")

Asia & European Sessions:

- The markets were weaker Monday as players continued to adjust to Friday’s strong September data and price out aggressive rate cut expectations. In fact Fed funds futures have not only taken out risks for -50 bps next month, but now reflect chances for no action at all.

- Wall Street was in the red all session and the selloff extended into the close, in part given the pop in rates.

- Asian markets mostly corrected, with the Hang Seng leading the way and plunging -7.1% as mainland China bourses returned from a week-long holiday. The CSI 300 rose 5.8% in catch up trade, but failed to match the rally seen elsewhere over the past week.

- Investors were disappointed by the briefing from the Chinese National Development and Reform Commission, which did not present any additional stimulus measures. Instead, a CNY 100 billion investment plan scheduled for next year will be brought forward. China also announced a plan to issue special purpose bonds designed to stimulate local government growth.

- According to FT: ”Hong Kong equities were on track for their worst single-day performance since the global financial crisis on Tuesday, even as stocks in mainland China rose on their first day of trading after an extended break.”

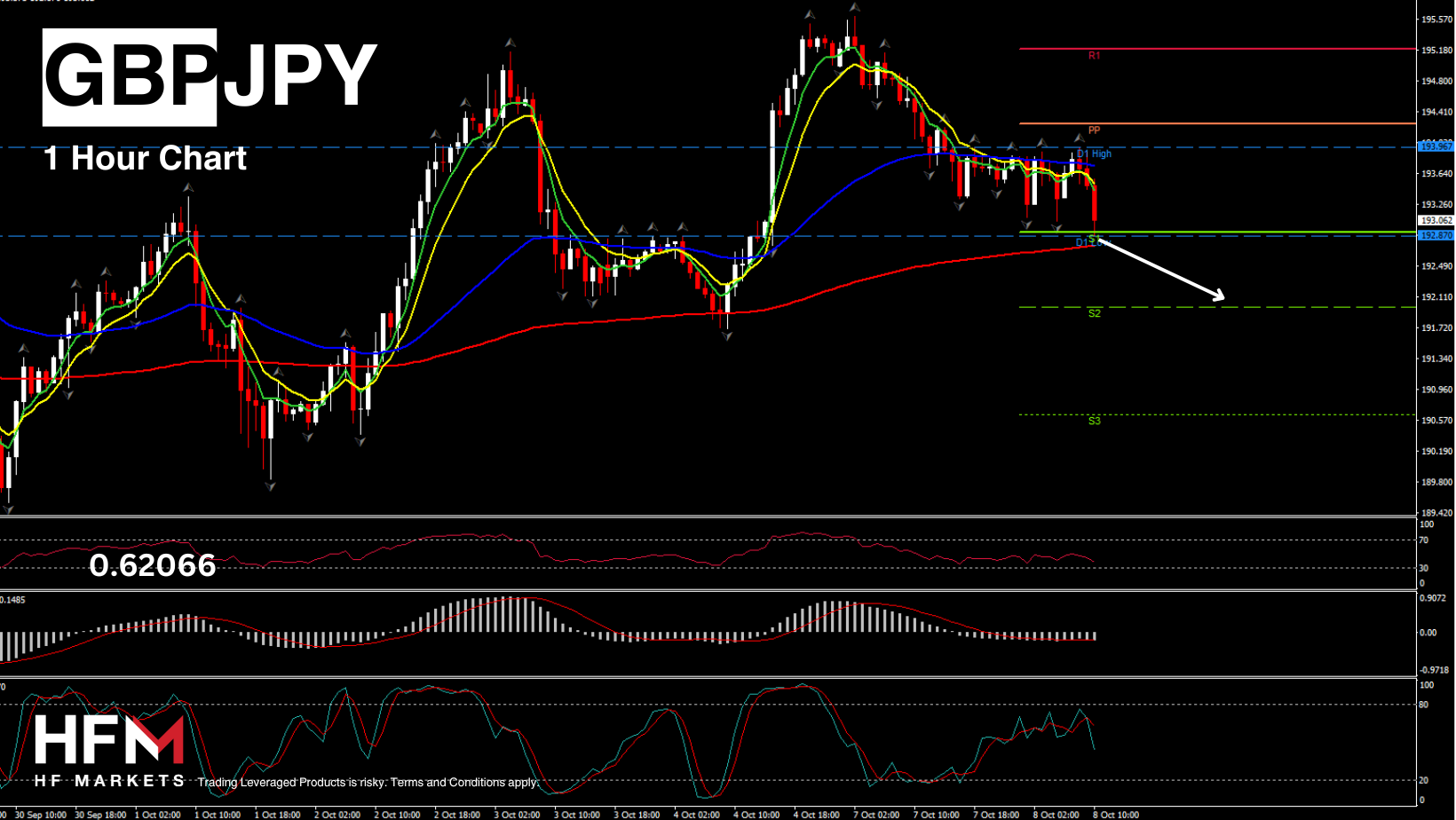

- RBA minutes suggested that the bank will keep interest rates at their 12-year high until inflation shows consistent signs of nearing its target. Minutes also reveal that the board considered both tightening and easing monetary policy, depending on future economic conditions. For now, they have decided to maintain the rate at 4.35%, reflecting uncertainty in the economic outlook.

Financial Markets Performance:

- The USDIndex closed at 102.493 after hitting a high of 102.620, the best since August 15.

- USOil rallied 3.9% to $77.87 per barrel prior to retreating to $75.44.

- Gold holds $2620 floor for a 3rd week in a row.

- Treasury yields hit their highest levels since the summer. The NASDAQ dropped -1.18%, while the S&P500 slumped -0.96%, with the Dow off -0.94%.

- Nikkei lost 1.2% to 38,861.09.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.