On Tuesday [05/09], the Reserve Bank of Australia will make a decision on interest rates, which are expected to remain unchanged for the third consecutive month. Weaker economic growth makes the RBA likely to be more cautious this time around. GDP figures due to be released on Wednesday [06/09] will show whether growth slowed or accelerated in Q2. A less hawkish RBA and growing concerns over a slowdown in China could leave the Australian currency vulnerable to further declines.

Chinese data has been closely watched lately; overall both private and national PMIs were better than expected, suggesting that the economy has not fully recovered. The authorities came up with a series of policies to stimulate the economy this week with a reduction in the down payment required for home buyers being particularly important, given the increased risks emanating from the real estate market. In the event that developer Country Garden fails to repay its debts, it could cause renewed pressure on the Chinese market. Trade balance figures due to weak exports have also been a concern lately. Any downturn in China, as Australia’s trading partner, will have a significant impact on regional exporters.

Meanwhile, Australia’s inflation rate is declining rapidly. Since February 2022, the consumer price index has been falling. In July, it fell to 4.9% y/y. The weighted CPI, one of the underlying indices of inflation, is also declining, from 5.4% to 4.9% y/y, . Another good development is that wage growth seems to have peaked.

The central bank is likely to keep rates steady in September, as the cumulative impact of 400 bps of tightening has yet to be felt. Australia’s economic growth slowed significantly this year due to many challenges. Since last year, the biggest drag on growth has been the housing market, which was the first market to feel the impact of rising borrowing costs. This year, rising interest rates have had a negative impact on consumption, as consumers are pressured to cut back on spending.

The central bank is likely to keep rates steady in September, as the cumulative impact of 400 bps of tightening has yet to be felt. Australia’s economic growth slowed significantly this year due to many challenges. Since last year, the biggest drag on growth has been the housing market, which was the first market to feel the impact of rising borrowing costs. This year, rising interest rates have had a negative impact on consumption, as consumers are pressured to cut back on spending.

GDP growth slowed to just 0.2% q/q in the first three months of the year and is likely to accelerate slightly to 0.3% in Q2. However if the S&P Global PMI survey is any indication, worse figures are likely and the economy may see a small contraction in Q3.

AUDUSD’s underperformance this year has been influenced by more aggressive Fed policy and a stronger American economy, but the underlying cause of this underperformance has been the thorny issues surrounding China in recent months.

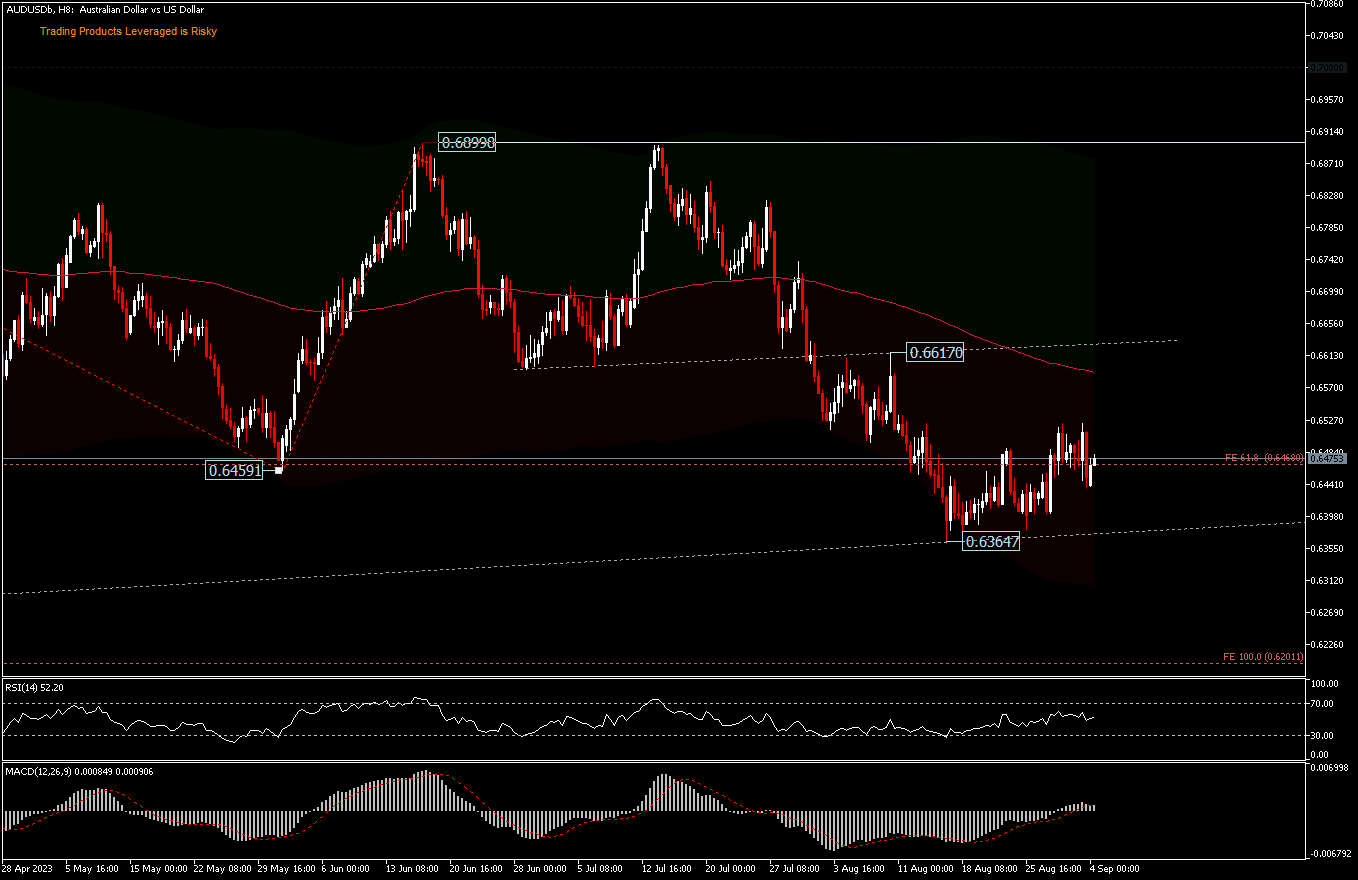

Technical Analysis

AUDUSD, W1 – The pair’s downtrend from the 2021 peak [0.8007] is still ongoing. A decisive break of 0.6170 will target the FE61.8% projection of 0.6021 [from 0.8007-0.6170 and 0.7157 pullback]. The level will now remain a concern, as long as 0.6899 holds.

On the H8 period, consolidation from 0.6364 continued last week and the outlook has not changed. The initial bias still looks neutral at the beginning of this week. In case of another recovery, the upside will be limited by the 0.6617 resistance. A break of 0.6364 will resume a larger decline from the FE100% projection at 6.2059 [from 0.7157-0.6458 and 0.6899 pullback]. Price is currently still moving below the 200 EMA, RSI is floating above the 50 level and MACD is depicting an ongoing consolidation at the moment. However, if the RBA gives a hawkish surprise on Tuesday, then a break above the 0.6617 resistance could bring a short-term change in direction, to test 0.6899.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.