Some of the more intense selling pressure seen so far in 2022 took a break this morning. Indeed, though Wall Street opened with sharp declines, the major indexes rebounded through the afternoon and the USA100 managed a modest 0.05% gain. The USA500 was -0.14% lower at the end of the day, while the USA30 lost -0.45%. Bonds traded mixed, as Treasury yields corrected slightly after the move higher in the wake of stronger than expected data yesterday.

Fed remarks: Little insight with no mention of the policy plans. Powell reiterated the economy is expanding at its fastest pace in many years and the labor market is strong, while facing “persistent supply and demand imbalances” with the resulting jump in inflation taking its toll. That outlook was the underpinning for the shift toward tightening policy sooner than later. He also stressed the Fed will use its tools to support the economy and the labor market.

- USD (USDIndex 95.82) slips from yesterday’s 96.22 high from temporary yields support.

- Goldman Sachs expects the Federal Reserve to raise rates four times this year, one more than previously forecast.

- US Yields 10-yr rose to an almost 2-year high above 1.8% overnight, but provided only muted support for the Greenback.- 1.759% currently.

- Today, treasuries cheapened further with the front end underperforming as more hawkish Fed bets were made on the heels of Goldman Sachs’ outlook. The advent of Chair Powell’s Senate Banking Committee hearing today has also added to the weakness amid uncertainties whether he would push back against the markets’ views on the FOMC and concomitant selloff. The upcoming $52 bln 3-year auction also weighed.

- Equities – in the red, with the USA100 leading the way USA100 at 15638. Topix and JPN225 lost -0.4% and -0.9%, the ASX corrected -0.8%, and mainland China bourses are also in the red, while the Hang Seng essentially moved sideways. GER30 and UK100 futures, however, are up 0.3%.

- USOil – up at 78.40.

- Gold – north for a 3rd day – at $1808.

- FX markets – EURUSD at 1.1334, USDJPY at 115.27, Cable steady at 1.3595.

European Open: The March 10-year Bund future is fractionally higher, underperforming versus Treasury futures. In cash markets US bonds have also found a footing after being pressured by stronger than expected data yesterday. The ECB is struggling to assure consumers that they are not blind to the uptick in inflation, although the central bank risks falling behind the curve.

Today – Fed Chair Powell’s testimony headlines today. Along with Powell, there is also Fedspeak from Mester and George (Bullard’s discussion on policy and the economy was postponed). The only data on tap is the NFIB small business optimism index. Wednesday brings the main event, CPI.

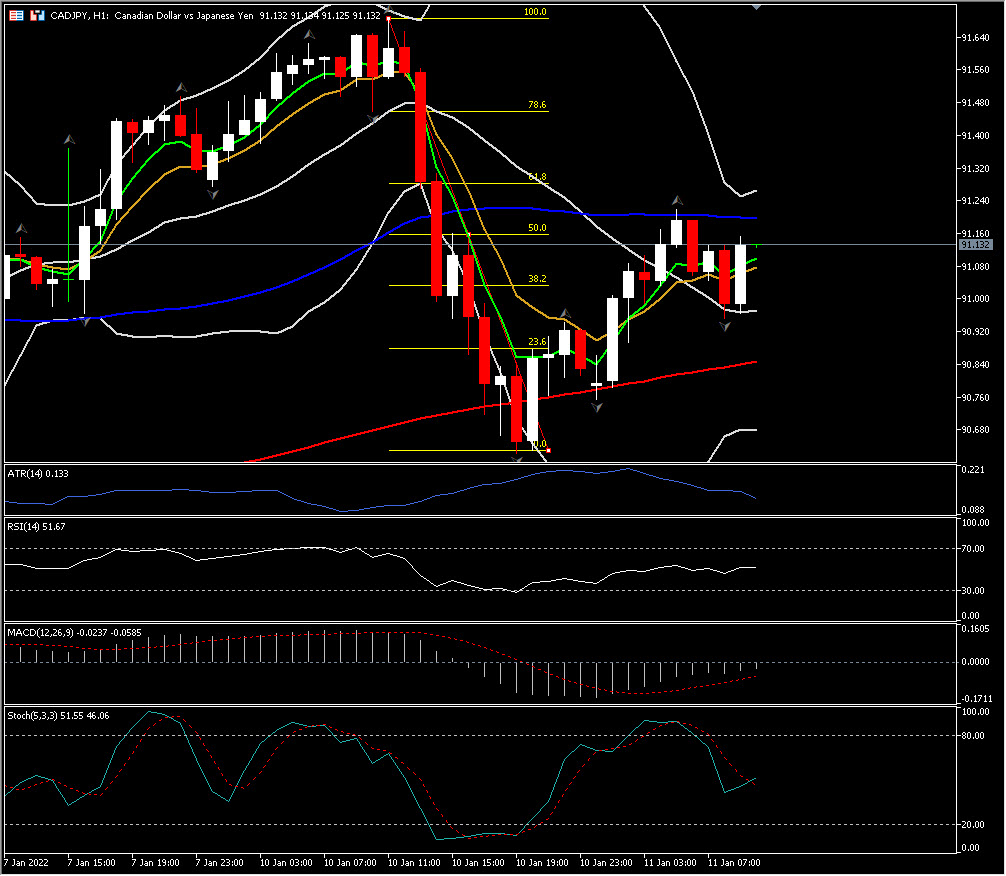

Biggest FX Mover @ (09:30 GMT) CADJPY (+0.33%) Rebounded to 91.13 reversing nearly half of this week’s losses. MAs currently flat, MACD signal line & histogram below 0 line. RSI 51, Stochastics started rising.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our written permission.