In its next meeting the ECB was to confirm an end to net asset purchases and pave the way for a rate hike in the last quarter of the year. Then Russia invaded Ukraine, commodity prices spiked, and stagflation fears are now making the rounds, leaving the doves at the central bank to warn against ‘tightening measures.’

The ECB was always likely to be far behind the Fed, and now its close geographical proximity to Ukraine and Europe’s reliance on Russian oil and gas have fuelled stagflation concerns and seen the German 10-year rate drop back into negative territory over the past week.

The fact that the ECB lags other central banks and continues to pump money into the system is coming back to haunt the central bank as there is nowhere much to go at the moment. Either the ECB finally moves towards policy normalisation and reduces stimulus, which could hurt those hoping for even more support, or it continues to fuel the fire of inflation that is already going through the roof. With EU heads of state set to announce another massive joint financing package to cover energy and defence policies the ECB may have more options on net asset purchases going forward, but if it doesn’t appear to be doing something to stem the spike in the cost of living it risks losing its remaining credibility on its commitment to maintaining price stability.

The ECB has already moved much further away from the Bundesbank tradition than ever seemed possible at the start of the Eurozone and German consumers in particular will be in for a shock as the combination of extremely high inflation and negative interest rates erodes not just disposable income, but also savings. A way out may be another modified asset purchase program alongside a revision of the commitment to phase out purchases before hiking rates. There are no easy options in sight and for tomorrow that could well mean doing nothing, keeping all options open and highlighting uncertainty.

Inflation meanwhile is not judged to be Lagarde’s main priority, which only highlights that the central bank needs to finally act if it doesn’t want to totally erode confidence in its commitment to price stability. That business confidence is plunging thanks to the Ukraine war is pretty much a given, but at the same time, the spike in inflation is also hitting consumer confidence and if the ECB doesn’t want to totally undermine its inflation busting credentials it will have to do something to rein in stimulus at least.

Maybe another EU debt issuance package will give Lagarde some options – as long as the ECB drops the commitment to phase out asset purchases before hiking rates – but while we expect the ECB to sound more vague on future policies than it would have otherwise, on balance we still expect the central bank to confirm that net asset purchases will end in Q3 – in the central scenario.

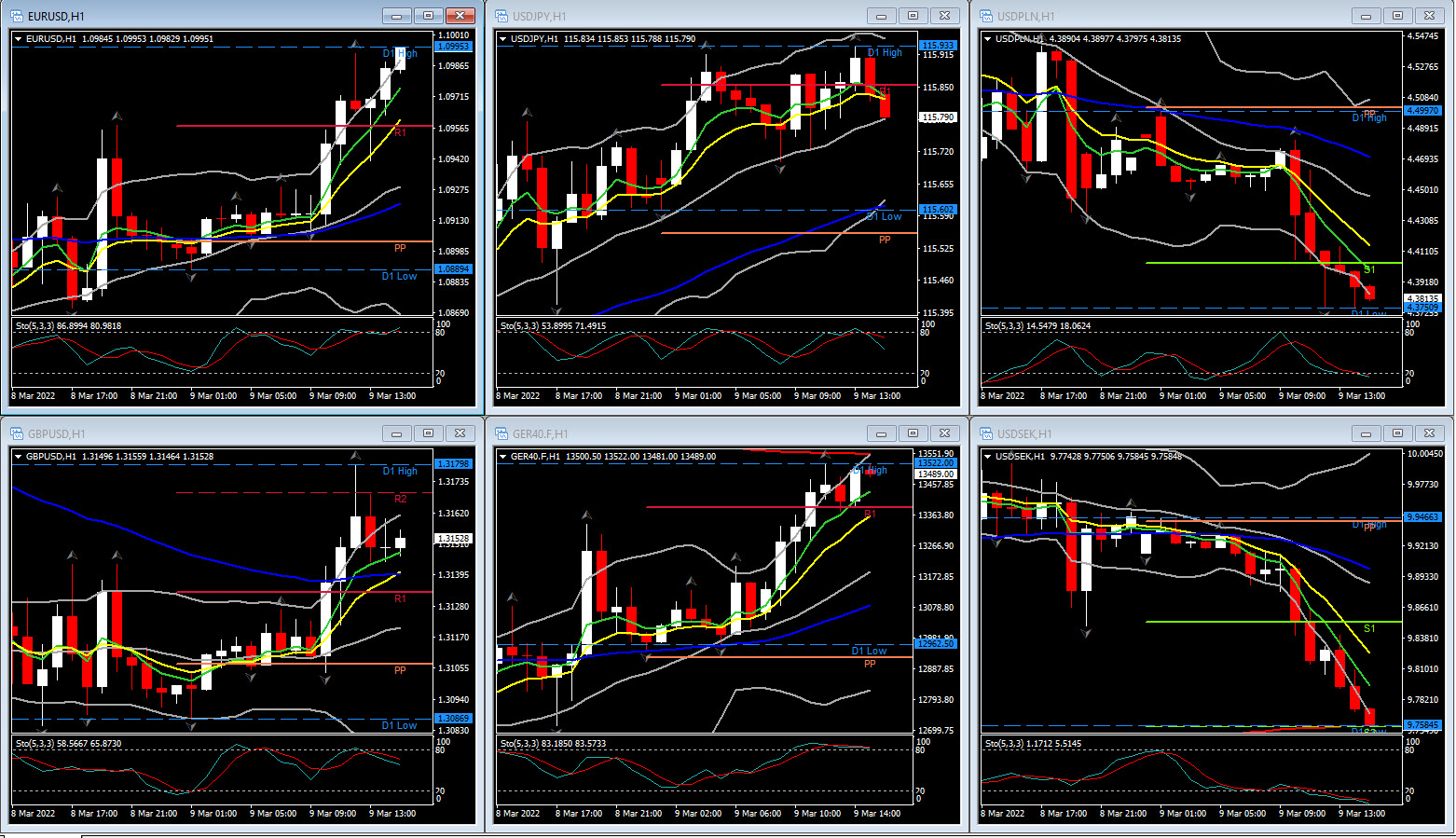

Reports of plans for jointly funded defence and energy projects at the EU level seem to have put a floor under EURUSD at around the 1.09 mark, at least for now, and boosted European bourses today as risk appetite stabilised and markets bank on ongoing support from the ECB ahead of tomorrow’s council meeting, though that is expected to be just a short term rally. If Lagarde comes over all dovish in the light of stagflation concerns, or Russia threatens to widen the conflict, setbacks are likely.

For now though it seems there is some hope that the war will remain localised, which has also helped the SEK to continue to bounce back from recent lows. Cable is trading at 1.3168 this morning, while Sterling corrected versus the EUR. The Yen is also down as safe haven flows eased, and USDJPY lifted to 115.81, even as the US Dollar declined against most other currencies.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.