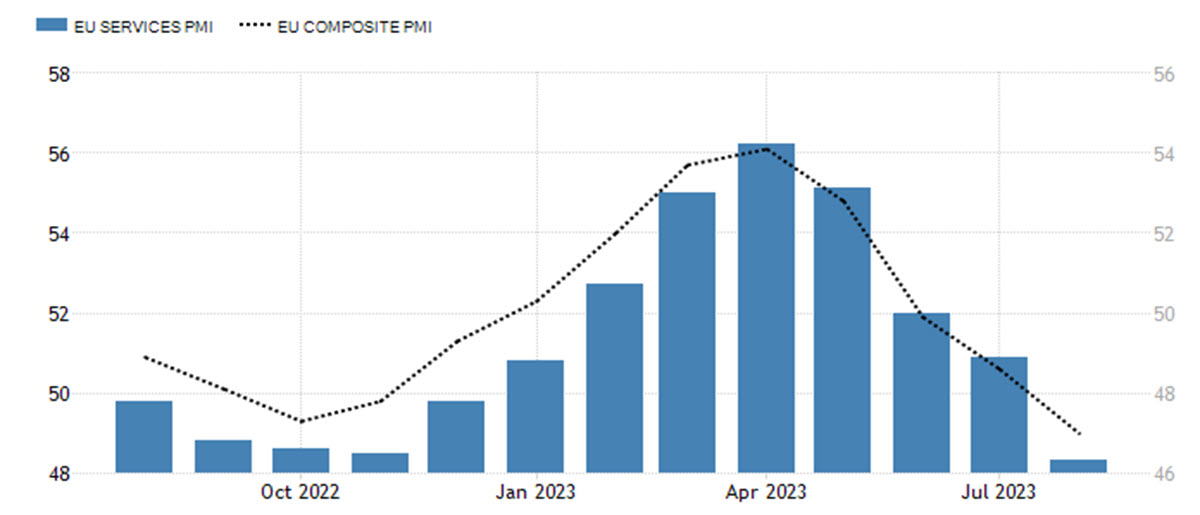

It is widely believed, not without reason, that the task of Lagarde and the ECB is far more difficult than that of her counterpart across the ocean. The PMI data of a few days ago showed grim future prospects, not just for manufacturing which we are used to by now. The leading data on services also returned to contraction after 7 months (48.3), following the composite that relapsed below the critical threshold two months ago. GDP growth for Q2 was not bad (+0.3%), but heavily influenced by the strong Irish figure while Germany continued to stagnate.

Services PMI lhs, Composite PMI rhs

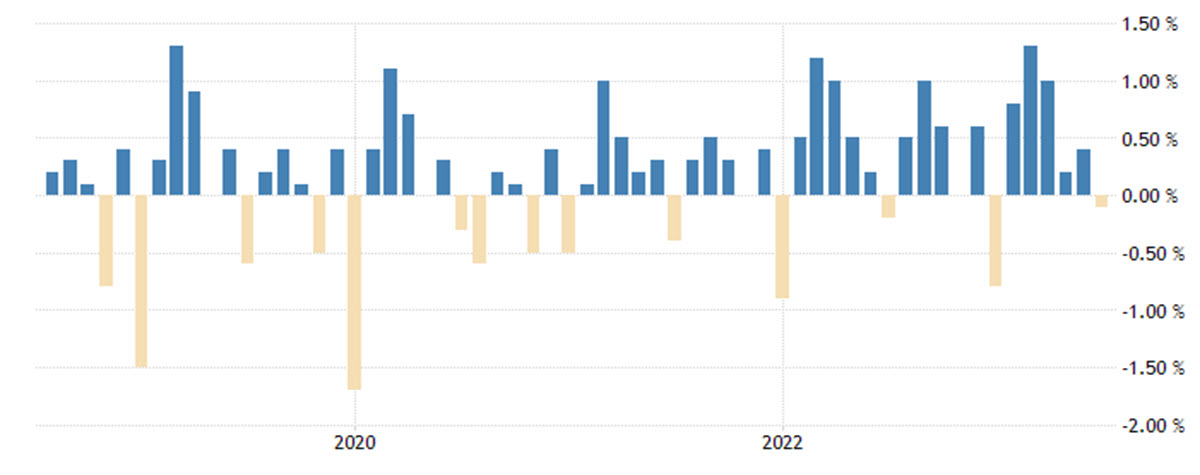

At the same time, price pressure continues to be too high, especially in the service sector, due to wage pressures. True, the PPI has been declining m/m since the beginning of the year and is now in deflationary territory, but both core and headline consumer inflation readings are above 5% (5.5% and 5.3% respectively). If we look at the monthly data, both measures decreased in July but only imperceptibly (+0.1%) and for the first time after 5 months of increases.

