A new day, a new intervention by Chinese policy makers. But we will get to the solutions in a moment. Let’s start with the problems.

Part of this began in the mid-1990s when a metal industry worker from a small rural village, Hui Ka Yan, had an idea: to borrow money to buy land. Sell homes on the site before they are built. Use the cash to pay lenders and finance the next real estate project. As hundreds of millions of Chinese were moving from rural areas to the cities and house prices began to rise rapidly, this idea was a huge success and eventually became Evergrande, China’s largest property group.

The rest is much more recent history: as is often the case, the company pushed its leverage too far; by the beginning of the 2020s Chinese property sales started to decline and banks and investors became more cautious about lending to property developers. Evergrande sought different forms of financing, but as early as 2021 it started having problems selling its bonds. By the end of that year, Evergrande’s total liabilities had reached $300 billion. The cash-strapped company struggled to pay suppliers and complete homes. Its property revenues plunged. Finally the fall began to accelerate: trading in the group’s shares was suspended in March 2022 in Hong Kong and a few weeks ago the company filed for bankruptcy protection in the US in its attempt to orderly restructure its foreign debt.

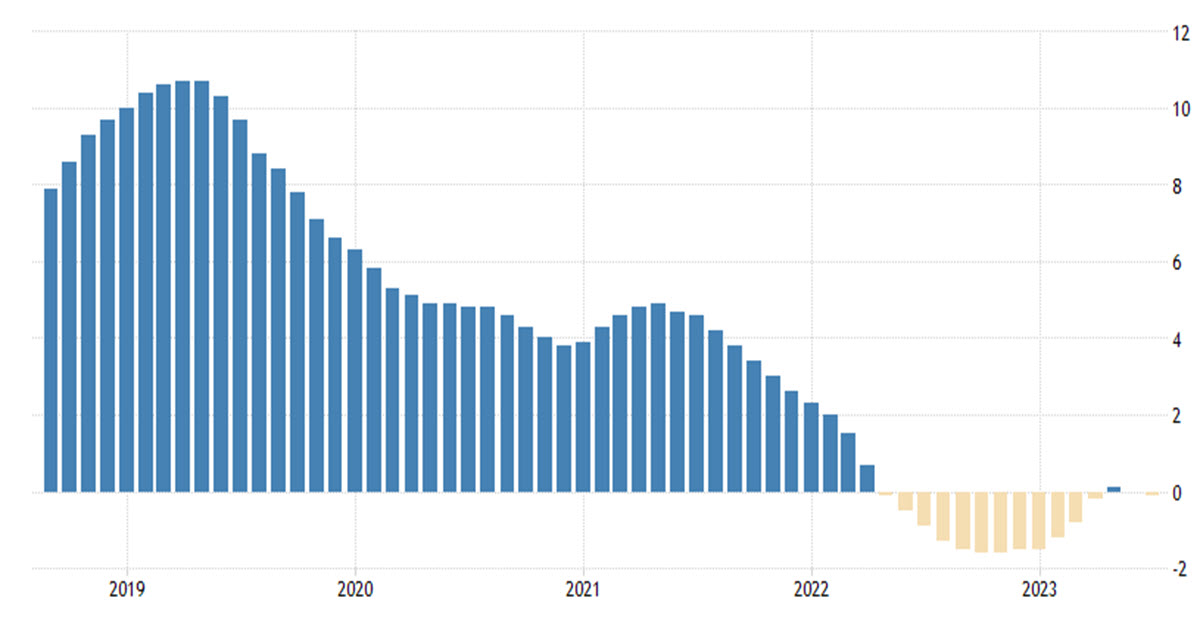

Meanwhile, the problem has become wider: home sales have been plummeting for at least two years now, as you can see in the above Bloomberg chart, and prices are also falling: two days ago, another now-famous real estate giant – Country Garden – posted losses of $6.72 billion for the first six months of the year and, after missing the payment on two coupons on USD-denominated bonds in August, officially warned of a default risk.

The property market in China is worth 29% of GDP.

Home Prices, year on year change

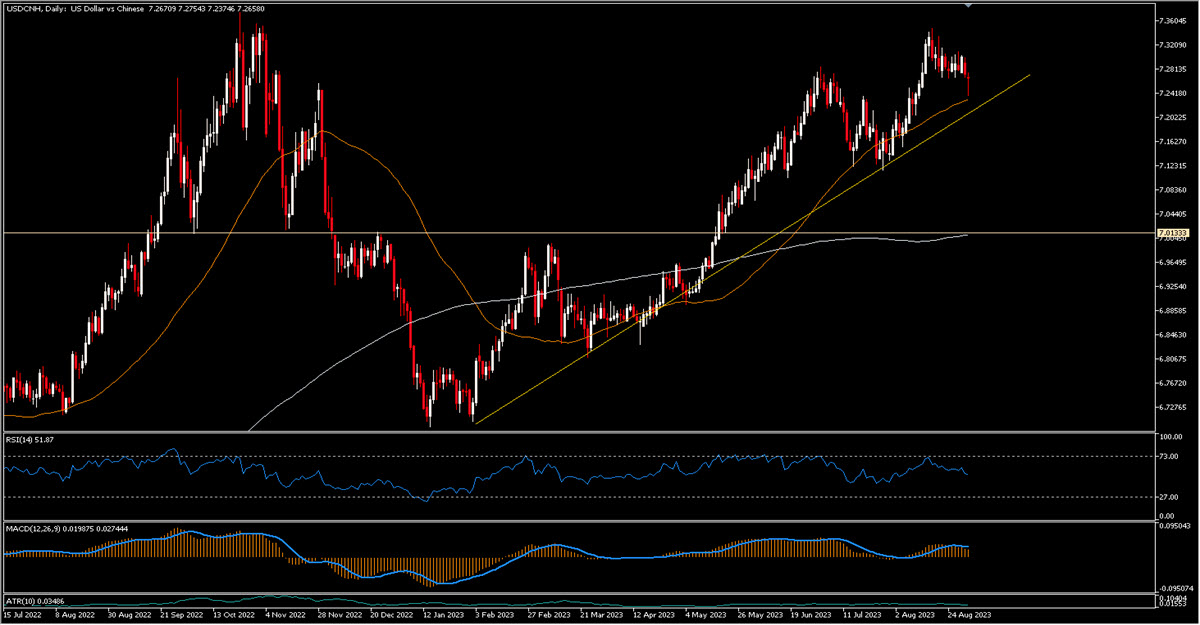

Beijing’s Central government and the PBOC are trying hard to revive the economy. They have a lot of tools at their disposal (first and foremost a USD 3trillion foreign exchange reserve) which they are handling carefully, weighing the results. 2 weeks ago the Central Bank lowered its one-year loan prime rate to 3.45% from 3.55% but surprisingly left its five-year loan prime rate unchanged at 4.2%. This was followed last week with a surprise cut to two other short- and medium-term rates, and the stock market was given a boost by a decreased levy on trading. However, the pressure on rates helped weaken the Yuan, which fell to levels of 7.30 against the USD. And it is in this balance between stimulating the economy without weakening the local currency too quickly that the policy maker has moved. China’s major state-owned banks have been spotted selling US Dollars to buy Yuan in onshore spot foreign exchange market several times during the last weeks. And today there were 2 other moves: down payment minimums for first-time homebuyers have been cut to 20%; and the FX reserve ratio for banks has been cut by 200bps to 4% to rein in Yuan weakness (can now sell more foreign currency in exchange for CNH).

China will certainly be in trouble, but do not underestimate its ability to resist. USDCNH trades lower at 7.26 this morning.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.