Forex markets have remained directionally unambitious. AUDUSD has been the main exception, with the pairing lifting by about 40 pips to within a whisker of the 3-week area seen yesterday at 0.7152. The move was sparked by remarks from RBA’s Debelle, who was upbeat about the labour market.

Canadian Dollar on the other hand, has rotated lower over the last couple of days concomitantly with new trend highs in oil prices. WTI crude prices yesterday printed a five-month high at $64.79. Military tension in Libya have been the latest bullish catalyst, which comes amid a backdrop of OPEC supply curtailment and US sanctions against Venezuelan and Iranian crude exports. WTI benchmark oil prices are now up by over 40% on the year-to-date, which, if sustained, will be a notable benefit to Canada’s terms of trade.

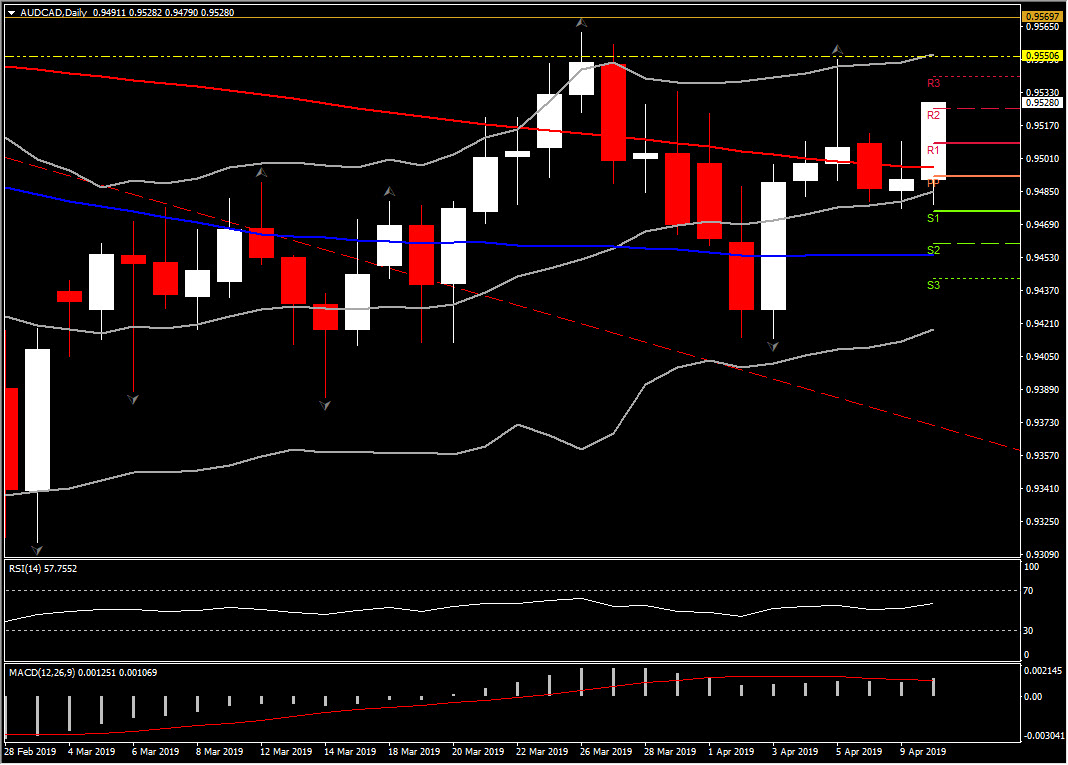

AUDCAD rebounded from the 4-day Support at 0.9475-0.9480 and has since settled in the lower 0.95s, retesting the 2nd Resistance of the day. Next Resistance comes in at 0.9540-0.9550, with the latter holding at Friday’s peak and March’s high area.

Intraday (1-hour chart) the asset looks like it is running out of steam, as it has been struggling to post a new high the last 3 sessions. Meanwhile RSI has flattened, suggesting consolidation in the short term. A failure to cross above R2 along with a pullback below 0.9517 could drive the asset to 0.9490-0.9500 area.

In the medium term however, as we stated in our March 26 post: “AUDCAD is performing its 5th bullish day, leaving behind the 3-month descending triangle and all the daily SMAs. The increasing positive bias seen since the beginning of March, has put pressure on the nearly 3-year Support which has turned to strong Resistance (i.e. 0.9550 also 50-week SMA and FE161.8). The failure last week to break this Resistance area, might have raised concerns for a possible reversal of March’s rally, however the positive outlook holds as momentum indicators preserve the bullish sentiment.”

As all the above are still relevant, with the pair trading within the upper daily Bollinger Bands, northwards of the 3-month descending triangle, the overall positive sentiment holds, despite the positive to neutral daily indicators.

A strong leg above the 50% retracement from the 8-month ceiling, at 0.9550 could strengthen bullish bias. However we need to have in mind the weak weekly candles, with large low wicks, presenting that the bears haven’t given up.

As China is Australia’s largest consumer, any positive or negative news could affect immediately Aussie.Meanwhile global growth concerns and geopolitical trade tensions could also pressure Australian Dollar.

Another downgrade of global growth by the IMF was flagged well in advance yesterday, while the US threat of new tariffs on imports from Europe has reminded markets that geopolitical trade tensions are far from resolved, which put a stop to the rally in recovery in stock markets seen over the past week.

Nevertheless, China’s bond yield meanwhile rose to the highest this year as risk aversion flared up and the focus increasingly turns to China’s still large number of non-performing loans.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.