FX News Today

- RISK OFF

- 10-year Treasury yields are down -0.8 bp at 1.637%, JGB yields fell back -1.4 bp to -0.341% after falling to the lowest level since 2016 during the course of the session.

- Risk Aversion continued to dominate during the Asian session and stock markets headed south after the S&P fell more than 1.5% on Monday.

- Bond markets remained supported as investors continue to bet on further central bank action with trade concerns, Brexit risks and political unrest in Hong Kong adding to the risk off backdrop. U.S. 30-year rates are nearing all time lows with Argentina default risks only boosting the flight to quality that is seeing a marked flattening of the curve.

- In Asia escalating political protests in Hong Kong remain in focus and Australia’s 10-year bond yield opened at a fresh all time low. China’s 10-year rate meanwhile fell below 3% for the first time since 2016 before steadying slightly above the 3% mark.

- GOLD breaches $1520.00 (highest since April 2103) and USOil meanwhile is trading at USD 54.81 per barrel.

Charts of the Day

Technician’s Corner

- USD: The The dollar has traded moderately firmer against most of the other main currencies outside the case against the Australian dollar, which has modestly outperformed so far today. The yen softened, correcting some of the recent safe-haven driven gains, despite a tumble on Wall Street yesterday and across Asian equity bourses today, though the Japanese currency has lifted out of its lows into the London interbank open. There is plenty on the worry list, including disruptive pro-democracy protests in Hong Kong and a crash in Argentina’s peso following a poor performance of market-friendly Argentine President Macri in presidential primaries. Singapore also made a substantial cut to its GDP forecast for 2019 (to between 0% and 1%, down from 1.5%-2.5%), citing the deteriorating global conditions, with the Hong Kong situation, along with the U.S.-China and South Korea-Japan trade wars, and Brexit, all getting a mention. The U.S. yield curve is now at its lowest level since 2007, which is seen by many as portending recession, or at least a significant risk of recession. GS analysts also said that the U.S.-China trade war will have a bigger detrimental impact on the U.S. economy than it previously thought. A Reuters poll, meanwhile, found a new high in the probability being ascribed by analysts for there being a no-deal Brexit, which is now pegged at 35%, up from 30% in the previous survey. Amid all this, the PBoC set the yuan at a new near 11-year low against the dollar at the day’s midpoint fixing, at 7.0326, versus 7.0211 yesterday. Given the risk-on vibe, the yen looks likely to find fresh demand in London, with shorts of AUD-JPY and GBP-JPY likely

Main Macro Events Today

- Average Earnings & ILO Unemployment Rate (GBP, GMT 08:30) – The ILO unemployment rate (3-month) is expected to have remained at 3.8%, with average income falling 3.5% y/y in the three months to June in the ex-bonus figure, and to 3.1% in the in-bonus figure from 3.4% y/y in July.

- ZEW Economic Sentiment (EUR, GMT 09:00) – Economic Sentiment for August is projected at -22.3 from the -24.5 seen last month, as the current conditions indicator for Germany turned negative. The overall Eurozone reading though expected to improved slightly at -3.1 from -20.3.

- Consumer Price Index (USD, GMT 12:30) – US CPI is expected to rise a 0.2% headline in July with a 0.2% increase in core prices, following respective June readings of 0.1% and 0.3%. As-expected gains would result in a headline y/y gain of 1.6%, steady from 1.6% in June, while core prices should rise 2.1%, a steady pace from June. Overall, the inflation outlook remains benign, though with an updraft into the end of Q1 and early-Q2 from a petroleum price rebound that reversed course temporarily in May.

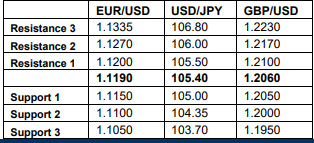

Support and Resistance levels

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.