FX News Today

- US equities are weaker and Treasury yields fell amid flight to safety trades.The concerns that the global economy will slide back into recession amid prolonged trade tensions continue.

- Chinese media’s suggestion yesterday that Beijing could be limiting the export of rare earths minerals used in the defence and energy sector in order to put pressure on the US only highlighted that the trade war is likely to escalate further before a deal is reached.

- Against that background, US GDP numbers and tomorrow’s inflation data will remain in focus with Bloomberg highlighting that the “Fed model” suggests that there is still value in US stocks, but only if the Fed cuts rates.

- Oil prices also moved up from recent lows and the WTI future is trading at USD 59.23 per barrel.

- In Europe, Stock futures are also pointing to a stabilisation and a slight easing of risk aversion, with European futures moving higher in tandem with US futures.

- Political developments also remain in focus in Europe amid a pretty quiet data calendar, although after the French number yesterday and ahead of German HICP tomorrow, Spanish inflation data may attract some attention.

Charts of the Day

Technician’s Corner

- EURUSD – H1 – printed one-week lows of 1.1125, and is down for the third straight day. Safe-haven flight into the Dollar has been a driver this week, while worse than expected German unemployment data, along with dovish ECB commentary on rate guidance, also weighed on the Euro. Support now comes at last week’s two-year low of 1.1107.

- XAUUSD – H1 – drifted to $1,276.25 slightly below the 200-day EMA, while it remains for a third day in the lower Bollinger Bands pattern. The asset has been in a descending triangle since year’s peak. Support could be found in the near term at May 22 low, at $1,272.45, and a break of this level could retest year’s strong Support at $1,266.25

Main Macro Events Today

- Gross Domestic Product (USD, GMT 12:30) – The Preliminary GDP is expected to show a revised 2.9% gain in Q1, versus the 3.2% advance figure released last month, following a 2.2% growth rate in Q4.

- Tokyo CPI and Production Data (JPY, GMT 23:50) – The country’s main leading indicator of inflation is expected to have dropped slightly, at 1.2% y/y in May. Industrial Production is expected to have improved, growing by 0.2% m/m in April, compared to -0.6% m/m in March, while Retail Sales are expected to have fallen by 0.8% y/y, compared to 1.0% in March.

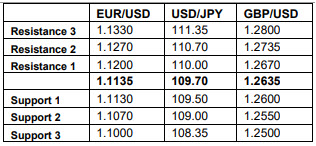

Support and Resistance levels

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.