Core Inflation m/m

That is why in Jackson Hole last Friday, the president of the ECB said central bankers had to be “extremely attentive that greater volatility in relative prices does not creep into medium-term inflation through wages repeatedly ‘chasing’ prices’’ and that “if global supply does become less elastic, including in the labour market, and global competition is reduced, we should expect prices to take on a greater role in adjustment’’.

The ECB has left the door open to a pause in policy tightening at its next meeting on September 14 and currently a hike at that meeting is only 40% priced in. Despite this, ultra hawkish voices such as Nagel’s have been heard saying it’s too early to think about a pause.

Looking at the futures curve of both the 1- and 3-month Euro short-term rate (ESTR) linked to the new Eurozone overnight swap, there is not a consistent probability of a further hike: the highest level currently priced is for January 2024 at 3.825% (13.5 bps higher than the September 2023 contract). The official deposit rate as of today is 3.75%. The 3m Euribor future gives a very similar picture peaking between December 2023 and March 2024 at levels that do not yet price a 4% deposit rate. (Remember that the ECB has 3 rates, deposit, main refinancing and marginal lending).

TECHNICAL ANALYSIS

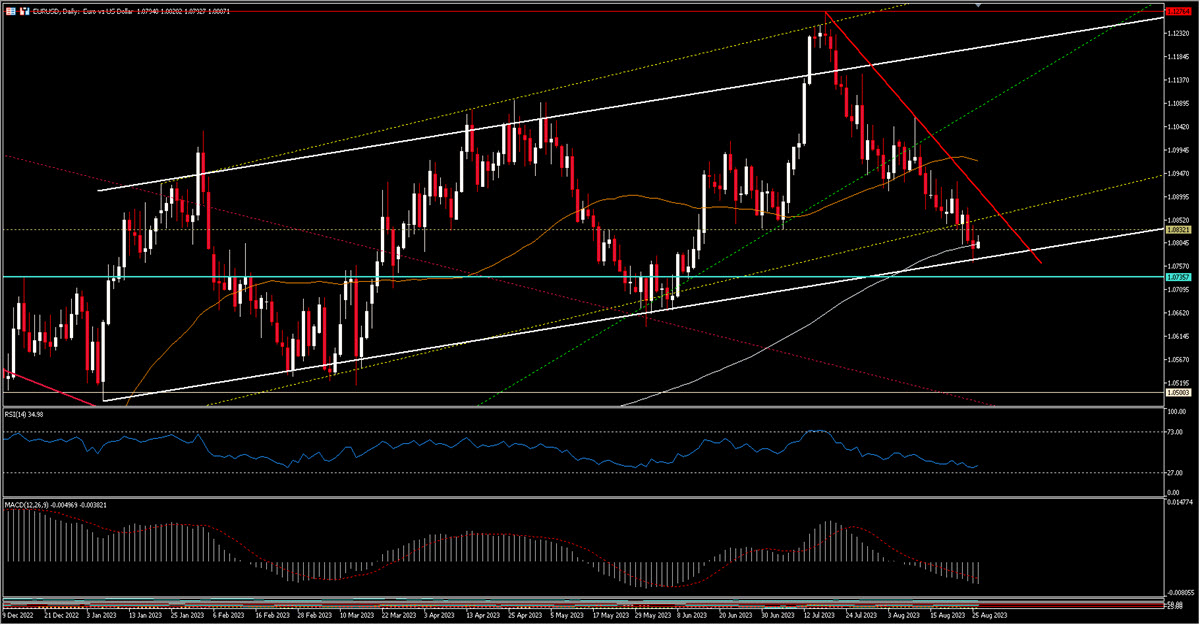

Having said all this, the exchange rate between 2 currencies is influenced by many difficult-to-quantify factors and the interest rate differential is only 1 of them. The EURUSD returned to trade at the 1.07 handle Friday and is recovering to 1.08 (1.0818 now) this morning. It is trying to react to the MA 200 (1.0806) and seems to be close to the lower part of a slightly tilted bullish channel in which it has been moving since early 2023 (note that at the beginning of August it lost the steepest trendline at 1.0975). It will be important to see the reaction to the current levels of this pair so sold lately, as 1.0735 will probably have to hold to avoid further downside (to 1.05?). A reaction will face resistance first at 1.09 and then close to the 50MA (1.0976 today).

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.