Oil prices steadied last week after a nearly 20% decline since September, with anticipation building around the upcoming OPEC+ meeting. Speculation on potential output cuts deepening heightened market uncertainties. However, a reported delay in the meeting to November 30 due to disputes over output targets has temporarily allayed concerns of fresh supply shortages. Currently, the USOIL contract trades at $74.59 per barrel, and Brent is at $79.63.

OPEC+ Outlook: Balancing Act Amidst Disputes

Market expectations on new OPEC+ output cut targets diverge, with a consensus forming around Saudi Arabia possibly extending its unilateral supply cutback of 1 million barrels a day into early 2024. This move aims to maintain current oil price levels despite lower-than-expected demand from China and a supply shortage in the last quarter.

There is lingering speculation that Saudi Arabia may consider a deeper output cut to support future plans amid lower oil revenues. However, the meeting delay, attributed to a disagreement over output quotas, suggests challenges in convincing other OPEC members to endorse deeper cuts.

US Energy Landscape: Breaking Records Amidst Climate Goals

Simultaneously, US Oil and gas production is poised to break records this year, contradicting climate goals. Despite climate initiatives, federal forecasts anticipate a record 12.9 million barrels of crude oil production, doubling the output from a decade ago. Gas production is also set to reach record levels, supported by new export terminals facilitating an export boom, particularly to Europe amid disruptions in Russian gas deliveries.

While the EU and other “high ambition” countries push for a fossil fuel phaseout at COP28, the US government expects robust oil and gas activity to persist until 2050, constituting a third of the world’s planned expansion.

Gas Dynamics: Price Corrections Amidst Regional Factors

Gas prices in the US have dropped to their lowest in twelve weeks, driven by ample storage and lower demand. European gas prices have also corrected, with the Dutch TTF down over 12% in a month. Despite forecasts of increased demand due to cold weather in early December, high storage levels and regional factors have helped maintain price stability.

Spain, with the most LNG terminals in Europe is experiencing congestion as inventories remain high. Renewable energy sources and a warm autumn have suppressed demand, with November seeing an 8.5% YoY decrease in consumption.

USOIL Performance Amidst Economic Trends

Since reaching its peak at $89.80 in October, USOIL experienced a notable decline, breaking decisively below historical support levels. Last week, the price hit its lowest level since July, at 72.33, though it managed to recover some losses. Nevertheless, the asset has been in a downchannel since October, with the upper trendline and 61.8% Fib. level of the $67.00-$93.92 upleg acting as a barrier to any upward movement.

A confirmed break of July’s bottom at $72.33 could prompt further downwards pressure for USOIL and could open the doors to year bottoms, with immediate support at the $70 level.

