The year 2021 has basically wrapped up. Though under the clouds of Omicron, inflation, and reduced central bank accommodation, the extreme fears from a few weeks ago have faded. That provided an optimistic setting for a Santa Claus rally into the Christmas weekend. Global data has generally reflected a solid pick up in Q4 growth, even if dented somewhat by the variant. Inflation remains a risk significant risk but the FOMC and other central banks are addressing it and bond markets are giving policymakers the benefit of the doubt. There is little this week to distract from cautious merry making into 2022.

Most of the key US data reports were released ahead of the holidays and they have reflected a substantial jump in Q4 growth, with GDP estimated accelerating to a 7.0% clip from teh this month’s critical reports were released in the advance of the holidays, allowing a substantial fine-tuning of market estimates on Wednesday and Thursday before a light report week. This week’s slew of data largely narrowed growth prospects around existing expectations. The GDP growth rate in Q4 is anticipated at 7%, triple the 2.3% pace in Q3 clip. However, inflation prospects were also boosted slightly. Robust growth and near 40-year highs on CPI made the FOMC’s decision to accelerate the taper a relatively easy call.

Now comes the hard part, determining the timing and the pace of liftoff and tightening. Currently the markets are set for liftoff in May or June, with a quarter point hike, and possibly on or two on the year.

The thin data slate in the abbreviated week contains few top-tier releases. The Treasury’s $169 bln in shorter dated coupon auctions will be an interesting test of investor demand given several contradictory forces. The demand for the safety of Treasuries and their higher yields, along with further supply cuts will help cap yields. But the risks of persistent inflation, the Fed’s tapering and eventual rate hikes will push rates higher. As to these auctions, the total volume was cut by $7 bln from last month as the pandemic related borrowing needs have declined substantially. The 2-year closed 2.8 bps cheaper on Thursday at 0.745%. A stop there would be the highest since the 1.188% from February 25, 2020. The 5-year was up 2.6 bps at 1.270%. The 7-year was 3 bps higher at 1.425%. It is not clear that those rates will be attractive enough to attract strong demand, especially amid thin holiday conditions.

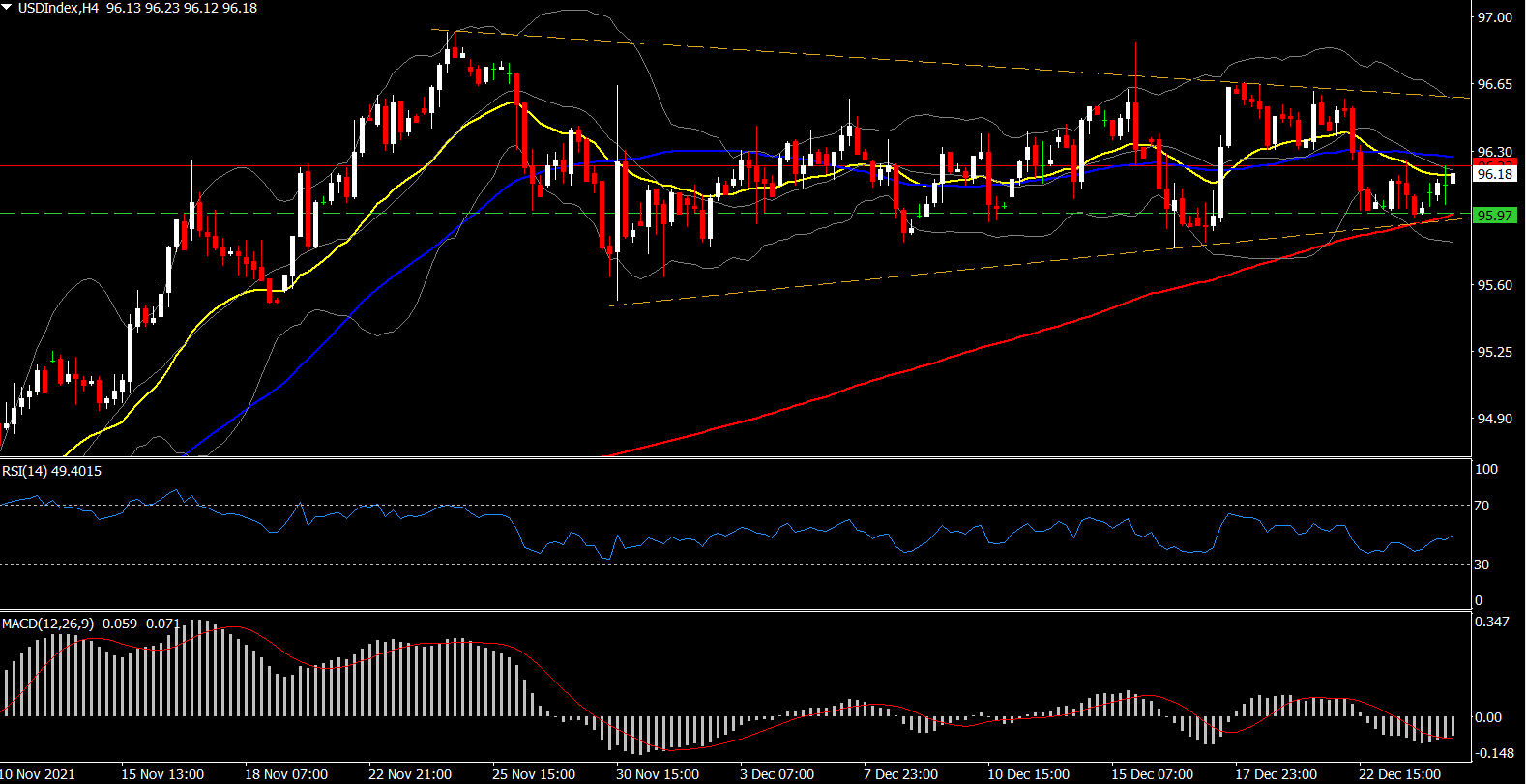

The US Dollar has remained range bound at the start of another holiday shortened week, with the USDIndex currently at 96.18. London, Canada, Australia and Hong Kong were among the markets still closed for the extended Christmas holiday weekend. Incoming data last Thursday was mixed, which saw jobless claims sit near trend lows, while personal income and consumption were in-line with forecasts. Durable orders beat expectations, though a large new home sales downward revision was not expected. The US was closed on Friday in observance of Christmas.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our written permission.