In an interview published last weekend by the Japanese newspaper The Yomiuri Shimbun, BOJ Governor Kazuo Ueda touched on some interesting points that led – as soon as markets reopened Monday morning – to both a sharp appreciation of the JPY and the biggest jump in 10y JGB yields since the central bank revised the upper limit of the long-term interest rate in July. To make a long story short, Ueda had it put in writing that ”It is not impossible that we will have enough by the end of the year to anticipate wage hikes next spring” since, inter alia, corporate performance improved in a wide range of industries, including automobiles and distribution, due to the depreciation of the Yen and the penetration of price increases in the April-June quarter of 2023. Although rising interest rates are a burden on households and corporate finances, if the economy improves, the economy will have the strength to absorb the increased burden (a hint of the future possibility of exiting a negative interest rate regime? – Japan’s official rate is still at -0.10%).

Very important is the fact that Ueda revealed that the July decision is based on reflections that the bank had underestimated the price outlook until now and that he does not want to make the mistakes made by the Fed, which in 2021 had continued to maintain an easy monetary policy and is now struggling to make inflation subside.

The Japan 10 Year Treasury is up 5.9 bps to 0.706% and the JPY is currently up 1.04% against the USD (but was gaining 1.28% earlier in the day – the USDJPY minimum has been hit at 145.90).

TECHNICAL ANALYSIS

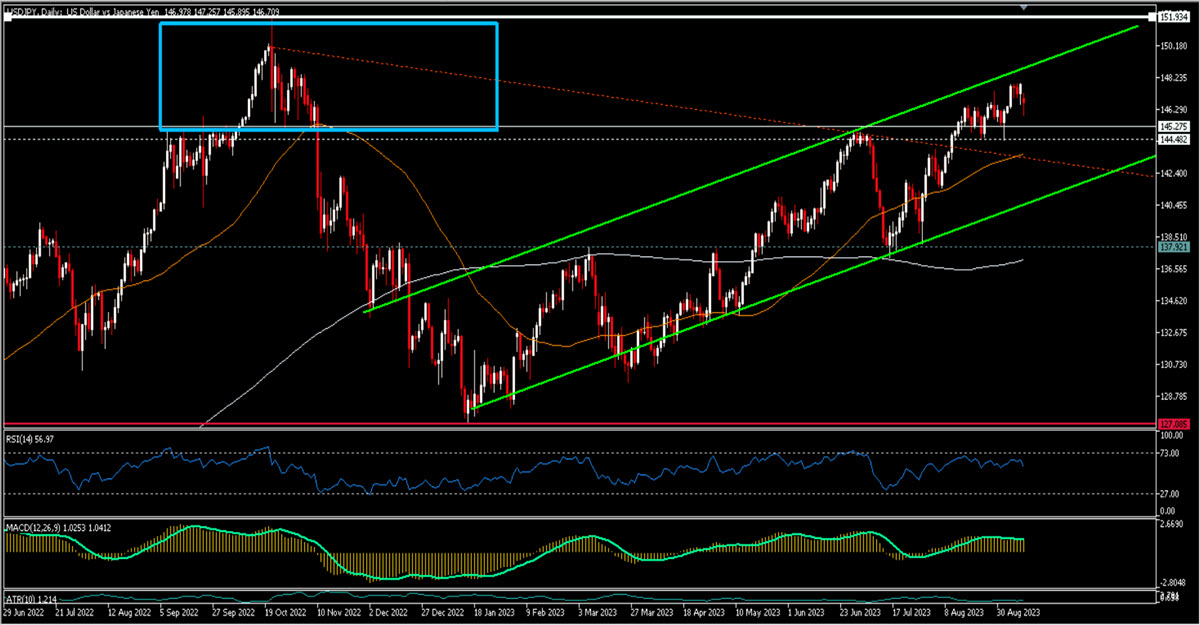

The USDJPY has recently climbed very close to 148 (147.87 has been the high set last Friday) and this is well within the BOJ’s intervention zone of last autumn between 146 and 151.94, the October 2022 high. The bank was in no hurry to use new reserves to stop the devaluation of the national currency, which indeed served monetary purposes well. Continuing with the price action analysis it seems that the USDJPY has come very close to testing the top of a bullish channel and is retreating from there: the natural target would be the bottom of it (currently in the 140.85 area but it will go up) although there are quite a few obstacles to overcome first: 145.25, 144.50, 143.70 and so on. The RSI is cooling off and the MACD is still positive; while the MM200 is flat, the 50 has crossed to the upside and is tilted positively.

Despite the small, slow changes in the economic situation and Ueda’s good intentions and words, the Yen is still a structurally weak currency that offers a huge positive carry trade to institutional investors and – even if they will raise their level of caution about possible sudden news – they are likely to continue to sell it in the medium term.

150.15 is the highest close since 1990, with 151.94 the highest high.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.