EURUSD, H4

Eurozone preliminary PMI readings disappoint, with data showing that the manufacturing sector remains stuck in recession. The overall Eurozone manufacturing reading came in at 47.8 in the preliminary April release, up from 47.5 in March, but still showing ongoing contraction. The German manufacturing reading improved to 44.5 from 44.1 but for now at least the German services sector remains strong and the German composite actually improved markedly to 52.1 from 51.4. However, the overall Eurozone Services PMI actually fell to a three month low of 52.5 from 53.3 in March, despite improvements in German and French readings, which suggests weakness in peripheral countries.

Indeed, Markit reported that while the German economy expanded slightly and France stagnated, the rest of the region saw the worst growth rate since late 2013, which on balance left the Eurozone composite reading falling back to a three month low of 51.3 from 51.6 in the previous month. The backlog of work continues to decline and employment growth, while ongoing, is also slowing down.

Concerns about political uncertainty rising were named as one of the key reasons for the further deterioration in sentiment and Markit reported that the rate of quarterly growth has slowed to just under 0.2%, for the Eurozone as a whole. Overall then PMI readings suggest a second month of slowing growth for the Eurozone, rather than the stabilisation in economic activity that the ECB is banking on, which will back the arguments of the doves at the ECB and put pressure on Draghi to push out the guidance on the timing of the first rate hike further into 2020.

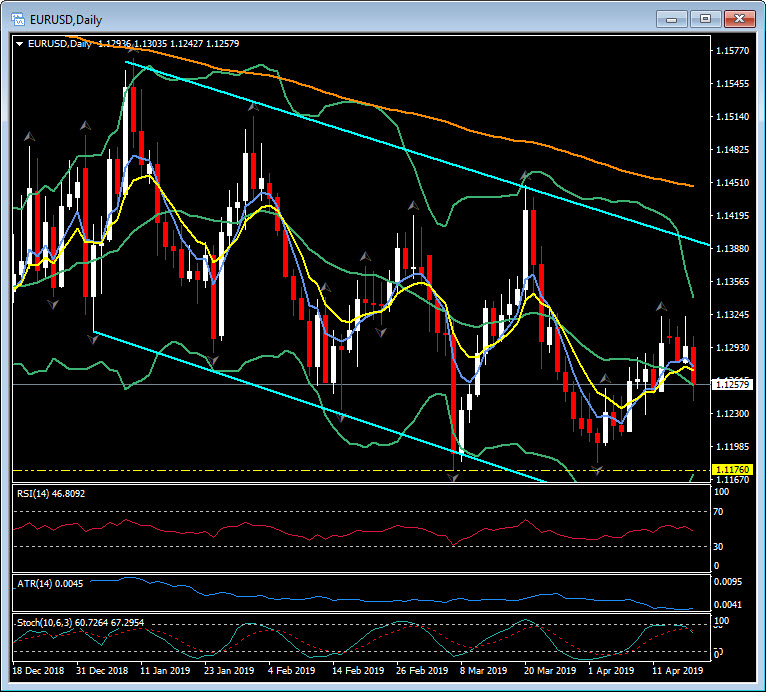

The euro has dropped quite sharply on the weak data out of the Eurozone, with EURUSD plummeting to five day lows at 1.1243, with S3 the next support at 1.1230. This swings the major trend lows seen in March and early April at 1.1176 and 1.1183 back into scope. A breach of these levels would be need to reaffirm that the bear trend that’s been unfolding since early 2018 remains in force. Market participants will now been looking to the dollar side of EURUSD, with today’s release of U.S. March retail sales anxiously awaited for corroboration on the improved growth outlook, as the December plunge was a major worry early in the year. The expected rebound for US retail sales should help maintain a downside directional bias for EURUSD.

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.