- USD down (USDIndex at 95.80) as Omicron worries ebbed further after reports that 3 jabs of the Pfizer vaccine are offering good protection against the variant, with global stock markets sustaining weekly gains but traded mixed, with USA30 and USA100 unchanged most of the session.

- The BoE is increasingly seen to push back a planned rate hike into next year, which is adding to pressure on the Pound.

- The JOLTS report showed a bounce in openings to another 11 mln level, but a decline in quits.

- The Bank of Canada left policy on hold, as expected.

- A business outlook indicator for Japan came in much stronger than anticipated, but Topix and JPN225 still dropped -0.6% and -0.5% respectively.

- US debt limit drama averted as Senate leadership makes a deal (expected at $2 trl increase) – The Senate could take it up perhaps today, with the House voting on Friday, allowing possible enactment just before Christmas.

- US Yields 10-year rate remains above the 1.5% mark though as confidence in the global recovery continues to strengthen, with most expecting the latest virus variant to provide only a temporary set-back for the world recovery and as ongoing Fed tightening worries continue to unwind safe haven trades since Thanksgiving.

- China PPI inflation drops back from 26-year high. – creates room for further stimulus measures.

- USOil – rose to $73.12.

- Gold: at the $1780 area as there are limited gains on elevated Treasury yields and caution in the run-up to a key US inflation data and Federal Reserve policy meeting, which capped gains of the non-yielding asset.

- FX markets – AUD and NZD were sought as local yields moved higher. Sterling stabilised, after selling off yesterday and Cable is currently at 1.3213. EURUSD corrected overnight, but is still firmly above the 1.13 mark at currently 1.1331. USDJPY at 113.50.

European Open – The March 10-year Bund future has lifted 16 ticks to 173.65, outperforming versus Treasury futures, which are little changed, although in cash markets the US 10-year rate has also corrected from yesterday’s highs. GER30 and UK100 futures are up 0.1%, after being pressured by a jump in yields yesterday, as ECB officials signalled that Omicron won’t derail plans to phase out PEPP in time next year.

Today – In the US, Jobless claims are on tap. In Switzerland SECO will release its latest set of forecasts ahead of next week’s SNB decision.

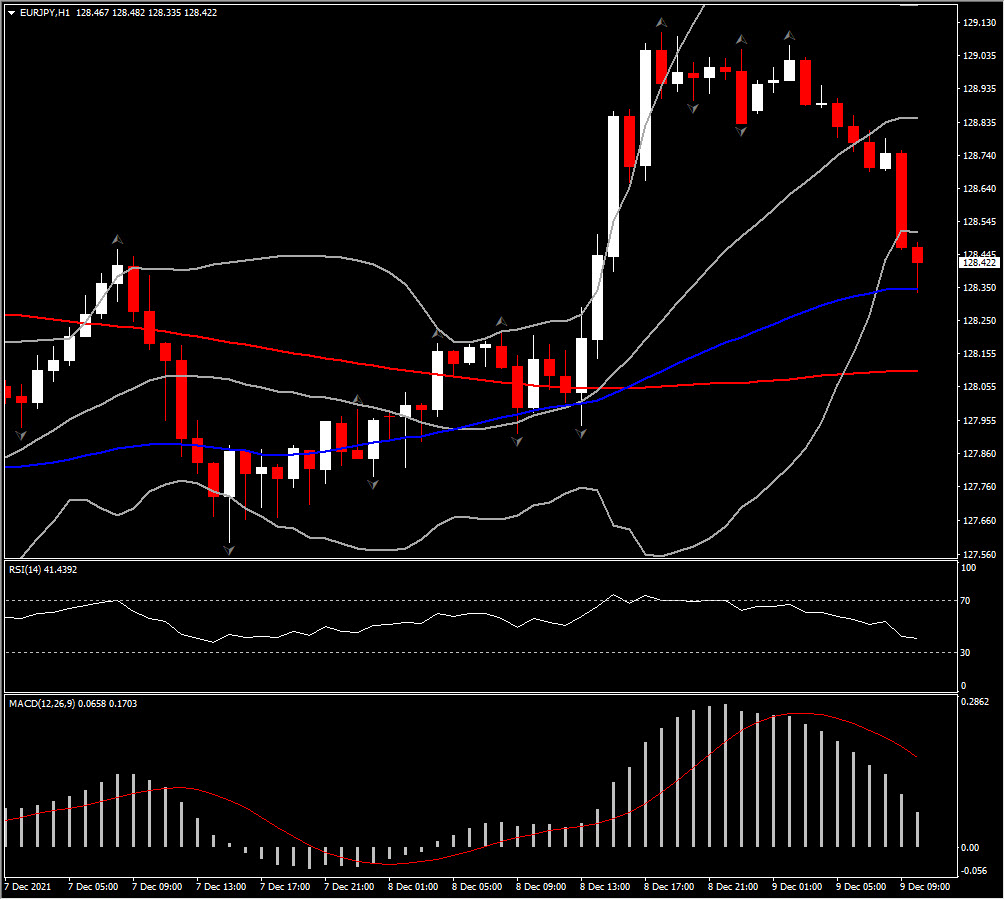

Biggest FX Mover @ (07:30 GMT) EURJPY (-0.36%) Currently MAs are aligned lower as the asset turned below PP. MACD signal line & histogram are slipping, RSI is at 41 and Stochastic declined to 12. H1 ATR 0.127, Daily 0.908.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.