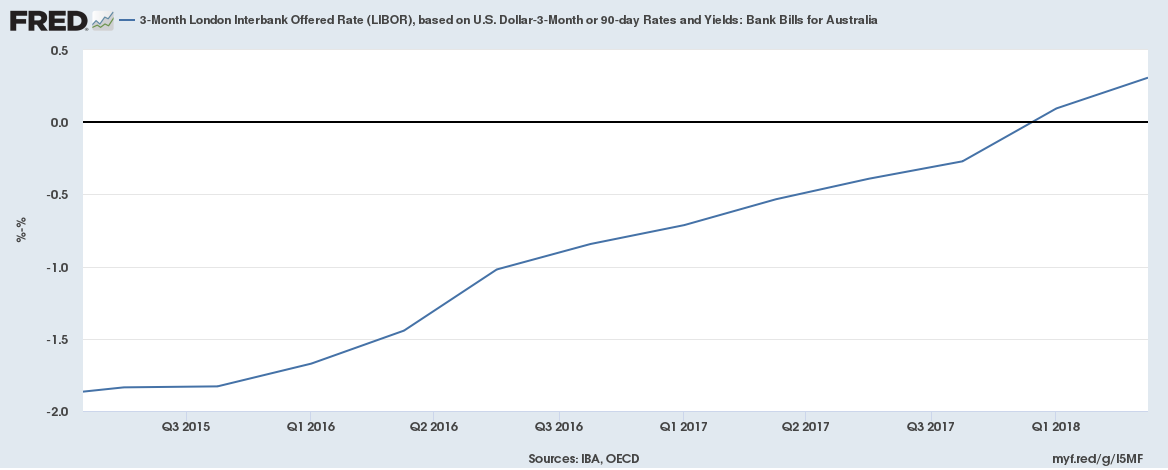

Following a 14 basis points (bp) increase in mortgage rates by Australia’s third largest lender last week, both for new as well as existing loans, two more major lenders, ANZ and Commonwealth Bank, raised their mortgage rates today, by 15 and 16 bps respectively. The ANZ group executive commented that “The reality is it is more expensive for us to fund our home loans on wholesale markets and we also needed to balance the needs of all stakeholders.” While RBA officials commented that this is expected because Australian banks borrow a lot of money offshore, particularly in the US, where rates are rising, this appears not to be a perfectly satisfactory answer. Granted, the spread between the Australian 3-month Libor rate and the respective US interest rates (Overnight Libor, Federal Funds Rate, and 3-month Libor – for ease we just report the spread using the 3-month US Libor rate) has only become positive since early 2018. However, the question which should come to our head would be why should Australian banks need to borrow from abroad?

When elaborating on the economic fundamentals of inflation, we have noted that in an open economy, capital flows from the rest of the world have a strong effect on the economy. The reason that Australian banks need to borrow from abroad is that credit has been growing fast in the country, reaching 177% of GDP in 2017, more than doubling over the course of the last twenty years, with Australia having the largest debt-to-GDP ratio among the main developed economies. This has forced Australian lenders to look out of their country for funds, relying more and more to the US as total credit increased. As a result of the protracted increase in bank lending, house prices have also been on the rise, doubling since 2003, albeit in a downwards trend in the past few months.

At the moment, 35% of total loans fall in the interest-only (IO) category, meaning that principal is not repaid, usually for the first 5 years of the loan’s life. As in the pre-crisis period in the US, most of these loans are usually re-financed at the end of the 5-year period. According to some estimates, a total AUD120 bln of interest only (IO) loans are due to expire every year between 2018 and 2021. The drop in house prices, if continued, could increase loan-to-value ratios, which stand at more than 80% for about 20% of consumers. This would increase the already escalated worries about mortgages, as those who borrowed near their maximum would find it difficult to refinance their loans. The overall situation bears much resemblance to the US in late 2006-early 2007.

Unfortunately, that is not all there is: the combination of declining house prices and high total mortgage credit suggests that homeowners would be unable to refinance their debt and would be forced to revert to traditional Principal & Interest (P&I) loans. In a speech in April, RBA Assistant Governor Christopher Kent commented that a shift from interest-only loans, to P&I loans would cost an extra AUD7,000 per year for households. Given the current estimates, this increase would amount to more than 10% of median income, a 30-40% increase compared to interest-only payments. The estimate may appear to be quite conservative in light of the expected interest rate hikes in the US which would likely raise the Australian banks’ cost of funding even further. Add to that the potential for interest rate hikes from the RBA in 2019, and interest payments could double as Bloomberg also notes.

So what are the chances of Australia coming out of this unscathed? The country’s largest lender, ANZ has already began focusing on customers with lower loan-to-value ratios, offering lower rates most likely in an effort to lower its exposure, while other lenders appear to have tightened their standards. Nonetheless, if housing prices continue their decline, combined with the expected increase in funding costs and the highest level of indebtedness on record, tighter standards could actually boomerang and Australia may looking ahead at the storm it managed to avoid in 2008-2009. As house prices have declined for the third quarter in a row (with unofficial data showing that the decline will continue) it is now a waiting game.

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/09/11 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.