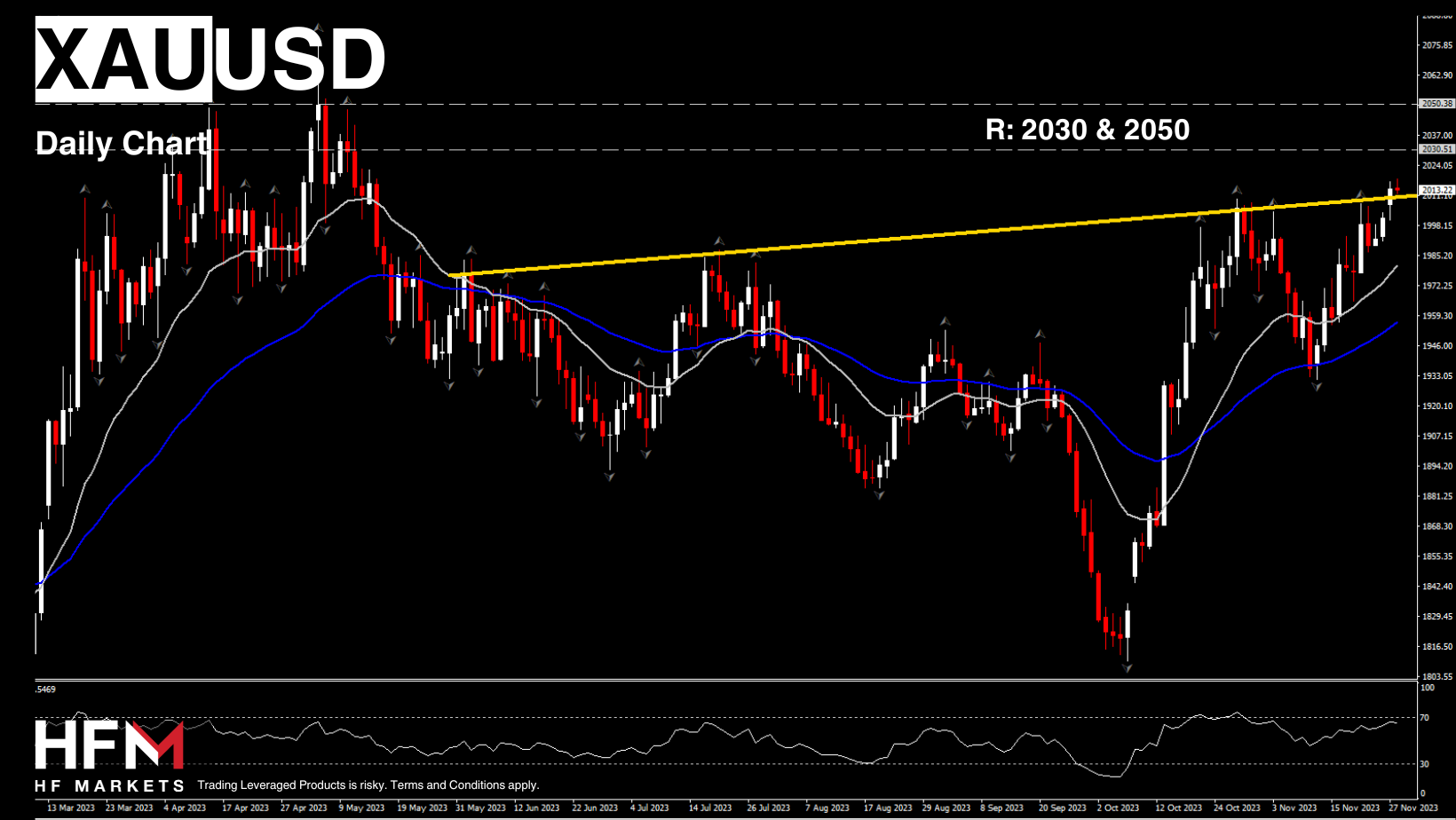

Precious Metals Rally: Gold and Silver Shine Amidst Economic Trends

Gold (XAUUSD) and Silver (XAGUSD) are experiencing heightened demand, with silver up over 6% in the past month. Bullion is trading within $2,010-2,017 per ounce, reaching levels not seen since early May. The ongoing US Dollar correction has been underpinning demand as markets are increasingly convinced that Fed rates have peaked and rate cuts on the agenda in 2024. Non-interest bearing bullion has benefited and is trading at levels not seen since May.

The current upward trend in Gold prices is pushing towards a 6-month high and remains well above the daily simple moving averages. From a technical perspective, the RSI reinforced its bullish bias above neutral line, indicating further potential bullish momentum in the upcoming sessions. In the event of a continued upward movement, the market could aim for the 2,030 and 2,050 resistance level.

Conversely, failure to extend further and a pullback to the 2000 level could see the price of gold retreating towards the 1,980 level which is a confluence of the 20-day EMA and May-October 2023 Resistance level. Below this level, attention may turn to the 50-day EMA and November’s bottom at 1,954 and 1,930, respectively, before potentially reaching the 50% Fibonacci level at 1,910 (October’s upleg).

Silver has been outperforming over the last month and lifted nearly 6% amid concerns over supply shortages amid forecasts of rising demand for industrial silver. The Silver Institute warned of a 2% drop in global mined silver production this year. Increasing investments in solar panels, power grids, and 5G networks continue to support demand expectations. Hence in the event of a continued upward movement, Silver next immediate resistance levels are at 25 and 25.45.

Silver has been outperforming over the last month and lifted nearly 6% amid concerns over supply shortages amid forecasts of rising demand for industrial silver. The Silver Institute warned of a 2% drop in global mined silver production this year. Increasing investments in solar panels, power grids, and 5G networks continue to support demand expectations. Hence in the event of a continued upward movement, Silver next immediate resistance levels are at 25 and 25.45.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.