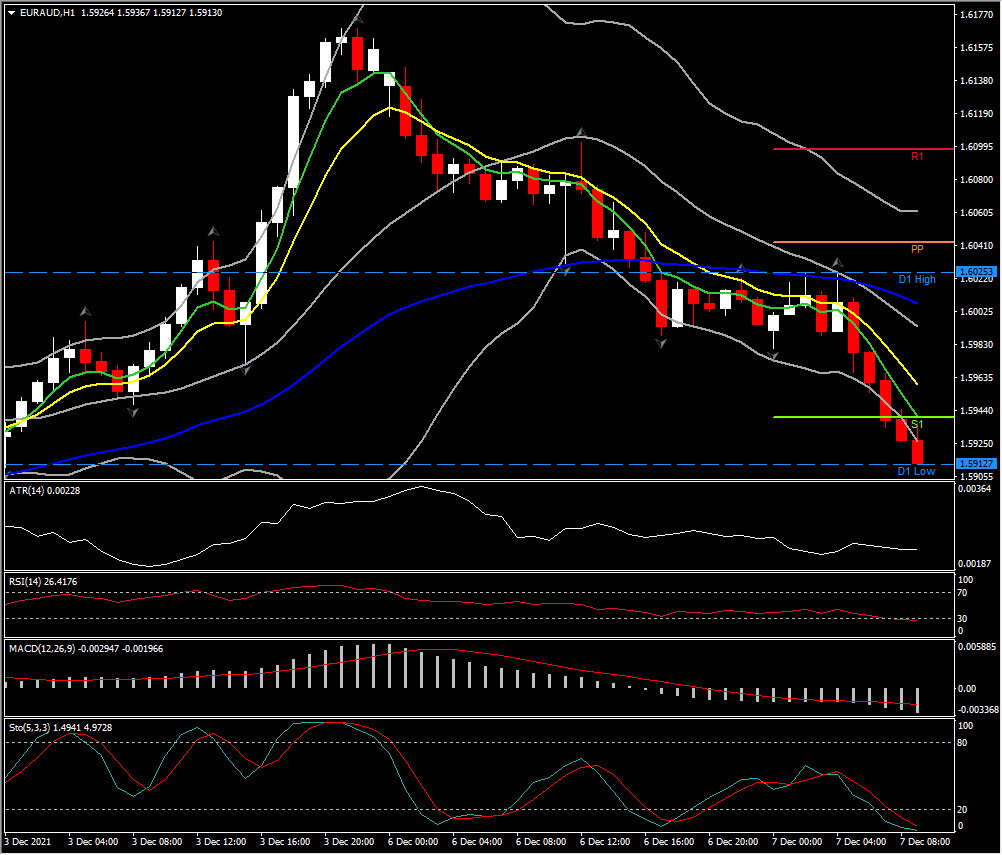

Biggest FX Mover @ (07:30 GMT) EURAUD (-0.41%) Currently MAs are aligned lower, MACD signal line & histogram below 0 and dipping, RSI sloping to 26, Stochastic declines. H1 ATR 0.00226, Daily 0.01442.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.