FX News Today

- FOMC minutes of the June meeting were a little anti-climactic following Fed Chair Powell’s testimony. However, there were “many” indications that an easier policy stance was the more desired outcome.

- 10-year Treasury yields dropped -2.3 bp to 2.039% overnight, and reopened soft, stopped at 2.064% tailing out from 2.057%.

- US stocks rise, yields drop, Powell’s testimony supported rate cut expectations.

- The S&P 500 briefly topped the 3000 mark for the first time, but the index didn’t manage to hold these levels as stocks generally came off highs.

- USD lower as Powell signals July FOMC rate cut.

- The WTI future is trading at $60.57 per barrel, amid reports that Iranian boats attempted to “impede” the passage of a British tanker.

Charts of the Day

Technician’s Corner

- FX Update: The USD posted fresh lows during the pre-Europe session in Asia as markets continued to readjust Fed easing expectations in the wake of Chairman Powell’s testimony yesterday, which was consistent with a 25 bp rate cut at the end of this month with an addendum stipulating that the Fed has the tools needed and could use them “aggressively” if necessary. The narrow trade-weighted USD index (DXY) has declined by about 0.6% over the last day, earlier printing a six-day low at 96.90, while EURUSD rose to a six-day high at 1.1280 and USDJPY posted a six-day low at 107.86. The US currency saw a similar magnitude of decline against other currencies. In the mix has been an unexpected upward revision to June German HICP, to 1.5% y/y from 1.3% y/y, while news that Iran tried to intercept a British tanker in the Strait of Hormuz (London claiming that its navel ship HMS Montrose saw off three Iranian vessels with “verbal warnings”) saw front-month WTI crude prices spike above $60.0, the first time above this level since late May.

Main Macro Events Today

- Harmonized Index of Consumer Prices (EUR, GMT 06:00) – The German HICP inflation is expected to hold at 1.3% y/y for June.

- Consumer Price Index and Core (USD, GMT 12:30) – May’s CPI has been estimated at a -0.1% drop for headline PPI in June, and a 0.2% rise in the core index. As expected readings would result in a y/y gain of 1.4% for headline PPI, slowing from a 1.8% pace in May, and a 2.1% y/y rise for the core, versus 2.3% in May.

- Fed Chair Powell Testimony 2nd day (USD, GMT 14:00)

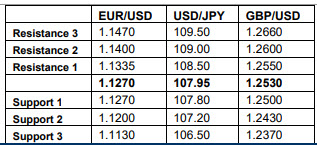

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.