FX News Today

European Fixed Income Outlook: The December 10-year Bund future opened at 159.82, down -4 ticks from yesterday’s close of 159.70. 10-year Bund yields are down -1.2 bp at 0.420%, while 10-year Treasury yields are down -3.7 bp at 3.19%, 10-year JGBs down -0.4 bp at 0.116%. Stocks struggled and moved off earlier highs during the Asian session as investors digested the US mid-term election result. US futures are also down from highs, but still managing to hang on to early gains and U.K. futures are also higher. Released at the start of the session, German industrial production rose a modest 0.2% m/m, in line with our forecast and a tad higher than Bloomberg consensus, although after the very strong orders number yesterday, a positive production report is not a surprise. The calendar also has Eurozone retail sales, UK house prices and a German 10-year Bund auction, but politics from the U.S. election result to Brexit, Italy’s budget spat and in Germany the battle for Merkel’s succession are all overshadowing the data calendar as the FOMC announcement comes into view.

Asian Market Wrap: 10-year Treasury yields are down -3.5bp at 3.189%, 10-year JGB yields fell back -0.4 bp to 0.115%. Asian equities and US stock futures moved down from early highs as traders mulled the implication from the US midterm election which showed a split in Congress as the Democrats are on course to win the House of Representative majority and Republicans clinching control of the Senate. With the elections out of the way the focus will also return to the U.S-China trade conflict. The ASX managed to close with a 0.37% gain, but Topix and Nikkei erased earlier gains and are down -0.42% and -0.28% respectively, the Hang Seng is down -0.52% and Shanghai and Shenzhen Comp lost -0.35% and -0.25% so far. U.S. futures are still higher, but also down from earlier highs. The WTI future meanwhile is down from highs over USD 62 per barrel and trading at USD 61.84.

Charts of the Day

Main Macro Events Today

- Canadian Ivey PMI – Expectations – The Ivey PMI for October is anticipated to improve to 53.0 from 50.4 in September.

- RBNZ Monetary Policy – Expectations –The RBNZ will also release the quarterly Monetary Policy Statement.No change is expected to the current 1.75% setting for the official cash rate (OCR).

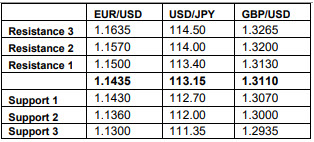

Support and Resistance Levels

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.