FX News Today

- Stock markets struggled during the Asian session, with mainland China bourses underperforming.

- Discussions between the US and Mexico ended without a breakthrough last night, which capped risk appetite, and stock markets struggled for direction during the Asian session.

- GER30 futures as well as US futures are also slightly in the red, despite better than expected German manufacturing data at the start of the session.

- German orders data better than expected, with manufacturing orders rising 0.3% m/m in April, while March data was revised up to 0.8% m/m from the 0.6% m/m reported initially. Still, a better than expected number, although the German manufacturing PMI is still firmly stuck in contraction territory and a real rebound doesn’t seem to be in sight.

- The WTI future remains pressured by EIA inventory data yesterday, but has come up to now $51.71 per barrel, after falling to a low of $57.20 in the wake of the report yesterday.

- Geopolitical trade tensions continue to provide a risk backdrop that is keeping bond markets underpinned amid growing conviction of additional central bank support.

Charts of the Day

Technician’s Corner

- NZDUSD & NZDJPY – were the biggest movers and shakers yesterday in the forex markets, with the pairing and cross showing respective 0.6% and 0.7% gains at prevailing levels, with both modestly off highs. The outperformance of the Kiwi dollar, with buying having been catalyzed by RBNZ assistant governor, Hawkesby, vaulted the pair to a 4-week high at 0.7007. Overnight the pair turned lower to 0.6610, However however this could be a correction of the overbought asset. The overall outlook remains bullish as the asset extends Bollingers to the upside.

- USDJPY – H1 – fell to 108.04 overnight, while the pair has since rebounded to 108.15 ahead of then London open. Given the slide in Treasury yields however, further upside for the pairing is likely to be limited. The next support level comes at the January 10 low of 107.77.

Main Macro Events Today

- Gross Domestic Product (EUR, GMT 09:00) – The final Q1 results in the Eurozone are expected to remain unchanged, at an annualised rate of 1.2%, and at 0.4% in quarterly basis.

- Event of the week – ECB Interest Rate Decision (EUR, GMT 11:45) – The ECB is widely expected to keep policy rates on hold at the June council meeting, but the presser is likely to be very dovish, with the guidance on rates likely to be pushed well into 2020.

- Trade Balance (USD, GMT 12:30) – The trade deficit is expected to widen slightly in April to -$50.6 bln from -$50.0 bln in March.

- Initial Jobless Claims (USD, GMT 12:30) Initial jobless claims for the week of May 31 are estimated to fall to 213k, after a 3k rise to 215k in the week of May 25.

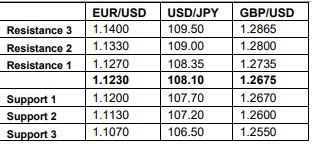

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leverage Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.