Treasury yields were mixed inside a narrow range as the market consolidated, coming to grips with the hawkish stance from the FOMC and other core central banks, while they found some support from EGBs. ECB’s Lagarde stressed rate hikes will not begin until after asset purchases are ended. Trading was also slowed as the CPI report looms Thursday. The front end outperformed slightly as shorts covered, paring some of the selling from Friday. Wall Street was mixed and rather directionless, despite earnings. After finding a small bid into the afternoon, the indexes slumped into the close. Oil drops on progress in US-Iran talks.

- USD (USDIndex 95.61) steady.

- US Yields 2-year rate slid 2 bps to 1.288% after having surged to test 1.32% on Friday. However, the 10-year was fractionally underwater and rose to 1.945%, a new high since late 2019.

- Equities – USA500 ( -0.37%) 4487, USA100 (-0.58% )recovered to 14605. (Meta shares fell more than 5%, Peloton jumped over 20% on media reports of interest from potential buyers including Amazon, Tyson Foods firmed on upbeat quarterly results, Nvidia rose 1.7% ,Alibaba fell about 6% after it registered an additional 1 billion American depositary shares.) JPN225 and ASX are up 1.1% and 0.1%. GER40 and UK100 futures are up 0.1% and 0.2%.

- USOil – flattened around $90.00 amid concerns over tight supply.

- Gold – jumped to $1823 above 20-day SMA. Gold rose 1.2% last week and posted its strongest weekly gain since November. Yields have been ebbing from overnight highs, while the USD is a little weaker, to provide some support to gold. Geopolitical risks are also underpinning.

- Bitcoin extended to $45,485. – Bitcoin and the Australian Dollar had posted gains as equity markets rallied in Europe.

- FX markets – EURUSD up to 1.1405, USDJPY up to 115.48 & Cable to 1.3520

Overnight – ASX outperforming, helped by a jump in iron ore prices, which boosted miners. Talk of more companies being added to the list of companies that may need extra permits to buy from US entities weighed on the Hang Seng in particular and the index is currently down -0.99%. WTO lets China impose $645 million tariffs on US.

European Open – The March 10-year Bund future is down 8 ticks, slightly outperforming versus Treasury futures, as yields continue to rise in cash markets. Lagarde failed to push back against speculation of an early end to net asset purchases and swift start to rate hikes yesterday and Eurozone peripherals in particular are likely to continue to struggle.

Today – Today’s calendar is thin and should have no impact on expectations. The December trade report is due. The earnings calendar features reports from Pfizer, BP, S&P, Fiserv, Thomson Reuters, Coinbase, Centene, KKR, Chipotle, DuPont, Sysco, Yum! Brands, Transdigm, Cenovus Energy, Warner Music, FleetCor, Incyte, and FMC.

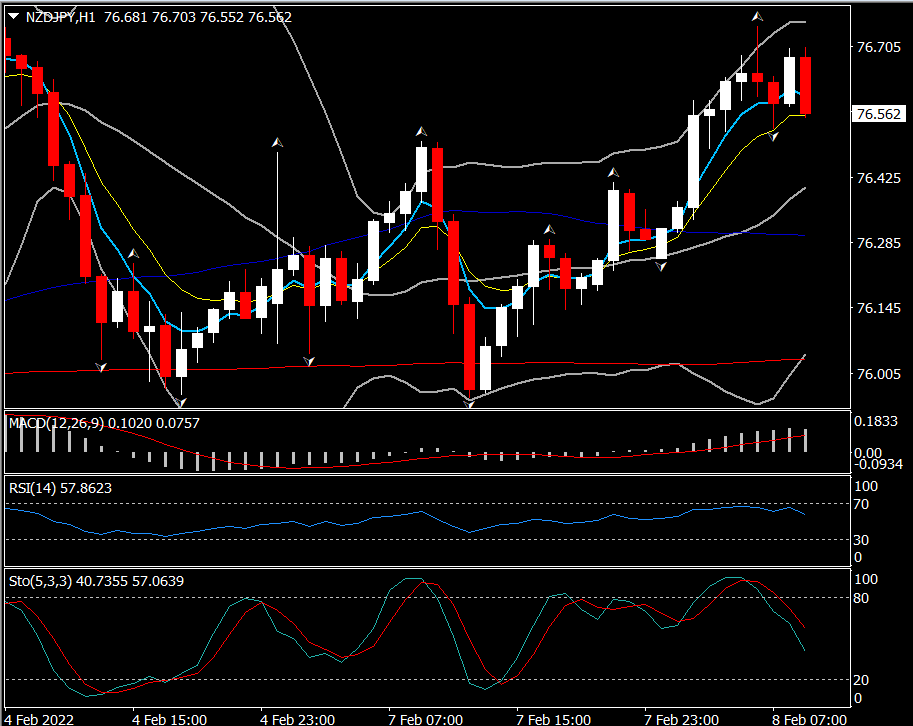

Biggest FX Mover @ (07:30 GMT) NDZJPY (+0.46%) Rallied to 76.75 retesting the 20 DMA for a 4th day. MAs aligned however started turning lower, MACD signal line & histogram levelling off but well over 0 line, RSI at 57 in a pullback.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.