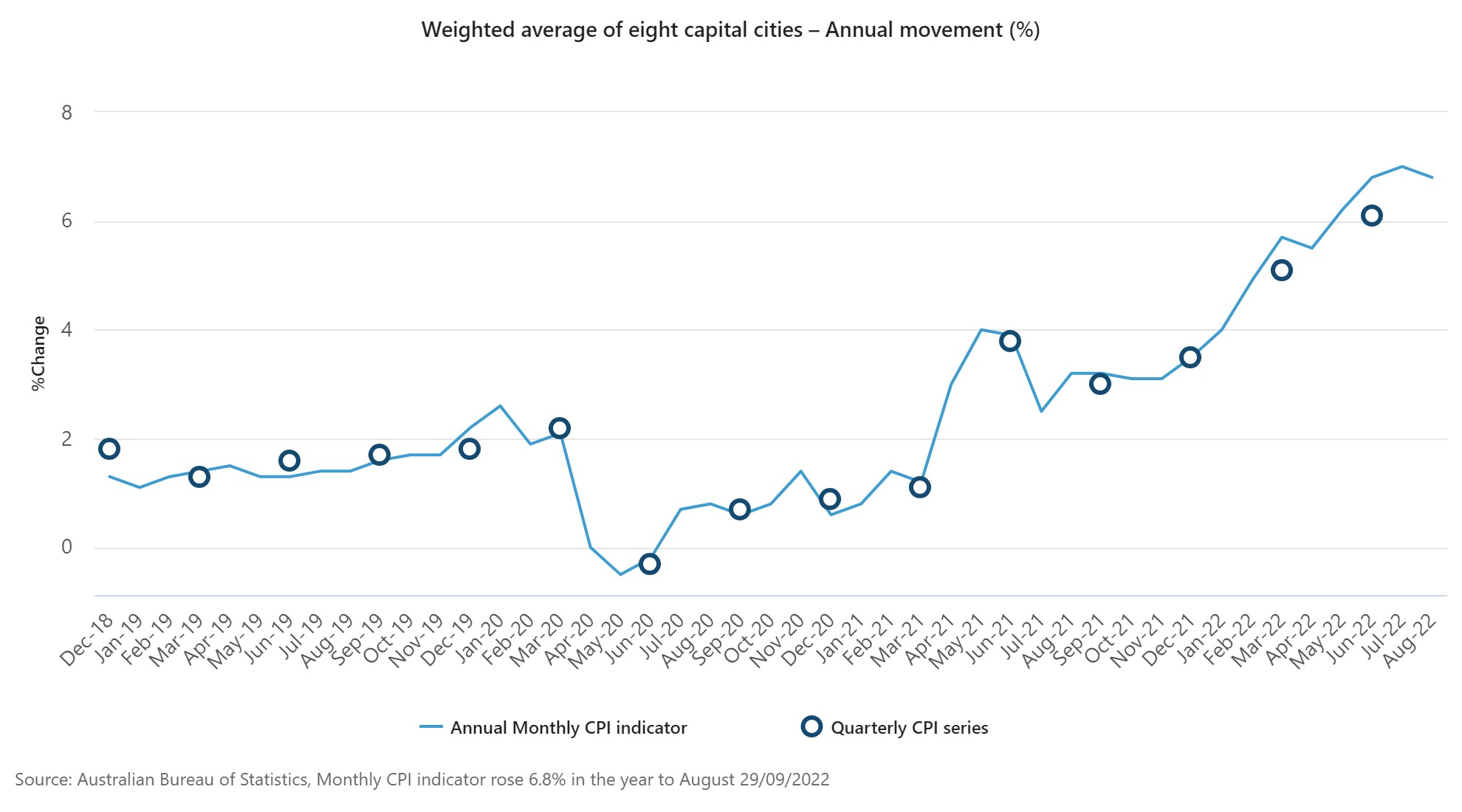

Australia’s monthly consumer price measure on Thursday (29/09) showed the annual inflation rate eased slightly in August from July thanks to a sharp drop in petrol prices, which may hint cost-of-living pressures may be nearing their peak.

In its first monthly release, Australia’s CPI rose 6.8% y/y in June, accelerated to 7.0% y/y in July and slowed to 6.8% y/y in August. The monthly CPI excluding fruit, vegetables and fuel rose 5.5% y/y in June, increased to 6.1% y/y in July, then 6.2% y/y in August. However, the monthly readings can differ considerably from the quarter CPI figures. The monthly CPI only has about two-thirds of the price observations of the quarterly series and is more volatile, thus somewhat limiting its usefulness. After all, it has not been seasonally adjusted and does not include the core inflation measure favoured by the RBA.

This data comes ahead of next week’s RBA Policy Board meeting, where markets are expecting a 50bp rate hike to a 9-year high of 2.85%.

Meanwhile, ANZ New Zealand Business Confidence rose from -47.8 to -36.7 in September. Own Activity Outlook rose from -4.0 to -1.8. Investment intentions rose from -2.0 to 1.8. Work intentions rose from 3.4 to 5.9. Price intentions rose from 68.0 to 70.1. Cost expectations fell from 90.9 to 89.8. Inflation expectations decreased from 6.13% to 5.98%.

ANZ said that demand has not rolled over as feared as the Central Bank has raised interest rates. But to the extent that the RBNZ can keep going until they see the drop in demand they need to tame inflation, it will likely be a temporary reprieve, if not a double-edged sword for companies that have considerable debt.

Technical Review

Meanwhile in the FX market, AUDNZD has rallied since December 2021 and reached an 8-year high below the 1.1500 range. RSI (70.62) entered the overbought area for the first time since July 2008. However, poor market sentiment and fear over China’s economic outlook will be a test for AUDNZD. The PBOC has recently intervened several times in the market and is likely to do so again to defend the Yuan amid fears of an economic slowdown, caused by the lockdown.

AUDNZD,H2 – Intraday bias looks neutral for now, and a move to the upside could test the recent peak at 1.1488 or the multi-year peak of 1.1528 (2015). However, 1.1500 will make the bulls rethink their positions. In today’s Asian session trading, it was seen that the bears attempted to surpass the minor support of 1.1369, but this attempt has not been maximised.

Moving to the downside, it is likely to test the 1.1315 support before moving further to break the ascending trendline and resistance which is the support at 1.1255. The oscillation is now on the downside after the divergence created by the pair’s long liquidation attempt. Broadly speaking, it is likely that the pair will enter a consolidation phase before deciding on the next trend.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.