Dollar Index starts the new week rebounding from a bearish onslaught on the back of a softer CPI report.

Dollar

The Dollar begins the new week rebounding from last week’s decline, where it saw a 4% drop in value against a basket of major currencies. Factors driving this renewed enthusiasm in the safe-haven currency can mostly be attributed to the benefits of a risk-off sentiment in the beginning of the week. What investors will be focused on going forward is the ramifications of a softer October CPI report, which lends credence to the actions that have been taken by the FED on interest rate hikes. While most traders are seeing this as a sign of a potential pivot from the FED in the December meeting, Federal Reserve Governor Christopher Waller poured cold water on that notion, stating that one data point would not suffice in changing the pace of rates, and it would take a few more reports that affirm that inflation is indeed falling.

Technical Analysis (D1)

In terms of market structure, price has come to a significant juncture by invalidating the uptrend drawn from Feb 2022. However, this on its own doesn’t suffice to affirm that a downtrend is about to ensue, because a confluence of factors remains unchecked. The next line in the sand will be the 104.12 area where the previous higher-low was formed. If bulls can defend this area, the narrative could still remain bullish, however the opposite applies if the area is invalidated by sellers.

Euro

The Euro kicks off the week fighting to hold onto the gains it made last week versus the US Dollar. Factors influencing this rally were mainly attributed to the risk rally that ensued on the back of a reduced inflation report from the US last week, which influenced the market to scale back bets on the prospect of an additional 75 basis point rate hike in December from the FED. However, the Euro began the morning session in severely overbought territory amid the FED speak pointing towards an “over-optimism” in the market concerning their trajectory on future rate hikes, pointing towards the 7.7% inflation rate still being unacceptably high, and this has made it somewhat difficult for the Euro to continue its rally against the Dollar heading into the new week.

Technical Analysis (D1)

In terms of market structure, price remains in a downtrend, printing out lower-lows and lower-highs. Current price action seems to be printing out a larger potential bearish continuation pattern (rising channel), which would only be confirmed by an impulsive break of structure below the lower trendline. Confirmation of the above will give sellers the impetus needed to test the low of the range around the 0.95 area. Conversely, a break above the 1.01 area might give bulls renewed buying interest.

Pound

Sterling begins the week fighting off a resurgent Dollar driven by fresh risk-off sentiment. Factors contributing to this renewed pressure on the Pound are mainly linked to a weakened forecast for the British economy, cited by the National Institute of Economic and Social Research (NIESR) as it reported that there is an increasing risk of a deep economic downturn heading into 2023. This, combined with the FED speak over the weekend, has capped the momentum that the British currency had last week and it now sits at a juncture where the short-term trend will be driven by Tuesday’s employment data and Wednesday’s CPI report as well as Chancellor Hunt’s statement on Thursday as he lays out his fiscal plans.

Technical Analysis (D1)

In terms of market structure, price continues to be in a downtrend, printing lower-lows and lower-highs. Current price action is printing out a potential larger bearish continuation pattern (ascending channel). The pattern will only be confirmed by an impulsive break of the lower trendline, which will give bears the impetus to test the lower end of the range located around the 1.04 area. Conversely, a violation of the upper trendline as well as the larger downtrend could potentially give bulls control of price.

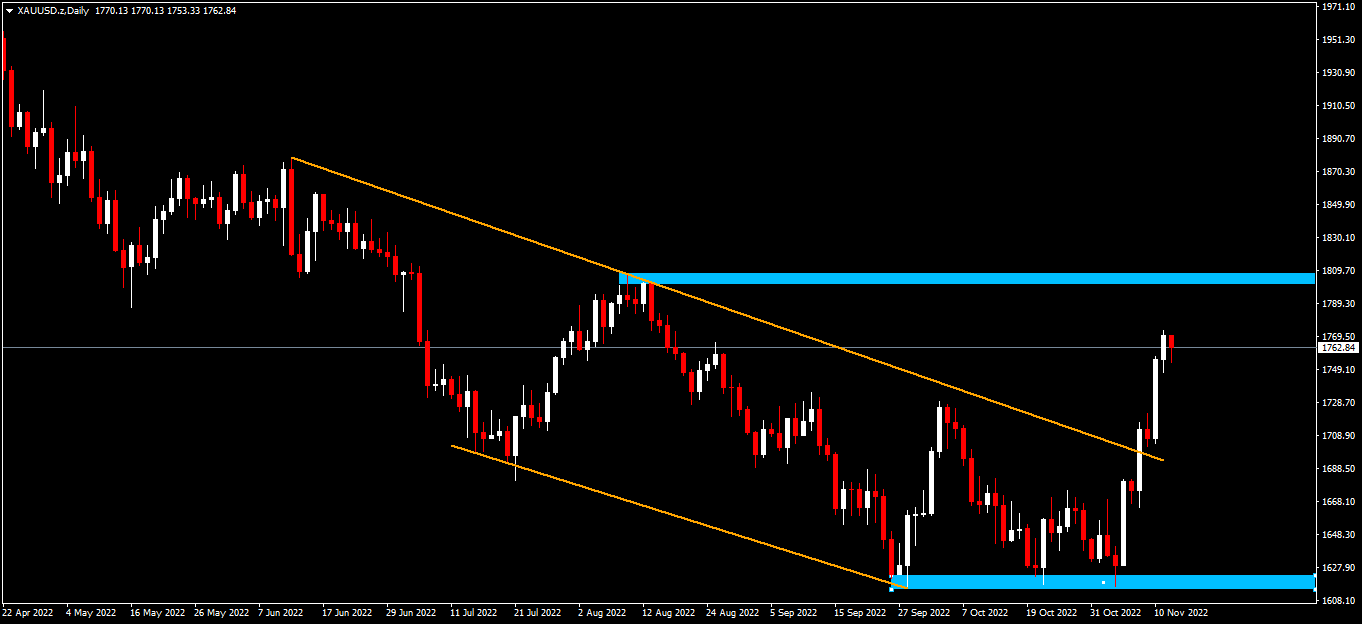

Gold

Gold heads into the new week with momentum beginning to fade at highs last revisited three months ago. This momentum was driven by last week’s softer inflation print, which prompted the Dollar to weaken amid speculation of a potential pivot driven by the report. However, in the early part of the European session these gains came under pressure, and this can be attributed to the comments made by US Federal Reserve Governor Christopher Waller, as well as an undertone of anxiety as the Group of 20 Nations (G20) meet in Bali where geopolitical divisions are taking centre stage.

Technical Analysis (D1)

In terms of market structure, Gold has just broken out of the outer trendline on the downtrend, which signifies an important inflection point in the bearish narrative. However, this on its own will not suffice to signal the end of the downward momentum, as the final line in the sand for sellers to defend is the $1 809 area. If breached, this could give bulls the impetus to drive the narrative further and if it holds, new sellers might be interested in testing the bulls.

Click here to access our Economic Calendar

Ofentse Waisi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.