Inflation worries and the Fed’s hawkishness prompted buying in shares like banks that usually perform well in a high interest rate environment, while high-growth stocks were routed. Share markets have made cautious gains so far today as the US jobs report gave the green light to investors to count down to another US inflation reading that could well set the seal on an early rate hike from the Federal Reserve, lifting bond yields yet further. Going from uber-accommodation in November to liftoff as soon as March, multiple rate hikes in 2022, and subsequent balance sheet shrinkage in a matter of two months spiked Treasury yields. Volatility in stocks jumped as investors repriced for the new conditions.

The explosion in coronavirus cases globally also threatens to crimp consumer spending and growth just as the Fed is considering turning off the liquidity spigots, tough timing for markets addicted to endless cheap money. – Reuters

- USD (USDIndex 96.20) slips but holds gains supported by higher yields – 95.88 currently.

- US Yields 10-yr is coming off of its worst week in years thanks to the FOMC’s pivot to the hawkish side, and as government and corporate supply picks up. Key technical levels were also broken to exacerbate the selloff. It will be hard pressed to rally unless there are signs Omicron will take more of a toll on growth than currently anticipated, suggesting the FOMC will not need to boost rates as aggressively as feared.

- Equities – US equities closed in the red. USA100 had struggled at the end of last week, but frayed nerves have started to calm – for now – USA100 at 15664. USA500 at 50DMA below 4700. Tech stocks in Hong Kong rebounded, which saw the Hang Seng lifting 0.8%. Stock markets across Asia traded mixed, in quiet trade, with Japan on holiday today.

- USOil – held firm,sustaining last week’s gains at 78.70.

- Gold – at $1794.

- FX markets – EURUSD corrected to 1.1341 amid broader pressure on the Euro, USDJPY rebounded to 115.75, Cable steady at 2-month high at 1.3590.

European Open – The March 10-year Bund future is down -13 ticks and US futures are posting similar losses, as yields continue to rise against the background of rising inflation and easing virus concerns. GER40 and UK100 futures are up 0.2%, as stock market sentiment improved at the start of the week.

Today – Central bank outlooks and virus developments will remain the focus of attention this week, with investors likely to keep a close eye on upcoming Fedspeak. For today though the calendar is pretty light on both sides of the Atlantic with only Eurozone unemployment and US Wholesale inventories scheduled.

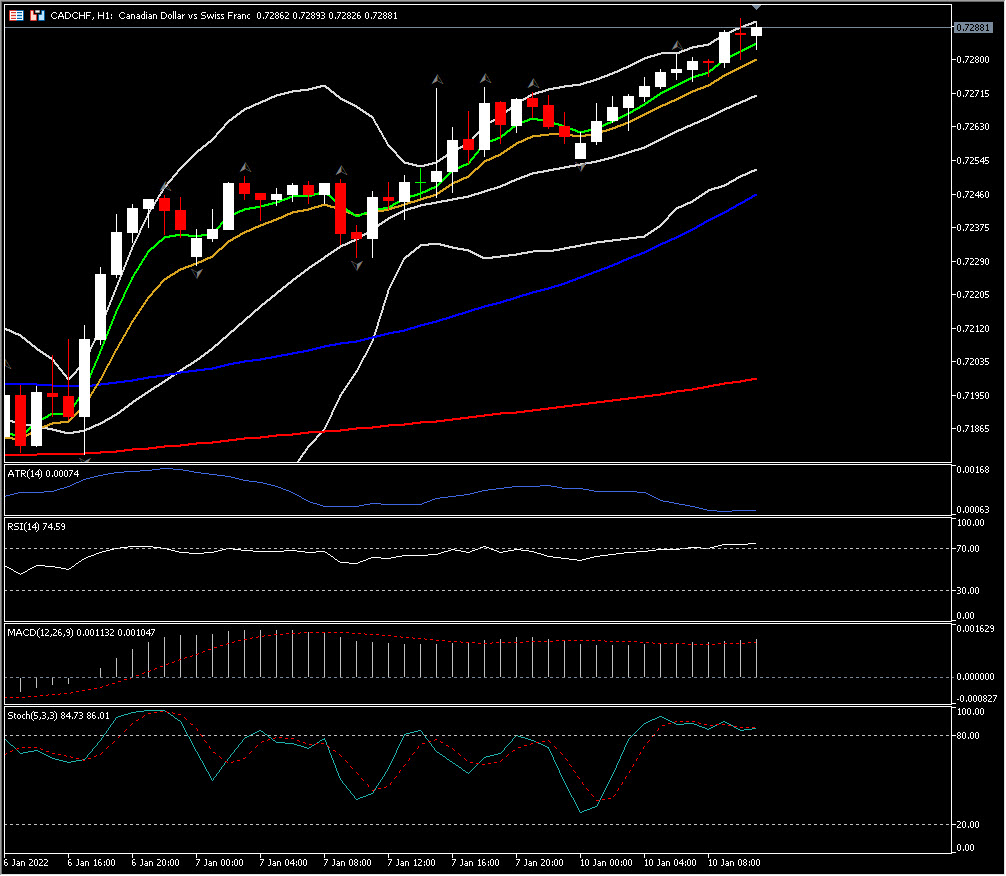

Biggest FX Mover @ (09:30 GMT) CADCHF (+0.33%) Rallied to 0.7289 extending to December’s highs. MAs aligned higher, MACD signal line & histogram well above 0 line. RSI 75, OB but still rising.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our written permission.