A flight out of equities and into the safety of bonds was the opening theme yesterday – Could we see this repeated?

US futures are under pressure once again, alongside a broad sell off across Asian equity markets. Tensions over the Ukraine, virus developments in China and the prospect of reduced central bank support all continued to weigh on sentiment overnight. The rise in Omicron cases ahead of the Lunar New Year holidays and of course the Olympic Games is adding to nervousness over slowing growth.

- Australia’s inflation rate came in higher than expected, which added to growing conviction that the RBA will end its quantitative easing program at the February 1 meeting.

- Singapore surprised with a move to tighten policy outside of a scheduled review

- USD (USDIndex 95.90) saw a pullback after breaching 96.11.

- Treasury rates dove lower with a strongly bid 2-year sale extending the slide. The just auctioned 2-year rate dropped 7 bps to hit 0.970%.

- Equities – Hang Seng and CEI 200 expected to drop more than -1.8% today. The Nikkei closed with a loss of -1.7%, the ASX plunged -2.5% after the hot inflation report. Yesterday, USA100 crashed -4.9%, with the broader indexes over -3% lower before hitting bottom and paring losses. But a late buy the dip rally saw the USA100 rally 0.63%, with the USA500 and USA30 up 0.29%.

- USOil – back to $82.00 territory, – recovering some of yesterday’s losses, as growing tension in Eastern Europe and the Middle East fuelled concerns over possible supply disruptions. Lower US oil inventories are also providing support.

- Gold – held on to gains at $1841 as investors sought safety.

- Bitcoin steadied to $35,000 handle.

- FX markets – The Yen was supported as risk aversion picked up and USDJPY dropped to 113.66. EURUSD at 1.1306 & Cable below 1.3500.

European Open – European stock futures are signalling a bounce back from yesterday’s sell off, with the GER40 and UK100 currently posting gains of 1.1% and 0.8% respectively. EGB yields are set to rise today, as stock markets bounce back from yesterday’s sell off. The German 10-year Bund yield is up 1.4 bp at -0.097% in early trade, the French 10-year up 1.3 bp, both underperforming versus Treasuries, which have moved higher overnight, as Asian stock markets sold off.

Today – The FOMC meeting starts today, with an announcement due tomorrow, ahead of the ECB and BoE meetings in February. Geopolitical risks will remain in focus today, while the data calendar highlights are the German Ifo readings and the UK CBI manufacturing survey.

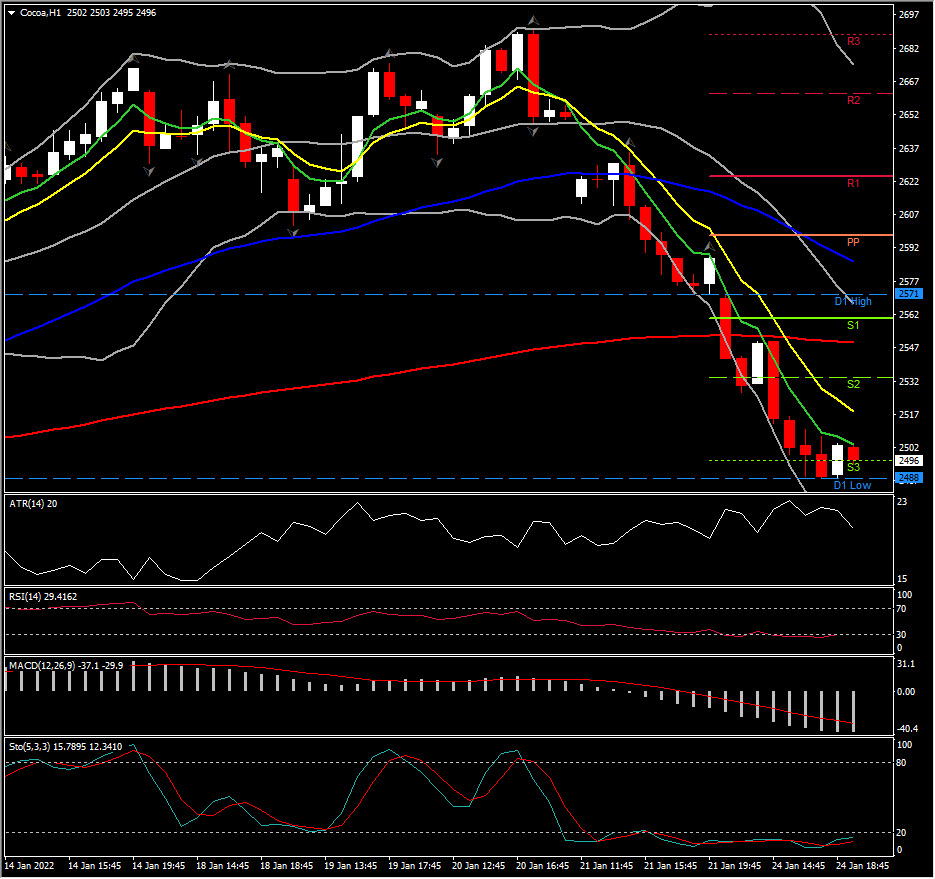

Biggest FX Mover @ (07:30 GMT) Cocoa (-3.22%) Huge dive to 2488 from 2684 highs seen last week, breaking all daily SMAs (20-, 50-, 200-day). Fast MAs aligned lower intraday with all momentum indicators pointing further lower.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our written permission.