- USD (USDIndex settled at 96.10) as risk appetite continued to improve, with global stock markets strengthening following Wall Street higher, with Topix and JPN225 posting gains of 0.6% and 1.4%. – The BOJ bought a total of 1.025 trillion yen ($9.03 billion) JGBs.

- Reuters: Intel’s INTC.O announcement of plans to take its self-driving car unit Mobileye public in the United States next year pushed his shares to a 3% gain and cheered chip investors across the board.

- Japan Q3 GDP revised lower with second report. Shoppers seemed to have already tightened their purse strings, leaving overall activity down -3.6% on a seasonally adjusted annualised basis. Business investment wasn’t quite as weak as feared, but the pressure on spending already evident in Q3 may foreshadow the impact Omicron will have on the overall outlook. Supply chain issues are weighing on exports and will continue to weigh on growth in Q4, which is generally expected to be even worse than the third quarter.

- US Yields 10-year rate still dropped -1.0 bp to 1.46% overnight, and JGB rates and Australia yields also corrected, as speculation that central banks will move earlier than anticipated is pushing up short rates, while supporting the long end to some extent.

- The bear flattening trade continues to weigh on Treasuries. The significant cheapening in rates since last month amid rising risks of Fed rate hikes made the maturity a little more palatable. The apparent strength in the economy is also adding to expectations the FOMC will not only announce an acceleration in QE tapering next week, but could also push up rate liftoff to the spring, and potentially hike rates three times in 2022.

- USOil – steadied at $71.00 – Risks: assessment of full impact of the Omicron variant on economy; effectiveness of existing vaccines; US-Iran nuclear talks to resume later this week; US-Russia tension raised as Biden warns Putin of sanctions, Nord Stream 2 disruption if Russia invades.

- FX markets – US Dollar struggled, EUR and Sterling strengthened somewhat against a largely weaker Dollar, leaving EURUSD at 1.129 and Cable at 1.3240. USDJPY pullback to 113.30.

European Open – The March 10-year Bund future is fractionally lower, underperforming versus US futures, while in cash markets the US 10-year rate has corrected -1.4 bp to 1.46%. 2-year yields have moved higher and curves flattened as improved growth optimism is boosting expectations of central bank action as inflation remains high. The Fed has sounded hawkish through the Omicron scare so far and while the doves at the BoE and ECB may want to err on the side of caution next week, the tide on monetary policy clearly is turning.

Today – The European data calendar is pretty quiet today, ahead of German trade data tomorrow and UK GDP numbers on Friday. Hence all eyes today are on BoC rate decision and statement. US Jolts are also on tap.

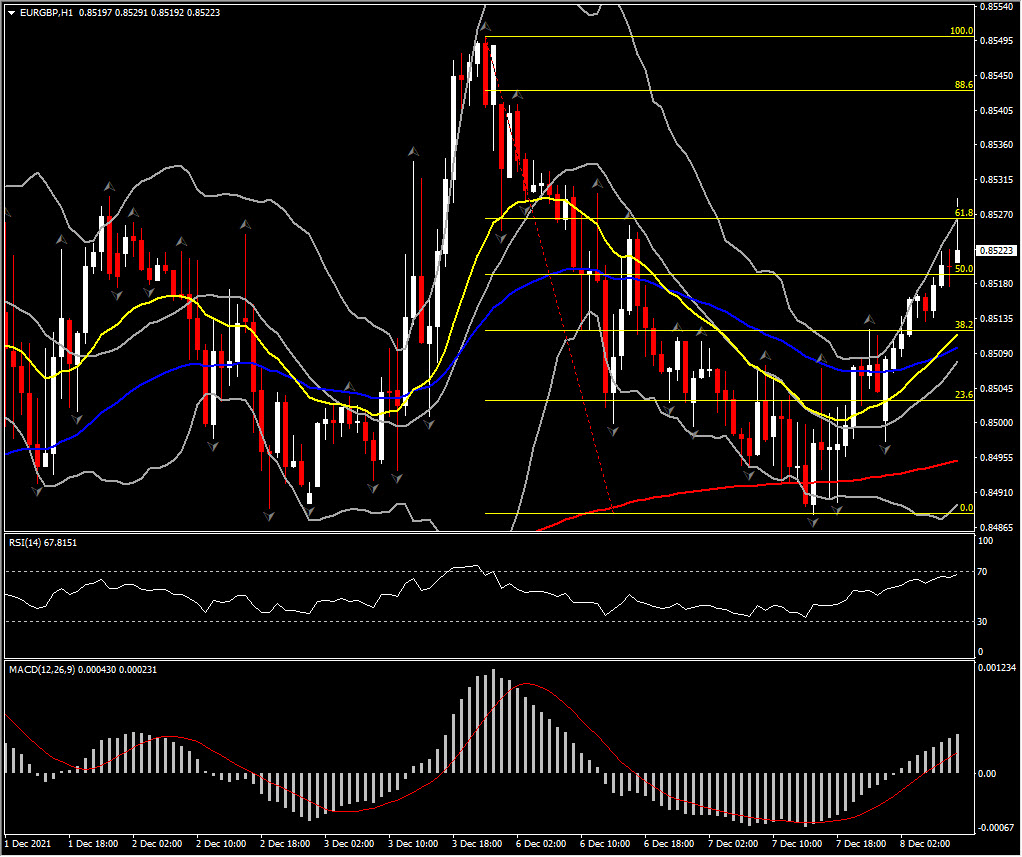

Biggest FX Mover @ (07:30 GMT) EURGBP (+0.42%) Currently MAs are aligned higher as the asset recovered more than 50% of 3-day losses, MACD signal line & histogram are above 0 and RSI is retesting OB barrier, but Stochastic declines suggesting a possible correction. H1 ATR 0.00062, Daily 0.00448.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.