Ltd. - [GBPJPY,H4] 12_13_2023 9_40_23 AM (2)")

Data reports indicating a fall in UK wages in October caused Sterling to decline, but downside risks were limited as this data is unlikely to change the Bank of England’s policy stance on Thursday (14/12).

Payrolls fell slightly by -13k in November, compared to October. Comparatively to November 2022, paid employment rose by 1.1% y/y or 333k. Meanwhile, monthly wages increased by 5.3% y/y, slowing from 6.2% y/y. In the three months to October, the unemployment rate was unchanged at 4.2% y/y. Average earnings growth (including bonuses) slowed from 8.0% y/y to 7.2% y/y, below expectations of 7.7% y/y. Average earnings growth (excluding bonuses) slowed from 7.7% y/y to 7.3% y/y, below expectations of 7.4% y/y. Source: ONS.

Following the data, money market rates show traders are now fully expecting the Bank of England’s first cut of 25bp for June, while the first cut was expected in August earlier in the week. The Pound Sterling has weakened as a result of continued rate cut speculation.

The Bank of England is of the opinion that wages, which are a major factor in domestic inflation, are still too high to be consistent with reducing inflation to the 2.0% target. While this would be a positive outcome, the BOE is expected to keep interest rates at 5.2% for some time based on the data.

The likelihood of the BOE being more ‘hawkish’ in its statement on Thursday remains low, as this wage data suggests a looser labour market, starting to lead to slower wage growth. The bank believes it is on track to lower inflation, but would like to see a further decline in wage pressures before considering a rate cut.

Meanwhile, Japan’s PPI slowed from 0.9% y/y to 0.3% y/y in November, but beat expectations of 0.1% y/y. Nonetheless, it was still the weakest pace since February 2021. November marked the 11th consecutive month that the pace slowed. Export prices were unchanged at 0.9% y/y. The decline in import prices slowed from -12.7% y/y to -9.7% y/y, remaining negative for the eighth month. On a monthly basis, PPI rose 0.2% m/m. Import prices rose 0.7% m/m. Export prices fell -0.2% m/m. Producer price growth remained below the latest consumer inflation figure for the third month. Consumer price growth excluding fresh food edged up to 2.9% in October.

JPY has seen a sharp decline, falling below 180.00 against GBP, fuelled by a shift in investor sentiment regarding a potential rate hike from the BOJ. Investors, who initially bet on a potential BOJ rate hike, are now reconsidering their positions. BOJ officials appear to be in no hurry to implement policy tightening, unless there is clear evidence of substantial wage growth that supports sustainable inflation. This cautious approach has investors questioning the timing and extent of future policy adjustments. This, in turn, could mean that the yen’s strengthening is only temporary.

The recent surge in the Yen was triggered by Governor Kazuo Ueda’s comments, which signalled the possibility of the central bank abandoning its negative interest rate policy earlier than anticipated. However, this optimism was short-lived as market dynamics quickly changed.

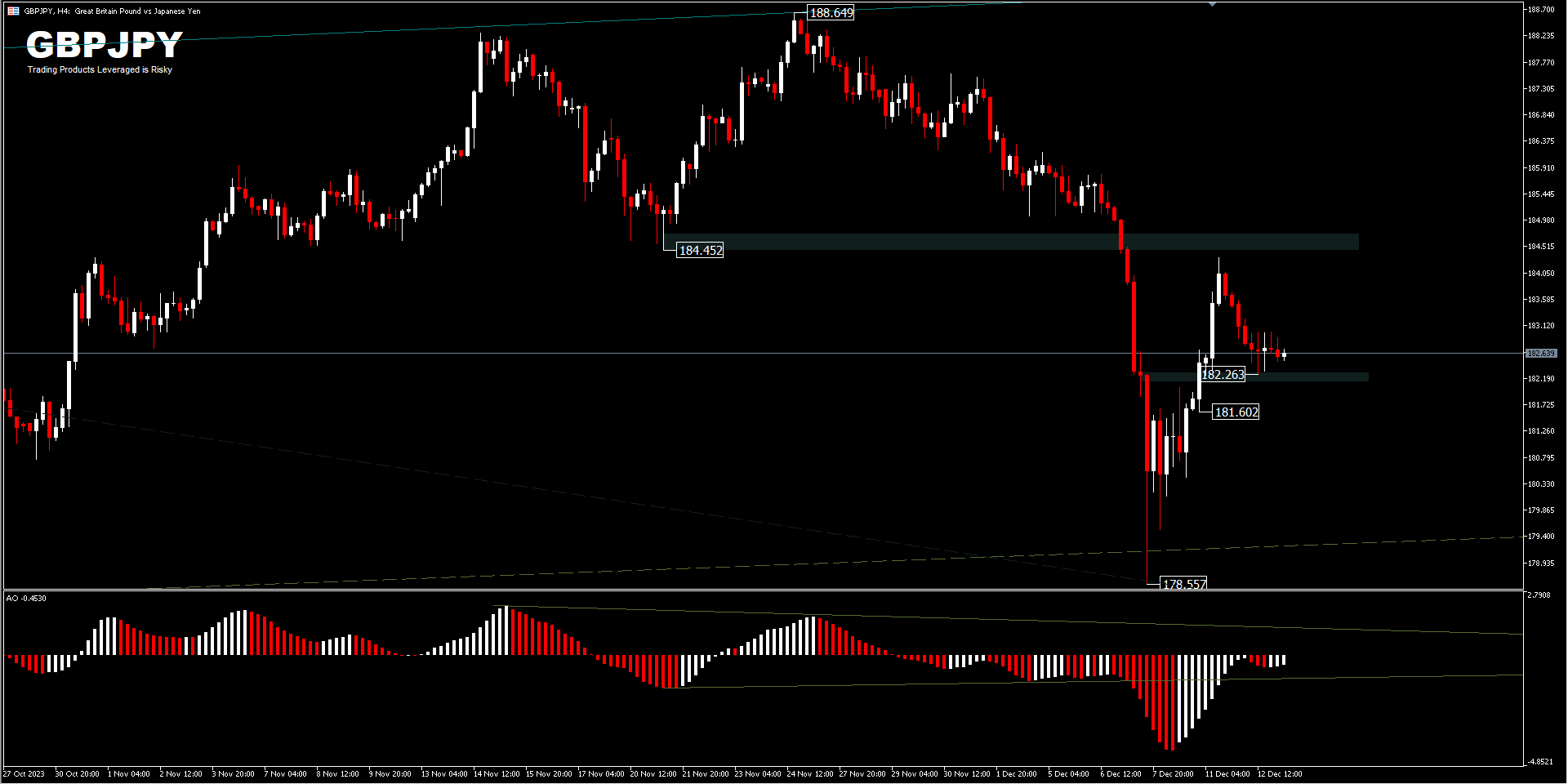

In the FX market, GBPJPY’s decline was contained at the 200-day EMA and hastily bounced back to the neckline range. Technically, the decline that occurred last week does not fully indicate a change in trend, until it is proven that the pair has moved below 176.29 support. If, indeed, that is the case, then prices are projected to FE100 from 188.64-178.55 drawdown and 184.31 at 174.22. At the moment, however, GBPJPY price remains in an upward price trajectory.

Meanwhile, the intraday of the GBPJPY cross pair turned neutral with the current pullback. On the downside, a break of 182.26 minor support is likely to test 181.60 support and will indicate that the rebound is complete. The intraday bias will return to the downside to retest the 178.55 low. The overall outlook will remain bearish as long as the 184.45 neckline generated from the double top pattern holds, as otherwise a retest of 188.65 still remains.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.